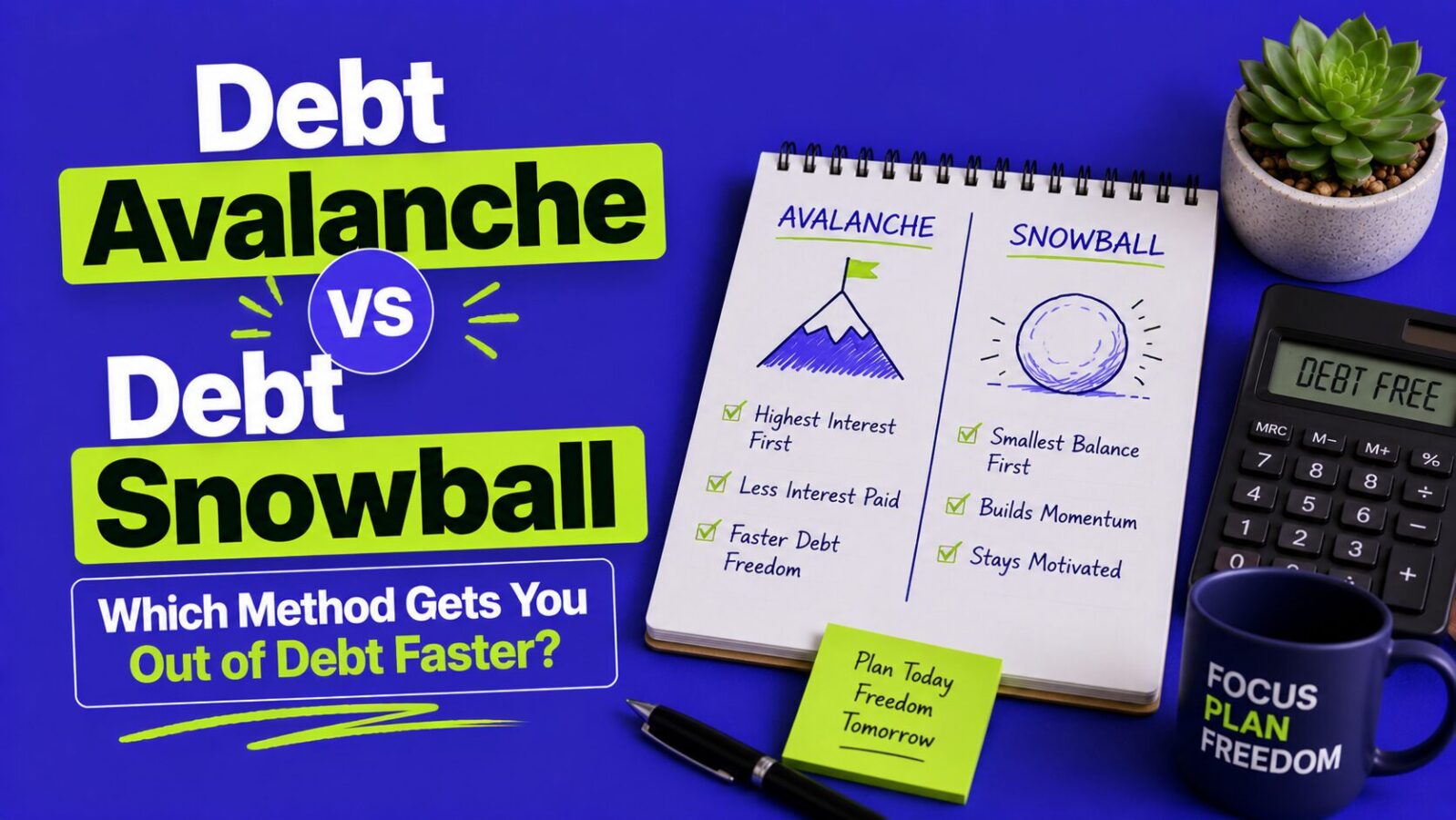

The debt avalanche saves more money; the debt snowball keeps more people on track. Both pay minimums on every debt and send extra cash to one target: the avalanche attacks the highest interest rate first, the snowball the smallest balance first. The avalanche always pays less interest and finishes slightly faster on paper, but the snowball has higher completion rates because early wins build momentum. The right choice depends on your psychology more than the math. Here is an honest comparison.

Key Takeaways

- Avalanche = highest rate first; it pays the least total interest.

- Snowball = smallest balance first; it delivers quick wins and higher completion rates.

- The interest difference is often small, so finishing matters more than optimizing.

- How much extra you pay matters far more than which method you pick.

What Is the Core Difference?

Both methods start the same: pay the minimum on every debt each month. The only difference is where your extra money goes. The avalanche sends it to the highest-rate debt first; the snowball sends it to the smallest balance first, regardless of rate. Everything else follows from that one choice.

Which Wins on Math?

On pure numbers, the avalanche always pays less interest and finishes sooner. Take three debts and $500 a month available ($290 in minimums, $210 extra):

| Debt | Balance | Rate | Minimum |

|---|---|---|---|

| Credit Card A | $4,200 | 24.99% | $105 |

| Credit Card B | $1,800 | 19.99% | $45 |

| Personal Loan | $6,000 | 11% | $140 |

The avalanche targets Card A, then B, then the loan; the snowball targets Card B, then A, then the loan.

| Avalanche | Snowball | |

|---|---|---|

| Months to debt-free | ~28 | ~30 |

| Total interest paid | ~$1,870 | ~$2,090 |

| First debt eliminated | Month 16 (Card A) | Month 8 (Card B) |

The avalanche finishes about 2 months sooner and saves roughly $220, while the snowball clears the first debt 8 months earlier for an early win.

Estimate Your Own Payoff

Use this calculator to compare the two methods for your specific debts:

Debt Snowball vs Avalanche Calculator

Which Wins on Psychology?

A 2012 Journal of Marketing Research study found people are more motivated by the number of debts remaining than by their size or interest cost, so eliminating whole accounts builds momentum. A 2016 Harvard Business Review study of 6,000 debt-management clients found that focusing on one debt at a time meaningfully increased the odds of full payoff, no matter which debt came first. The avalanche is mathematically better, but a method you quit at month 6 is worse than one you finish over 30 months. If quick wins keep you going, the small extra interest is a fair price.

How Do You Decide Which Method Fits You?

Choose the avalanche if you are motivated by numbers and stay disciplined without quick wins, you have one debt at a dramatically higher rate (28%+ vs 15%), or you have a hard payoff deadline and need minimum time. Choose the snowball if you have lost motivation paying off debt before, you have several small debts that feel overwhelming, you need an early win to believe the plan works, or your rates are all within a few points of each other.

What About a Hybrid Approach?

Many people blend the two: knock out the one or two smallest debts first (snowball) to clear mental clutter and free up payments, then switch to avalanche order for the larger, higher-rate balances. This captures early momentum without giving up much interest savings on the big debts.

What Matters More Than the Method?

How much extra you put toward debt dwarfs the avalanche-versus-snowball choice. In the example, the two methods differ by about $220 in interest, but paying $500 a month instead of $300 is a difference of thousands of dollars and years. Finding an extra $100 to $200 a month through spending cuts or income beats optimizing which debt goes first. Whichever method you use, track progress visually (a spreadsheet, a fill-in chart, or an app like Undebt.it), since seeing the number drop keeps motivation alive. See our guide on paying off credit card debt fast.

FAQ

Is the debt avalanche or snowball better?

The avalanche saves the most interest and finishes a bit faster; the snowball has higher completion rates because early wins build momentum. The best method is the one you will actually stick with.

How much does the avalanche really save?

Often less than people expect, sometimes just a couple hundred dollars on moderate debt. The gap grows when one debt has a much higher rate than the others.

Can I combine the two methods?

Yes. A common hybrid clears the smallest one or two balances first for momentum, then switches to highest-rate order for the rest, capturing both motivation and savings.

What matters more than choosing a method?

The amount you pay each month. Adding $100 to $200 to your monthly payment shortens your timeline and cuts interest far more than picking avalanche over snowball.

Bottom Line

Pick the avalanche to save the most interest or the snowball to stay motivated, but know the gap between them is usually small, so finishing matters more than optimizing. The real lever is how much extra you pay each month, so focus there and track your progress. To go deeper, see our guides on paying off credit card debt fast, how much debt is too much, and paying off debt on a low income.

This article is for educational and informational purposes only and is not financial advice. Example figures are illustrative; your results depend on your specific balances, rates, and payments.