If your federal student loans were forgiven on or after January 1, 2026, you may owe federal income tax on the cancelled amount. The temporary relief that made forgiveness tax-free from 2021 through 2025 expired at the end of last year, and the One Big Beautiful Bill Act did not extend it. This affects income-driven repayment (IDR) forgiveness, not Public Service Loan Forgiveness, which stays tax-free. Here is who is affected, how much it could cost, and what to do.

Key Takeaways

- IDR forgiveness is taxable again at the federal level starting January 1, 2026.

- PSLF stays permanently tax-free, so public-service borrowers are not affected.

- The insolvency exclusion (Form 982) can wipe out the tax for many borrowers.

- Start saving for the bill now if forgiveness is coming in the next few years.

What Changed?

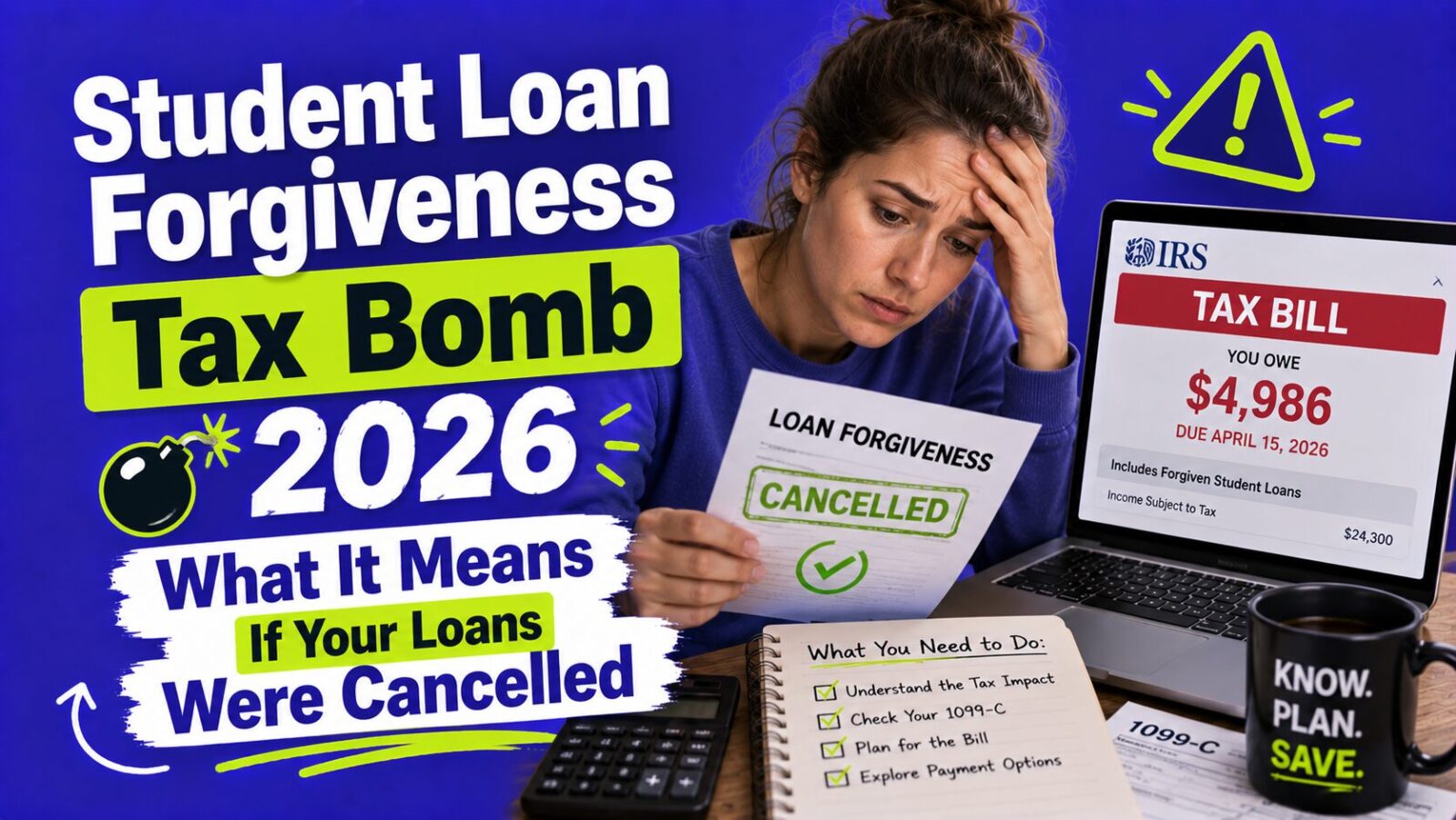

Normally, cancelled debt is taxable income: if a lender forgives $30,000, that $30,000 is added to your taxable income for the year. The American Rescue Plan Act of 2021 created a temporary exception making federal student loan forgiveness tax-free from January 1, 2021 through December 31, 2025, covering IDR forgiveness, employer repayment assistance, and certain other programs. That exception expired on December 31, 2025, and the OBBBA (signed July 4, 2025) did not extend it. So starting January 1, 2026, forgiven federal student loan balances are again taxable as ordinary income, with one major exception: Public Service Loan Forgiveness remains permanently tax-free under separate law.

Who Is Affected?

You may face a tax bill if you received forgiveness on or after January 1, 2026 through IDR forgiveness (after 20 or 25 years of payments), the restructured SAVE plan, or certain employer repayment assistance above set thresholds. Total and Permanent Disability discharges have historically had more complex treatment, so verify with a tax professional. You are NOT affected if your forgiveness came through Public Service Loan Forgiveness (tax-free), Teacher Loan Forgiveness (separate rules), or death or bankruptcy discharge (generally tax-free).

One important exception: borrowers who established eligibility for forgiveness before the end of 2025 keep tax-free treatment. Keep any dated documentation that confirms your eligibility status.

How Much Could You Owe?

The bill depends on the forgiven amount and your marginal rate, since the cancelled debt is added to your ordinary income. In the 22% bracket with $40,000 forgiven, you would owe roughly $8,800 in extra federal tax, plus state tax if your state taxes forgiven debt. This is the long-warned “tax bomb”: a borrower who makes low IDR payments for 20 years can end up debt-free but facing a five-figure tax bill they never planned for. See our guide on student loan default and repayment.

What Should You Do If Forgiveness Is Coming?

Start saving for the tax bill now. If IDR forgiveness is 1 to 5 years out, estimate your forgiven balance, multiply by your expected marginal rate, and divide by the months until forgiveness. For example, $50,000 forgiven at 22% is about $11,000, or roughly $306 a month set aside over 3 years in a high-yield savings account.

Consider Roth conversions earlier. If forgiveness will spike your income in one year, doing Roth conversions in lower-income years beforehand can smooth your tax picture. This is complex, so work with a tax professional. See our guide on the Roth conversion decision.

Check if insolvency applies. The IRS insolvency exclusion still works: if your total liabilities exceed your total assets at forgiveness, you can exclude some or all of the cancelled debt up to the amount of insolvency by filing IRS Form 982. Many borrowers getting IDR forgiveness after 20+ years of low-income payments qualify for full or partial exclusion.

Do not assume state taxes match federal. Some states keep their own exemption even though the federal one expired, so check your state’s rules (California, for instance, has had its own exclusion).

What If Forgiveness Already Happened in 2026?

- Adjust your withholding by updating your W-4 to cover the expected liability for the rest of the year.

- Make estimated tax payments if you have no withholding, to avoid underpayment penalties.

- Set up an IRS payment plan if you cannot pay in full; interest accrues but penalties drop once a plan is in place.

- Consult a tax professional on the insolvency calculation and state rules before filing.

See our guide on estimated taxes.

Is PSLF Still Tax-Free?

Yes. Public Service Loan Forgiveness remains completely tax-free. If you work for a qualifying government agency or nonprofit and pursue PSLF, your forgiveness after 120 qualifying payments is not subject to federal income tax, and the 2026 change does not touch it. If you are on an IDR plan and could qualify for PSLF, it may be worth exploring a switch, both to get forgiveness faster (10 years versus 20 to 25) and to avoid the tax bill entirely.

This is also why your repayment plan matters: see PSLF in 2026 and how RAP handles its 30-year forgiveness, plus the full student loan changes in 2026 hub.

FAQ

Is student loan forgiveness taxable in 2026?

Federally, yes for IDR forgiveness, because the 2021-2025 tax exemption expired and was not extended. The forgiven amount is added to your ordinary income. PSLF remains tax-free.

How much tax will I owe on forgiven student loans?

Roughly your marginal rate times the forgiven amount, plus any state tax. At 22% on $40,000 forgiven, that is about $8,800 federally, though the insolvency exclusion may reduce or eliminate it.

How can I avoid the student loan tax bomb?

Pursue PSLF if eligible (tax-free), claim the insolvency exclusion on Form 982 if your liabilities exceed your assets, and check whether your state still exempts forgiveness. Otherwise, save for the bill in advance.

Does PSLF have a tax bomb?

No. Public Service Loan Forgiveness is permanently tax-free, so borrowers who reach forgiveness through PSLF owe no federal income tax on the cancelled balance.

Bottom Line

Starting in 2026, IDR student loan forgiveness is taxable again, so a forgiven balance can mean a surprise five-figure tax bill, but PSLF stays tax-free and the insolvency exclusion protects many borrowers. If forgiveness is near, estimate the bill and save now, and talk to a tax professional about insolvency and state rules. To go deeper, see our guides on student loan default, the Roth conversion decision, and estimated taxes.

This article is for educational and informational purposes only and does not constitute tax advice. Consult a qualified tax professional before making decisions about student loan forgiveness tax liability, and confirm current rules at irs.gov.