Credit utilization is the percentage of your available credit you are using, and it makes up about 30% of your FICO score, the second biggest factor after payment history. It is also the fastest factor to change: paying down balances can lift your score within a single billing cycle. The common advice is to stay under 30%, but under 10% is meaningfully better. Here is exactly how it works, the thresholds that matter, and the statement-date timing trick most people miss.

Key Takeaways

- Utilization is about 30% of your FICO score and the fastest factor to improve.

- Under 30% is a floor, under 10% is the real target for maximizing your score.

- Pay before the statement closing date, not just the due date, to report a lower balance.

- It has no memory, so a high month does not haunt you once you pay it down.

What Is Credit Utilization?

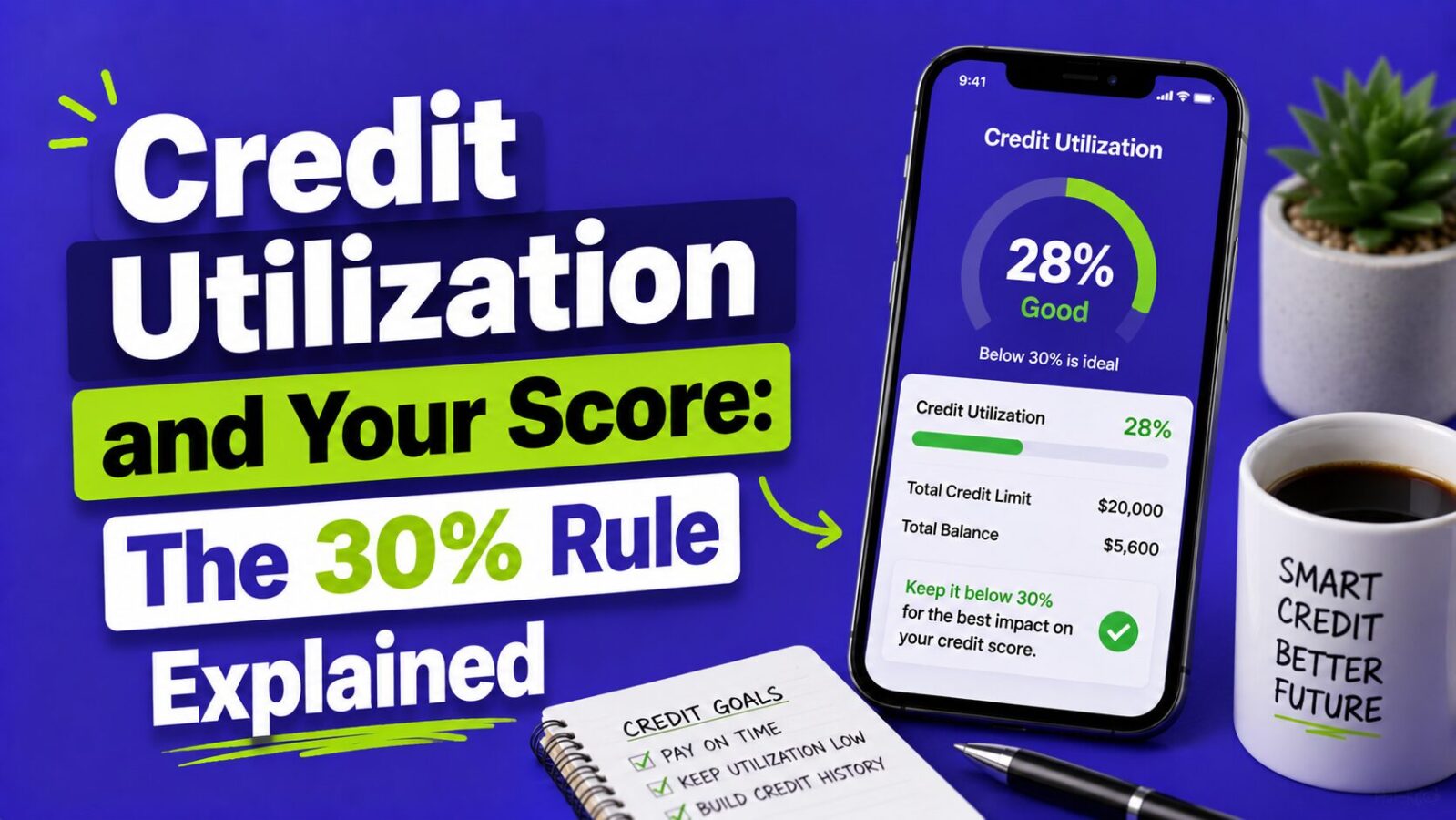

Credit utilization is your total card balances divided by your total card limits. Three cards with a combined $10,000 in limits and $3,000 in balances put you at 30% utilization. It is measured two ways, and both matter:

- Overall utilization: all balances divided by all limits combined.

- Per-card utilization: each card’s balance divided by its own limit.

A single maxed-out card can hurt even if your overall utilization is low, so keep an eye on both numbers.

What Utilization Thresholds Matter?

| Utilization level | Score impact |

|---|---|

| Under 10% | Optimal, maximizes your score on this factor. |

| 10-29% | Good, minor negative impact. |

| 30-49% | Noticeable negative impact begins. |

| 50-74% | Significant negative impact. |

| 75-89% | Serious negative impact. |

| 90-100% | Severe, signals financial distress to scoring models. |

The “under 30%” guideline is a floor, not a target. Under 10% is meaningfully better than 29%, so if maximizing your score is the goal, aim for single-digit utilization. See our guide on how your credit score is calculated.

What Is the Statement Date Timing Trick?

Most people do not realize when utilization gets reported. Your issuer reports your balance to the bureaus on your statement closing date, the last day of your billing cycle, which is usually a few weeks before your payment due date.

If you pay in full on the due date, your reported balance may still be high, because it was captured at statement close before you paid. To report a lower balance, pay the card down before the statement closing date, not just before the due date.

For example, if your statement closes on the 15th and payment is due the 10th of the next month, carrying a $2,000 balance through the 14th means $2,000 gets reported, even if you pay it off by the due date. Pay it down before the 15th and a smaller balance is reported.

How Do You Lower Utilization Without Paying Down Debt?

- Request a credit limit increase. Doubling a limit halves your utilization with no change in behavior. A $2,000 balance on a $4,000 limit is 50%; on an $8,000 limit it is 25%. Ask for a soft-pull increase if possible.

- Open a new card. Added available credit lowers overall utilization. This triggers a hard inquiry with a small, temporary score effect, but the utilization benefit can outweigh it. Skip this if you will run up the new card.

- Become an authorized user. Being added to someone’s high-limit card adds their available credit to your calculation, lowering your overall percentage.

For more on inquiries, see our guide on soft vs hard inquiries.

Why Does Utilization Reset Every Month?

Unlike late payments, which stay on your report for seven years, utilization has no memory. It reflects your current balance as of your most recent statement close, so pay down balances this month and your score reflects the improvement next month. That is exactly why utilization is the fastest lever you can pull. See our guide on how to improve your credit score fast.

FAQ

What is the 30% credit utilization rule?

It is the guideline to keep your card balances under 30% of your limits. That is a floor, though; under 10% is meaningfully better for your score if you want to maximize this factor.

Should I pay my card before the statement date or the due date?

Pay before the statement closing date to lower the balance that gets reported. Still pay at least the minimum by the due date to avoid a late mark. Ideally, pay in full at both points.

Does 0% utilization hurt my credit score?

Reporting a tiny balance (a few percent) can score slightly better than reporting exactly 0% across all cards, because it shows active, responsible use. The difference is small, so do not stress over it.

How fast does lowering utilization raise my score?

Usually within one to two billing cycles, since utilization updates each time your balance is reported. It is the fastest-moving factor in your score, though the exact change varies by profile.

Bottom Line

Credit utilization is about 30% of your FICO score and the fastest factor to change, so keep balances low and pay before the statement closes to report a small number. Aim for single digits, raise your limits to help, and remember that utilization resets monthly with no lasting memory. To go deeper, see our guides on how your credit score is calculated, how to improve your score fast, and soft vs hard inquiries.

This article is for educational and informational purposes only and is not financial advice. Credit scoring is individual, and the effect of utilization varies by your unique profile. Review your reports for free at annualcreditreport.com.