Pick RAP if you want lower payments tied to your income, protection from a growing balance, and you do not mind a 30-year forgiveness timeline. Pick IBR if you want a shorter path to forgiveness (20 or 25 years) and your income is high enough that IBR’s payment is competitive. Both plans count toward Public Service Loan Forgiveness (PSLF), so for public-service workers the choice is mostly about payment size and forgiveness timing.

RAP vs IBR: which one should you choose in 2026?

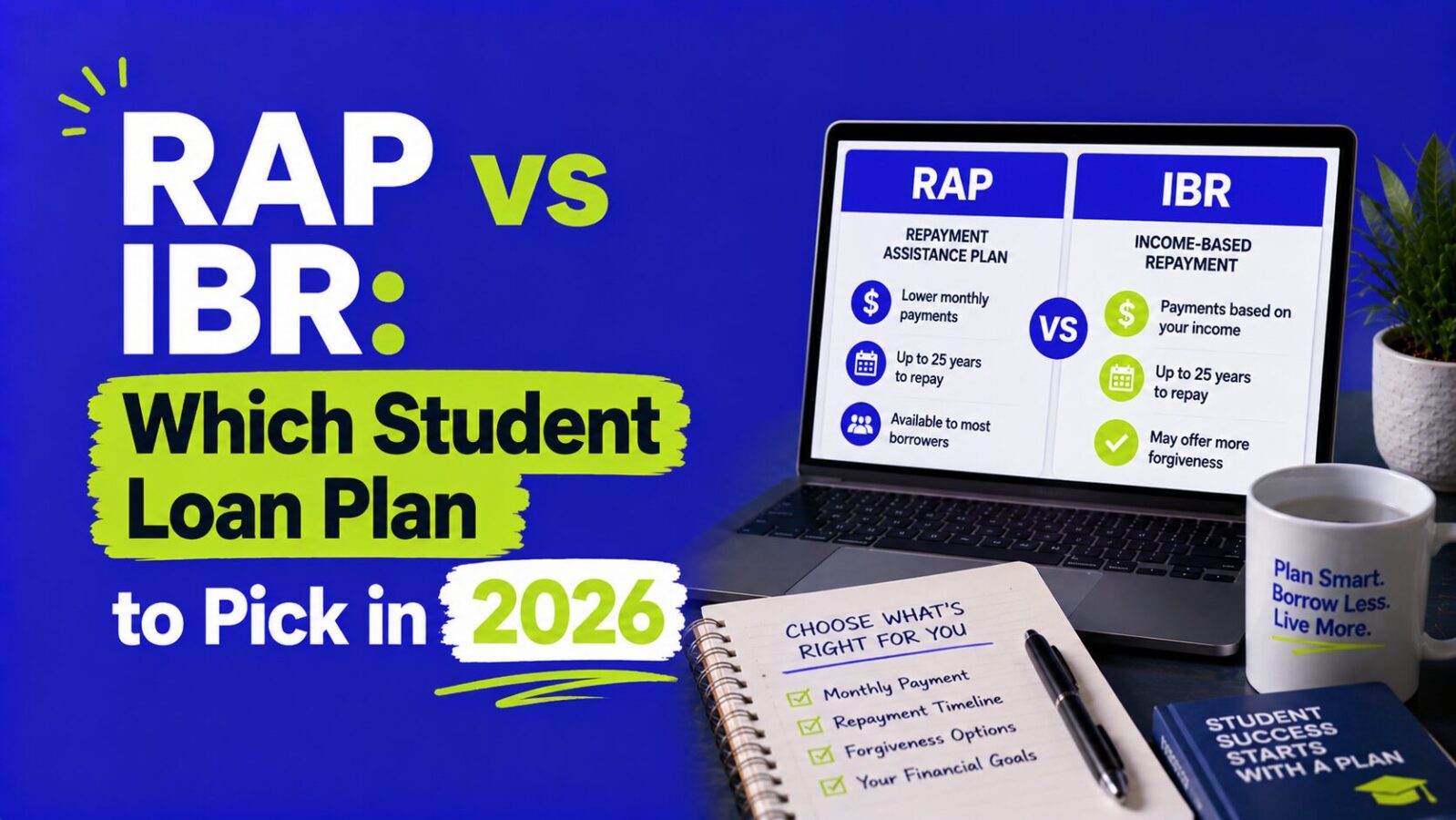

The Repayment Assistance Plan (RAP) and Income-Based Repayment (IBR) are the two income-driven plans most borrowers will compare after the SAVE plan ends on July 1, 2026. RAP is the newer plan with a built-in interest subsidy and a 30-year forgiveness window. IBR is the older plan with a shorter forgiveness window but no interest subsidy. The right pick depends on your income, your dependents, and whether forgiveness speed matters to you.

Key Takeaways

- RAP: 1% to 10% of income, $10 minimum, no balance growth, $50 principal match, forgiveness after 30 years.

- IBR: payment based on discretionary income, forgiveness after 20 or 25 years, but your balance can grow.

- Both count toward PSLF. The new Tiered Standard Plan does not.

- Lower earners often pay less and avoid balance growth under RAP.

- Higher earners sometimes find RAP gets expensive; IBR or another plan may be cheaper.

How do RAP and IBR calculate your payment differently?

RAP uses your adjusted gross income (AGI) directly. Your payment is a percentage of AGI, from 1% to 10%, minus $50 per dependent, with a $10 minimum, according to the Department of Education.

IBR uses your discretionary income, which is your income above 150% of the federal poverty guideline for your family size. Your payment is generally 10% or 15% of that discretionary income, depending on when you first borrowed. Because IBR subtracts a poverty-line amount before applying its percentage, it can produce a low payment for borrowers with families or lower incomes.

The practical difference: RAP’s math is simpler and includes an interest subsidy, while IBR’s math protects more income at the bottom but can let your balance grow if your payment does not cover the interest.

RAP vs IBR side by side

| Feature | RAP | IBR |

|---|---|---|

| Payment basis | 1%–10% of AGI | 10% or 15% of discretionary income |

| Dependent benefit | −$50 per dependent | Larger family size lowers discretionary income |

| Minimum payment | $10/month | Can be $0 for very low income |

| Balance growth | No; unpaid interest is waived | Possible; interest can outpace payments |

| Principal help | Up to $50/month match | None |

| Forgiveness | After 360 payments (30 years) | After 20 or 25 years |

| Counts toward PSLF | Yes | Yes |

Confirm the IBR percentage and forgiveness term that applies to your loans at studentaid.gov, since it depends on your borrowing history.

When is RAP the better choice?

RAP usually wins for lower and middle earners who want their balance to stop growing. If you had a low or $0 payment under SAVE, RAP’s $10 floor and interest waiver keep things manageable and prevent your balance from ballooning. The $50 principal match also chips away at what you owe in the early years when progress is otherwise slow.

RAP is also the only income-driven plan available to brand-new borrowers who take out loans on or after July 1, 2026, so for many newer borrowers it is the default income-driven path.

When is IBR the better choice?

IBR can win when a shorter forgiveness timeline matters or when your discretionary-income payment comes out lower than RAP’s AGI-based payment. IBR forgives remaining debt after 20 or 25 years, which is sooner than RAP’s 30 years, so a borrower expecting a long forgiveness horizon may reach the finish line faster on IBR.

For higher earners, RAP can get expensive because it is a flat percentage of AGI with no poverty-line deduction. Consider a borrower earning $95,000 with one dependent: RAP charges about 9% of AGI, which works out to roughly $662 a month. For that borrower, IBR or even the standard plan may cost less, so it is worth running both.

Estimate your RAP payment

Use this to get a quick RAP estimate, then compare it against the IBR figure shown in your studentaid.gov account.

RAP Payment Estimator

For the full RAP rules, see what the Repayment Assistance Plan is. To understand the fixed-term alternative, read the Tiered Standard Plan explained, and if you are going for forgiveness through work, see PSLF in 2026.

What if neither plan fits, should you refinance?

Only if you will not use federal protections. Refinancing federal loans into a private loan permanently removes RAP, IBR, income-driven forgiveness, and PSLF. It can lower your rate if you have a high, stable income or private loans, but for most federal borrowers staying in an income-driven plan is the safer call. See how to refinance student loans for the trade-offs.

Frequently asked questions

Is RAP always cheaper than IBR?

No. RAP is often cheaper for lower earners and prevents balance growth, but for higher earners RAP’s flat AGI percentage can exceed IBR’s discretionary-income payment. Run both numbers before choosing.

Which plan is better for PSLF?

Both RAP and IBR count toward PSLF, so either works for public-service forgiveness after 10 years of qualifying payments. The Tiered Standard Plan does not count, so avoid it if you are pursuing PSLF.

Can I switch from IBR to RAP later?

Borrowers can generally change income-driven plans, though the details depend on your loan type. Check your options at studentaid.gov before switching, since changing plans can affect your payment count.

Does RAP forgive my balance tax-free?

Tax treatment of forgiven student debt can change and depends on federal rules at the time of forgiveness. See our guide to the student loan forgiveness tax bomb and confirm current rules with a tax professional.

What happens to my balance under each plan?

Under RAP, unpaid interest is waived, so your balance will not grow. Under IBR, if your payment does not cover the monthly interest, your balance can grow over time.

Bottom line: RAP suits lower and middle earners who want stable, income-based payments and no balance growth, while IBR can suit those who want faster forgiveness or whose discretionary-income payment is lower. Both count for PSLF, so compare your actual numbers at studentaid.gov before you lock in.

For the full set of July 1 changes, start at our hub on student loan changes in 2026.

A quick note: this guide is here to help you understand your options, not to act as personal financial, legal, or tax advice. Repayment plan rules and dates come from the U.S. Department of Education and can change over time, so it is always worth checking your own numbers and deadlines at studentaid.gov or with your loan servicer before you make a move.