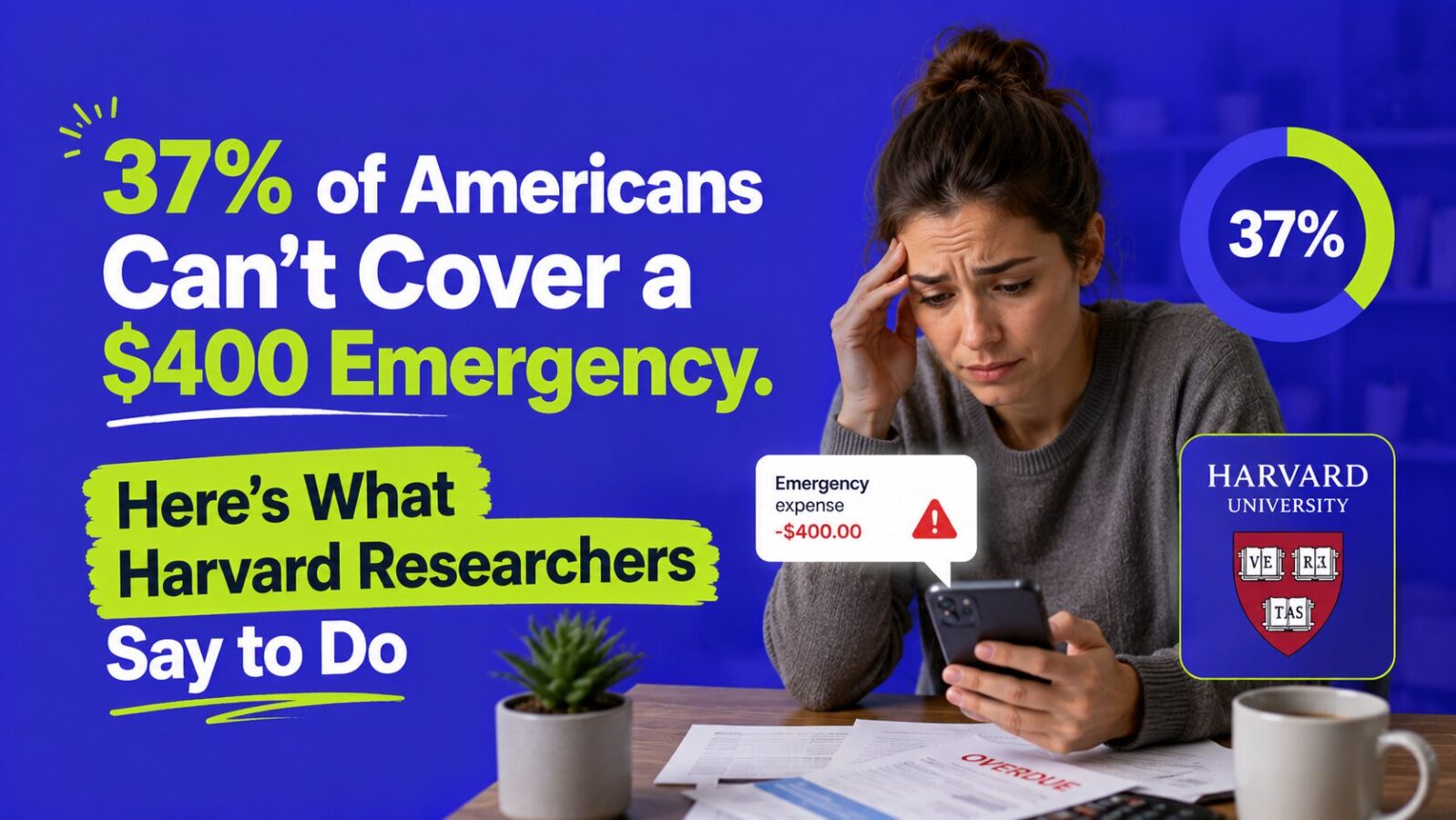

About 37% of Americans could not cover a $400 emergency with cash, savings, or a paid-in-full credit card, according to Federal Reserve data cited in a 2024 NBER paper from Harvard and Yale researchers. For most people under 40 the picture is even worse, with a quarter of every age group holding negative liquid net worth. The research also pinpoints the one thing that actually fixes it: automation. Here is what the data shows and exactly what to do.

Key Takeaways

- 37% can’t cover a $400 emergency, and a quarter of every age group has negative liquid net worth.

- Willpower is not the fix; when saving is opt-in, fewer than 1% of people opt in.

- Automation is what works: people who automate savings keep saving, 87% a year later.

- Build it in tiers: a $1,000 to $1,500 buffer first, then one to two months of essentials.

What Do the Real Numbers Show?

The NBER paper used the Federal Reserve’s Survey of Consumer Finances to calculate liquid net worth, counting only cash, checking, savings, and brokerage balances minus liquid debts like credit cards. That is the money you can actually reach in a day or two. The findings are stark: median liquid net worth is about $1,427 for ages 21 to 30 and just $956 for ages 31 to 40, and for every age group the 25th percentile is negative, meaning a quarter have more liquid debt than savings. The median does not clear $5,000 until ages 61 to 70. Against that, a car repair runs $500 to $1,500 and an ER visit can run $2,000 to $3,000, so for the median person under 40, one event means draining all savings or turning to ~21% credit card debt.

Why Don’t People Save Even When They Want To?

It is not a lack of information or intention; most people know they should and mean to. The obstacle is choice architecture, the default structure of how decisions are made. When saving requires an active choice, most people do not make it, not from irresponsibility but because active decisions take mental bandwidth that daily life already consumes, so inertia defaults to spending. The researchers proved it: they offered a free, fully liquid, employer-promoted payroll savings account, and fewer than 0.7% of eligible employees ever activated one. When saving is opt-in, almost no one opts in.

What Actually Works? Remove the Decision

The flip side is the key: among the few who did sign up, 87% were still saving automatically a year later. The decision that works is the one you make only once. This mirrors decades of 401(k) research, where automatic enrollment produces far higher participation than opt-in. Set up an automatic transfer from checking to savings that fires on payday, before you can spend the money, and saving becomes the default with inertia working for you instead of against you. You are not changing your discipline, you are changing the structure so the easy path is the right path. See our guide on the best high-yield savings accounts.

How Much Do You Actually Need?

Three to six months of expenses is the right target, but the number can paralyze people into not starting, so think in tiers. A first-tier buffer of $1,000 to $1,500 covers most single emergencies (a car repair, a medical copay, a broken appliance) and alone would put you in the top half of the 21-to-30 age group by liquid net worth. A second-tier buffer of one to two months of essential expenses covers income disruptions like job loss, and you build it after the first tier. See our guide on how much to save.

Use this calculator to set your specific target:

Emergency Fund Calculator

Where Should You Keep It?

The account matters almost as much as the amount. The researchers note that a separate, dedicated account (distinct from checking) helps you avoid spending it, a mental-accounting effect where earmarked money feels different. For most people a high-yield savings account is the right vehicle: fully liquid, FDIC insured, and earning far more than checking. Look for no minimum balance, no monthly fees, and easy transfers back to checking within one to three business days. For a true emergency, three days is fast enough; for non-emergencies, that slight friction helps prevent raiding the fund.

What If Your Employer Offers Payroll Savings?

Use it, because payroll deduction happens before the money reaches your checking account, and you cannot spend what you never see. Even without a formal program, most U.S. employers let you split your direct deposit across accounts, the DIY version of what the researchers studied: open a dedicated savings account and ask payroll to send a fixed amount there each pay period, with the rest to checking. You will not notice the savings, which is exactly the point.

Use this calculator to plan your timeline to a goal:

Savings Goal Calculator

FAQ

How many Americans can’t cover a $400 emergency?

About 37%, per Federal Reserve data, could not cover it with cash, savings, or a paid-in-full card. For people under 40 it is often worse, with a quarter holding negative liquid net worth.

Why is it so hard to build an emergency fund?

Because saving is usually opt-in, and inertia defaults to spending. In the research, fewer than 0.7% of people activated a free savings account when it required an active choice.

What is the best way to build emergency savings?

Automate it. Set a transfer to a separate high-yield savings account on payday before you can spend it. The few who automate keep going (87% a year later); manual savers mostly do not.

How much emergency savings do I need?

Start with a $1,000 to $1,500 buffer for single emergencies, then build to one to two months of essential expenses, working toward the three-to-six-month target over time.

Bottom Line

The emergency-savings gap is huge, but the fix is not willpower, it is automation: set up a recurring transfer to a separate high-yield account on payday and let inertia work for you. Start with any amount you can spare, build a $1,000 to $1,500 buffer first, then bump it $25 to $50 every few months toward a few months of expenses. To go deeper, see our guides on the best high-yield savings accounts, how much to save, and getting out of debt.

This article summarizes research for general educational purposes and is not financial advice. The savings experiment was conducted at UK firms; the U.S. savings figures come from Federal Reserve survey data cited in the paper.