Federal student loan repayment is changing on July 1, 2026. The SAVE plan is ending, two new options take its place (the Repayment Assistance Plan and a new Tiered Standard Plan), and more than 7 million borrowers have a 90-day window to pick a plan or get auto-enrolled in one. This guide explains every change, who it affects, and what to do by when, with links to a deep dive on each piece.

What is changing for student loans on July 1, 2026?

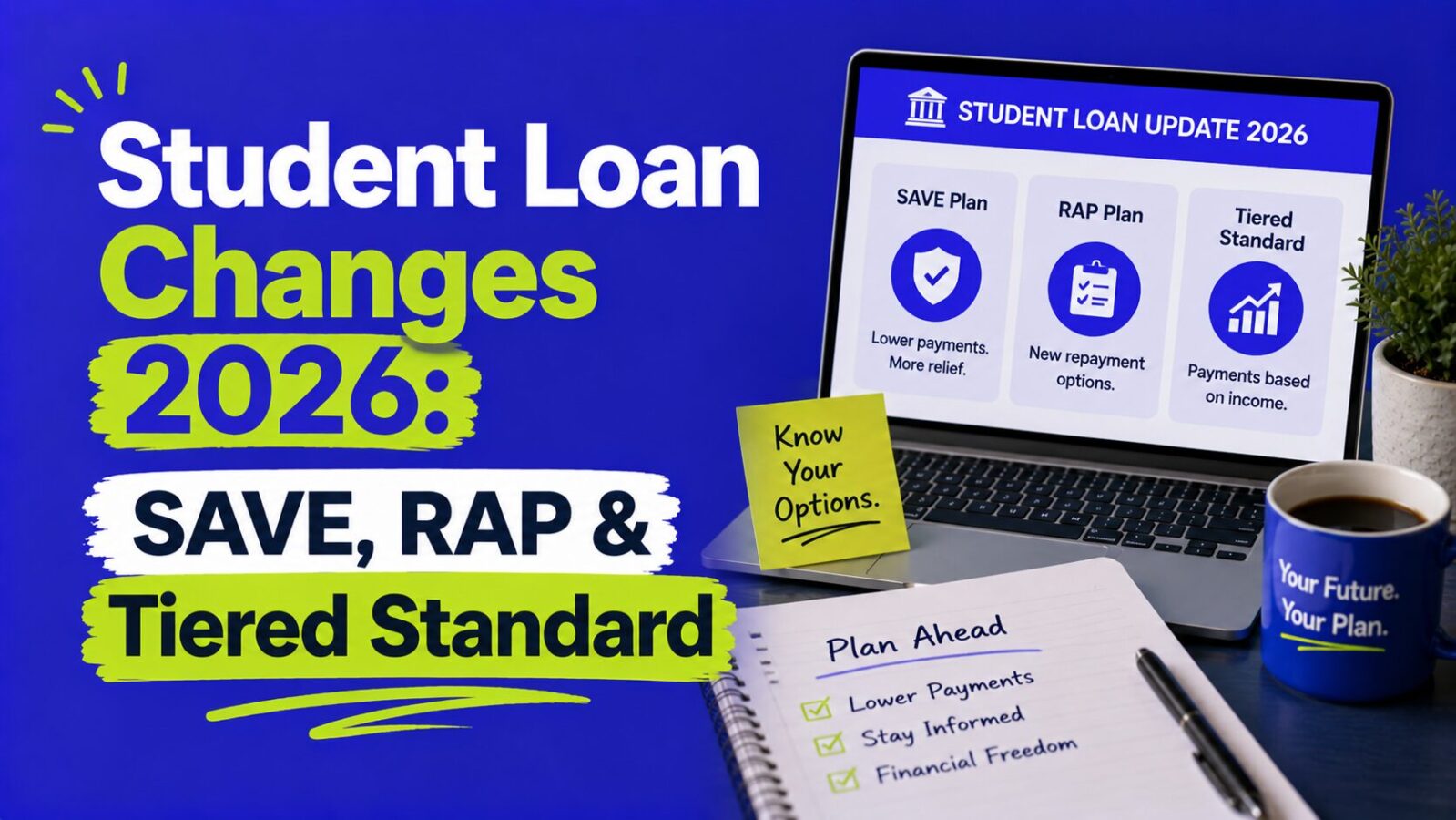

Four things change at once. The SAVE plan ends, the new Repayment Assistance Plan (RAP) opens, a new Tiered Standard Plan opens, and several older repayment plans (PAYE and ICR) close to new enrollment. The changes come from the 2025 budget law (the One Big Beautiful Bill Act) and a March 2026 court ruling that found SAVE unlawful, according to the U.S. Department of Education.

If you have federal student loans, this affects how your monthly payment is calculated, how long you pay, and whether your balance can be forgiven. Private loans are not affected.

Key Takeaways

- SAVE ends July 1, 2026. About 7 million borrowers in SAVE must choose a new plan or be auto-enrolled.

- You get roughly 90 days from your servicer’s notice to pick a plan before you are auto-enrolled.

- RAP sets payments at 1% to 10% of your income, with a $10 minimum and forgiveness after 30 years.

- The Tiered Standard Plan gives fixed 10 to 25-year terms based on your balance, with no income test and no forgiveness.

- Parent PLUS and grad borrowers face their own deadlines. Parent PLUS borrowers who want income-driven repayment need to act before key 2026 and 2028 dates.

Who needs to do what, and by when?

| If you are… | What changes | What to do | Key date |

|---|---|---|---|

| Enrolled in SAVE | Plan ends; forbearance stops | Pick RAP, IBR, or Tiered Standard, or be auto-enrolled | ~90 days after your servicer’s notice (notices begin July 1, 2026) |

| On PAYE or ICR | Plans close to new enrollment | Review whether to move to IBR or RAP | July 1, 2026 |

| A Parent PLUS borrower | Path to income-driven repayment narrows | Consolidate, then enroll in IDR | Consolidate before July 1, 2026; enroll in IDR before July 1, 2028 |

| A future grad student | Grad PLUS ends; new borrowing caps | Plan funding around the new limits | July 1, 2026 |

| Doing nothing | Auto-enrollment applies | Confirm which plan you land in | End of your 90-day window |

The rest of this guide walks through each change. For your exact situation, log in at studentaid.gov and check the notices from your loan servicer.

Why is the SAVE plan ending?

SAVE is ending because a federal court ruled it unlawful in March 2026, and the Department of Education is now moving borrowers off it. SAVE borrowers had been in an interest-free forbearance during the litigation; that pause is winding down, and payments resume as borrowers move to a legal plan.

If you are in SAVE, your loans do not disappear and you are not in trouble. You simply need to choose a new repayment plan. We cover the exact steps in what happens to your payments now that SAVE is ending and a step-by-step walkthrough for switching plans on studentaid.gov.

What is the Repayment Assistance Plan (RAP)?

RAP is the new income-driven repayment plan that opens July 1, 2026. Your monthly payment is 1% to 10% of your adjusted gross income (AGI), reduced by $50 for each dependent, with a minimum of $10 a month. Any remaining balance is forgiven after 360 qualifying payments, which is 30 years, according to the Department of Education.

Two extra features help your balance rather than your payment: RAP covers any unpaid interest each month (so your balance will not grow), and it adds up to $50 toward your principal when your payment alone does not cover that much. For new borrowers taking out loans on or after July 1, 2026, RAP is the only income-driven option.

For the full payment math, worked examples by salary, and the $50 match explained, see what the Repayment Assistance Plan is and how the payment is calculated. To compare it against the older income-driven plan, read RAP vs IBR: which repayment plan to pick in 2026.

What is the new Tiered Standard Plan?

The Tiered Standard Plan is a fixed-term repayment plan with a 10, 15, 20, or 25-year term set by your total loan balance. It is not income-driven, so there is no income recertification, no payment based on what you earn, and no forgiveness timeline. Borrowers with larger balances get longer terms and lower monthly payments.

This is one of the two plans you can be auto-enrolled into if you do nothing. We break down the term brackets in the new Tiered Standard Plan explained.

What happens to IBR, PAYE, and ICR?

Income-Based Repayment (IBR) stays open and still offers forgiveness after 20 or 25 years. PAYE and ICR are closing to new enrollment as part of the transition. IBR remains important because it is one of the plans that still counts toward Public Service Loan Forgiveness (PSLF), along with RAP.

If you are pursuing PSLF, the plan you choose matters, because the Tiered Standard Plan does not qualify. See PSLF in 2026: the new rules and what SAVE borrowers should do.

What happens if you do nothing?

If you do nothing during your 90-day window, your servicer auto-enrolls you in either the Standard Repayment Plan or the new Tiered Standard Plan. That keeps you out of default, but the automatic plan may not be your cheapest option, and it will not be income-driven, so it will not count toward income-driven forgiveness or PSLF.

Before letting the clock run out, it is worth checking what you would be placed in. We cover this in auto-enrolled after 90 days: what happens if you do nothing.

What should Parent PLUS borrowers do?

Parent PLUS borrowers face the tightest timeline. To keep access to income-driven repayment for Parent PLUS debt, you generally need to consolidate into a Direct Consolidation Loan before July 1, 2026, then enroll that loan in an income-driven plan and make a qualifying payment before July 1, 2028, based on Department of Education guidance reported by CNBC.

If you have not consolidated yet, do not assume it is too late. Read Parent PLUS borrowers: what to do if you have not consolidated yet for the current steps and the 2028 follow-up deadline.

What changes for graduate students?

Grad PLUS loans end for new borrowers on July 1, 2026, and new lifetime borrowing caps take effect. The annual Direct Unsubsidized limit for graduate students stays at $20,500, but graduate borrowing is now capped over a lifetime, which changes how many students will fund school. See Grad PLUS is gone: how grad students borrow now.

Should you refinance your student loans in 2026?

For most federal borrowers, the answer is no, because refinancing federal loans with a private lender permanently gives up RAP, IBR, income-driven forgiveness, and PSLF. Refinancing can make sense only for borrowers with high, stable incomes or private loans who will not use any federal protection and can qualify for a lower rate.

If that describes you, compare offers carefully and understand the trade-off first. Our guide to how to refinance student loans covers when it helps and when it hurts.

How do you switch plans on studentaid.gov?

You change plans by logging in at studentaid.gov, choosing “Manage Loans,” and applying for the new plan. Giving consent for the Department to pull your income directly from the IRS makes an income-driven application faster, and the application takes about 10 minutes. Full steps are in our studentaid.gov walkthrough.

Where should you go next?

Use these guides to go deeper on the part that affects you:

- How to pay off student loans fast, with every repayment strategy compared.

- Student loans vs credit card debt: which to pay first.

- Student loan default in 2026 and how to get out of it.

- Social Security garnishment for defaulted loans and how to stop it.

- The forgiveness tax bomb: when forgiven balances are taxable.

Frequently asked questions

When exactly does SAVE end?

SAVE ends July 1, 2026. Servicers begin sending notices that day giving borrowers about 90 days to choose a new plan, according to the Department of Education.

Will my payment go up?

It can. Many SAVE borrowers had very low or $0 payments. Under RAP, the minimum is $10 a month and payments rise with income, so some borrowers will see a higher payment. Your exact number depends on your income and dependents.

Is RAP better than the Tiered Standard Plan?

It depends on your goal. RAP ties payments to income and offers forgiveness after 30 years and counts toward PSLF. The Tiered Standard Plan has fixed payments and no forgiveness. Lower earners and PSLF seekers usually prefer an income-driven plan like RAP or IBR.

Do I have to do anything if I am not in SAVE?

If you are on a plan that stays open, like IBR or the Standard Plan, you may not need to act now. Check studentaid.gov for any notices, and review your options if you are on PAYE or ICR, which are closing to new enrollment.

Does refinancing affect these new plans?

Yes. Refinancing federal loans into a private loan permanently removes access to RAP, IBR, income-driven forgiveness, and PSLF. Only consider it if you will not use federal protections.

Bottom line: July 1, 2026 resets federal student loan repayment. If you are in SAVE, find your servicer’s notice, compare RAP, IBR, and the Tiered Standard Plan, and choose before your 90-day window closes so you control the outcome instead of being auto-enrolled.

A quick note: this guide is here to help you understand your options, not to act as personal financial, legal, or tax advice. Repayment plan rules and dates come from the U.S. Department of Education and can change over time, so it is always worth checking your own numbers and deadlines at studentaid.gov or with your loan servicer before you make a move.