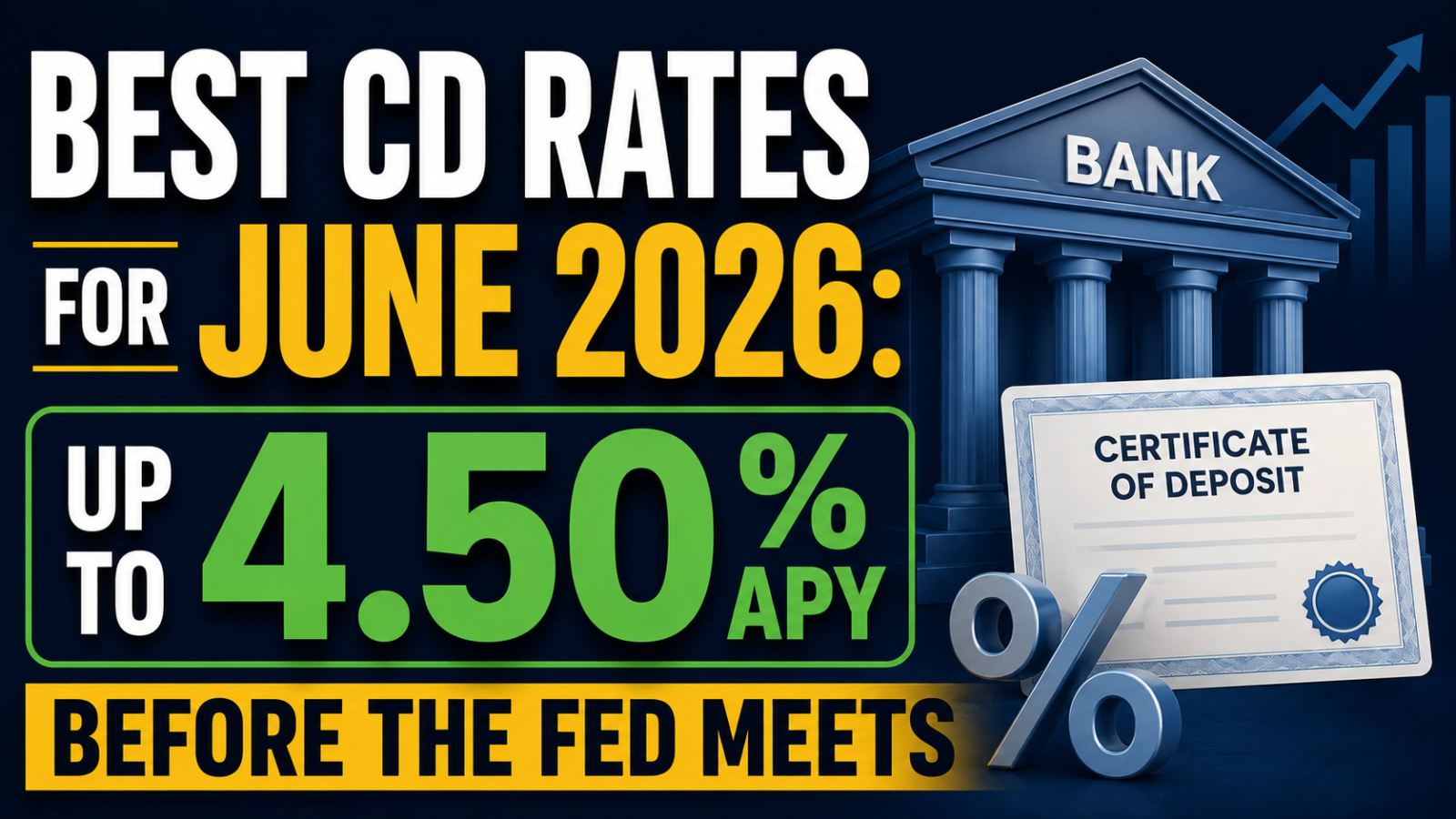

CD rates remain strong heading into June 2026, with the best 6-month CDs paying up to 4.50% APY and top 12-month CDs at 4.10% to 4.25% APY. The Federal Reserve is expected to hold rates at its June 16-17 meeting — new Fed Chair Kevin Warsh’s first — which means the current rate environment persists at least through summer. But rate cuts are likely later in 2026, making this a valuable window to lock in today’s rates on longer-term CDs.

Best CD Rates June 2026

| Term | Top APY Available | Best For |

|---|---|---|

| 3-month | 4.30%-4.50% | Short-term parking, maximum flexibility |

| 6-month | 4.25%-4.50% | Best risk/reward before possible rate changes |

| 12-month | 4.10%-4.25% | Lock in today’s rates through mid-2027 |

| 18-month | 3.90%-4.10% | Moderate rate protection with medium term |

| 24-month | 3.75%-4.00% | Avoid — lower rate, more exposure to rate rise risk |

| 5-year | 3.50%-3.80% | Only if you need guaranteed rate for full 5 years |

Rates as of late May 2026 from online banks and credit unions. Rates change frequently — verify directly with the institution before opening. Top rates typically require online-only banks (Ally, Marcus, Synchrony, Discover, LendingClub, Bread Financial, etc.).

Why June Is a Good Time to Lock In a CD

The Fed has held rates at 3.50%-3.75% since early 2026 after cutting three times in late 2025. With inflation running above 3.5% and a new hawkish Fed chair, a rate cut at the June 16-17 meeting is unlikely (97.5% probability of no change, per Polymarket). But cuts are expected later in the year.

When the Fed cuts, HYSA rates drop within days. CD rates typically start falling before the official cut as banks price in expected policy changes. A 12-month CD locked in today at 4.10% stays at 4.10% even if the Fed cuts twice by December. The same cash in a HYSA could be earning 3.50% by year end.

CD Ladder Strategy for June 2026

Rather than putting all savings into one CD term, a ladder splits savings across multiple maturities:

- 25% in a 3-month CD (matures September 2026)

- 25% in a 6-month CD (matures December 2026)

- 25% in a 9-month CD (matures March 2027)

- 25% in a 12-month CD (matures June 2027)

Every quarter, a CD matures and you reinvest at whatever rate is available. If rates fell, your longer-term CDs are still locked in at higher rates. If rates rose unexpectedly, you have money rolling over to capture the higher rate. The ladder hedges both directions.

CD vs HYSA: The June 2026 Decision

Current top HYSA rates (4.20%-4.75%) are similar to or slightly better than current 12-month CD rates. The choice comes down to liquidity:

- Emergency fund and money you might need: keep in HYSA

- Savings beyond 3-6 month emergency fund you won’t need for 6-12 months: consider a CD to lock in today’s rate

- Long-term inflation hedge: consider I Bonds at 4.26% with the 0.90% fixed rate that beats inflation permanently

What to Watch For

The May CPI report on June 10 and the FOMC decision on June 17 are the two events that could move CD rates in June. A surprise low inflation print (below 3%) could accelerate rate cut expectations and cause CD rates to fall before the meeting even happens. A hot print above 4% reinforces the current environment. Either way, locking in a 6 or 12-month CD before June 17 is the safer move for anyone sitting on cash above their emergency fund.

Savings Goal Calculator

Rates sourced from bank websites and rate aggregators as of late May 2026. Rates change frequently — verify before opening. All deposits at FDIC-insured institutions are insured up to $250,000 per depositor per bank. This article is for informational purposes only.