If you carry a $3,000 balance on a credit card with 24% APR, you are paying roughly $2 in interest every single day. Not per month. Per day. That is $60 a month, $720 a year — just in interest charges on top of whatever you originally spent.

Most people have no idea how the math actually works. They see “24% APR” on their statement and assume that means they owe 24% of their balance once a year. It does not. Credit card interest is calculated daily, compounds monthly, and is specifically designed to grow faster than minimum payments can shrink it.

This guide breaks down exactly how credit card interest is calculated, shows you the real numbers on common balances, and gives you an interactive calculator so you can run the math on your own situation right now.

Quick Answer

How credit card interest is calculated:

- Divide your APR by 365 to get your Daily Periodic Rate (e.g., 24% APR = 0.0658% per day)

- Multiply by your average daily balance for the billing cycle

- Multiply by the number of days in the billing cycle (usually 28 to 31)

- That total is the interest charge added to your next statement

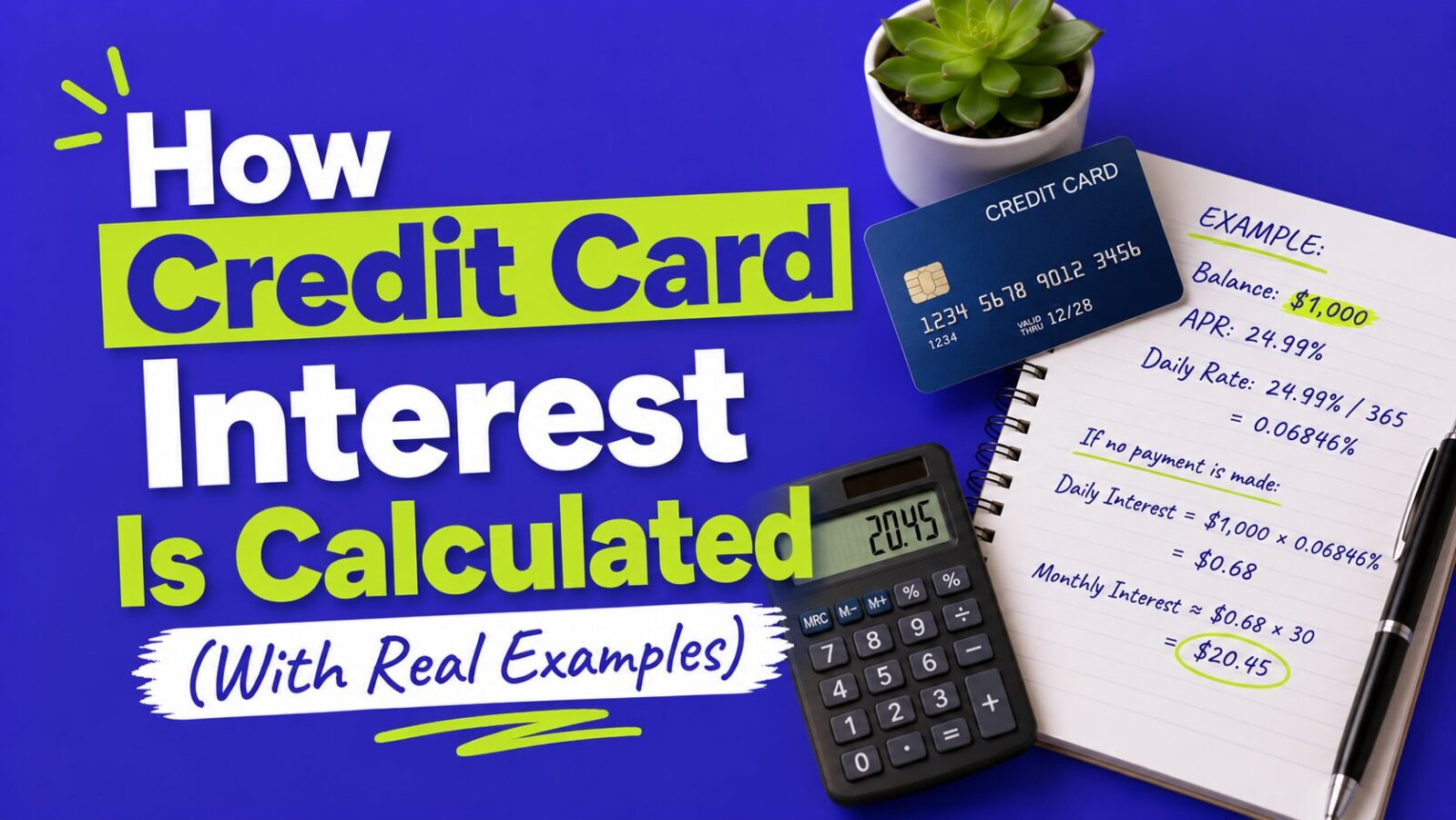

Real example: $3,000 balance at 24% APR = $0.0658% daily rate = $1.97/day = $59.18/month in interest.

Step 1: Understand Your APR

APR stands for Annual Percentage Rate. It is the yearly interest rate on your credit card balance. Common APRs in 2026 range from about 18% on the low end to 29% or higher on the high end, depending on your credit score and the card.

Here is the thing that catches most people off guard: even though APR is expressed as a yearly number, your credit card does not charge you once a year. It charges you every single day.

To find out how much interest you owe per day, credit card companies do one simple calculation:

Daily Periodic Rate Formula

Daily Rate = APR ÷ 365

Real examples:

- 18% APR: 18 ÷ 365 = 0.0493% per day

- 22% APR: 22 ÷ 365 = 0.0603% per day

- 24% APR: 24 ÷ 365 = 0.0658% per day

- 28% APR: 28 ÷ 365 = 0.0767% per day

Those percentages look tiny. That is the trick. They are tiny per day — but they are also relentless. They apply every single day, including weekends and holidays, whether you make a purchase or not.

Step 2: Calculate Your Average Daily Balance

Credit card companies do not just look at your balance on one day and call it done. They track your balance every single day of your billing cycle, then average those daily balances together. That average is called your Average Daily Balance, and it is what the daily interest rate gets applied to.

Here is why that matters: if you make a big purchase on day 5 of your billing cycle, your balance is higher for the remaining 25 or so days of the cycle. All of those days count toward your average.

A Real Example of Average Daily Balance

Let’s say your billing cycle is 30 days. Here is what happens to your balance:

- Days 1 to 10: balance is $1,500 (you had this balance carried over from last month)

- Day 11: you buy a $1,000 laptop, so balance jumps to $2,500

- Day 20: you make a $300 payment, so balance drops to $2,200

- Days 20 to 30: balance stays at $2,200

Your average daily balance:

- Days 1 to 10: $1,500 x 10 = $15,000

- Days 11 to 19: $2,500 x 9 = $22,500

- Days 20 to 30: $2,200 x 11 = $24,200

- Total: $61,700 ÷ 30 days = $2,057 average daily balance

Even though your balance was $1,500 at the start of the month, the laptop purchase partway through pushed your average up to $2,057. That higher number is what interest gets calculated on.

Step 3: Calculate Your Monthly Interest Charge

Now put it all together. The formula your credit card company uses:

Monthly Interest Formula

Interest = Average Daily Balance × Daily Rate × Days in Billing Cycle

Let’s Run the Real Numbers

Scenario: $3,000 balance, 24% APR, 30-day billing cycle

- Daily rate: 24 ÷ 365 = 0.06575%

- Daily interest: $3,000 × 0.0006575 = $1.97

- Monthly interest: $1.97 × 30 = $59.18

That is $59.18 added to your balance in a single month just from interest. Not from any new purchases — purely from the cost of carrying the existing balance.

Scenario: $5,000 balance, 24% APR, 30-day billing cycle

- Daily interest: $5,000 × 0.0006575 = $3.29

- Monthly interest: $3.29 × 30 = $98.63

Scenario: $1,200 balance, 28% APR, 30-day billing cycle

- Daily rate: 28 ÷ 365 = 0.07671%

- Daily interest: $1,200 × 0.0007671 = $0.92

- Monthly interest: $0.92 × 30 = $27.62

Interactive Calculator

See Exactly What Your Balance Is Costing You

Enter your current balance and APR to see your daily, monthly, and annual interest cost — plus how long it takes to pay off at different payment levels.

The Minimum Payment Trap: A Real Example That Will Make You Angry

Here is the most important thing you can understand about credit card interest: minimum payments are designed to keep you paying for as long as possible.

Let’s use a concrete example. You have a $4,000 balance on a card with 22% APR. Your minimum payment is 2% of the balance, or $25, whichever is greater.

At the start, your minimum payment is roughly $80 per month.

Here is what happens over time if you only pay the minimum:

- Month 1: Balance $4,000. Interest charge: $73.33. Minimum payment: $80. Only $6.67 actually reduces your balance. Balance after payment: $3,993.33.

- Month 6: Balance around $3,960. Monthly interest: $72.60. You have paid $471 in six months and reduced your balance by only $40.

- Month 12: Balance around $3,920. You have paid roughly $930 over the year — and still owe $3,920. You are essentially paying $78/month in rent on your debt and barely moving the needle.

The brutal math: paying only the minimum on a $4,000 balance at 22% APR takes approximately 19 years to pay off and costs over $4,500 in interest — more than the original balance you spent.

You end up paying $8,500+ for $4,000 worth of purchases. The credit card company makes more money from your balance than you spent on things you actually bought.

What Happens When You Pay More

The flip side is equally dramatic. Here is what the same $4,000 balance at 22% APR looks like with different monthly payments:

| Monthly Payment | Months to Pay Off | Total Interest Paid | Total Cost |

|---|---|---|---|

| Minimum only (~$80) | ~228 months (19 yrs) | $4,529 | $8,529 |

| $150/month | 37 months (3.1 yrs) | $1,491 | $5,491 |

| $200/month | 26 months (2.2 yrs) | $1,001 | $5,001 |

| $300/month | 17 months (1.4 yrs) | $611 | $4,611 |

| $500/month | 9 months | $340 | $4,340 |

Going from minimum payments to $300 per month saves you over $3,900 in interest and 17 years of your life. Going to $500 per month saves nearly $4,200 in interest. The math is almost shocking once you see it laid out.

Use our credit card payoff calculator to run these numbers on your exact balance and APR.

The Grace Period: How to Pay Zero Interest Every Month

Here is the good news that most people do not know: if you pay your full statement balance every month before the due date, you pay zero interest. None. The 24% APR on your card is completely irrelevant.

This works because of the grace period — the window between your statement closing date and your payment due date, typically 21 to 25 days. During this window, no interest accrues on purchases from the previous billing cycle if you pay the full balance.

How the Grace Period Works With a Real Example

Let’s say your billing cycle runs from October 1 to October 31. You spend $1,200 on purchases during October. Your statement closes on October 31 and your payment due date is November 22.

- If you pay the full $1,200 by November 22: You owe $0 in interest. You just used your credit card like a free 30-to-52-day loan.

- If you pay only $1,000 by November 22: Your $200 remaining balance immediately starts accruing interest at your card’s daily rate. And here is the kicker: you also lose the grace period for next month’s purchases until you pay your balance in full again.

That last point is critical. Once you carry a balance — even a small one — you start paying interest on new purchases from the day you make them, with no grace period. This is how people end up paying interest on groceries they bought yesterday.

The $200 Mistake That Cost $340

Here is a real scenario. Someone has a card with 24% APR and a $1,500 statement balance. They pay $1,300, figuring $200 is not a big deal. Here is what actually happens:

- The $200 remaining balance starts accruing interest at $0.0658% per day

- Next month they charge another $800 in groceries and gas

- Those new purchases immediately accrue interest too — no grace period

- Total balance: roughly $1,015 (the $200 plus $800 plus some interest)

- Monthly interest: about $20.21

What started as “no big deal, just $200” turned into a compounding interest situation on over $1,000. Paying in full every month is the only way to completely stop this cycle.

How APR Affects Different Balance Amounts: Side-by-Side

Here is a quick reference for how much interest different balances cost per month at common APRs. This is pure monthly interest, assuming no payments and no new purchases.

| Balance | 18% APR | 22% APR | 24% APR | 28% APR |

|---|---|---|---|---|

| $500 | $7.50 | $9.17 | $10.00 | $11.67 |

| $1,000 | $15.00 | $18.33 | $20.00 | $23.33 |

| $2,500 | $37.50 | $45.83 | $50.00 | $58.33 |

| $5,000 | $75.00 | $91.67 | $100.00 | $116.67 |

| $8,000 | $120.00 | $146.67 | $160.00 | $186.67 |

| $12,000 | $180.00 | $220.00 | $240.00 | $280.00 |

Look at the $5,000 row at 24% APR: $100 every month just in interest. If your minimum payment is $125, only $25 of it is actually paying off your debt. The other $100 is gone — it pays for the privilege of owing money.

Penalty APR: The Interest Rate Nobody Talks About

Most credit cards have a regular APR (the one advertised) and a Penalty APR — a much higher rate triggered by specific events. Common triggers:

- Missing a payment by 60 days or more

- A returned payment (bounced check or failed ACH)

- Exceeding your credit limit (less common now)

Penalty APRs are commonly 29.99% to 31.49%. Once triggered, they typically apply to your entire existing balance, not just future purchases. And by law (the CARD Act of 2009), if you miss a payment, your card issuer can apply the penalty rate after 60 days — but they must notify you 45 days in advance before increasing your rate on existing balances.

Real example of the Penalty APR impact:

You have a $6,000 balance at 22% APR ($110/month in interest). You miss a payment and your rate jumps to 29.99% APR. Your monthly interest charge immediately becomes $149.95 — a $40 increase just from missing one payment. If you were already struggling to pay, this makes recovery significantly harder.

Set up autopay for at least the minimum payment to ensure you never trigger a penalty rate. Even if you cannot pay the full balance, protecting your regular APR is worth it.

Cash Advance APR: Even More Expensive Than You Think

If you use your credit card at an ATM to get cash, you are triggering a cash advance — and the rules are much harsher than regular purchases.

- Cash advance APR: Usually 25% to 30%, higher than your regular purchase APR

- No grace period: Interest starts accruing immediately from the moment you take the cash, with no grace period at all

- Cash advance fee: Usually 3% to 5% of the amount withdrawn, charged immediately (minimum $5 to $10)

Real example: You take a $500 cash advance on a card with 28% cash advance APR and a 5% fee.

- Immediate fee: $25

- Daily interest from day one: $500 × (28 ÷ 365) × 0.01 = $0.38 per day

- After 30 days: $500 + $25 fee + $11.51 interest = $536.51 owed on a $500 withdrawal

Cash advances are almost never worth it. If you need cash urgently, exhaust every other option first.

How to Reduce the Interest You Pay

Strategy 1: Pay the Full Balance Every Month

The most effective strategy. Pay in full by the due date every month and you will never pay a cent of interest, regardless of your APR. If you are spending more than you can pay off monthly, the problem is spending, not the interest rate. Our guide on the 50/30/20 budget rule can help you structure spending so full monthly payoff becomes realistic.

Strategy 2: Pay More Than the Minimum

Every extra dollar above the minimum goes directly to reducing your principal. Even $50 extra per month dramatically changes the payoff timeline and total interest paid. Run the numbers in the calculator above to see exactly how much your specific extra payment saves.

Strategy 3: Use a 0% Balance Transfer Card

If you have existing high-interest credit card debt, a 0% intro APR balance transfer card pauses interest for 12 to 21 months, letting every payment go toward the principal. See our breakdown of the best 0% APR credit cards to compare options. There is typically a 3% to 5% transfer fee, but on a $5,000 balance at 22% APR, a $150 transfer fee beats $1,100 per year in interest.

Strategy 4: Target the Highest-APR Debt First

If you have multiple credit cards, put all extra payments toward the one with the highest APR while paying minimums on the rest. This is the debt avalanche method and it minimizes total interest paid. Read our full breakdown of how to pay off credit card debt for all three proven methods.

Strategy 5: Call and Ask for a Lower Rate

This one surprises people: you can simply call your credit card company and ask for a lower APR. If you have been a customer for a while and have a history of on-time payments, issuers will often lower your rate — especially if you mention you have received lower-rate offers from competitors. A 2021 LendingTree survey found that 76% of people who asked for a lower rate got one. It costs nothing to ask.

Frequently Asked Questions

How is credit card interest calculated each month?

Credit card interest is calculated by first dividing your APR by 365 to get your daily rate, then multiplying that by your average daily balance (your balance averaged across every day of the billing cycle), then multiplying by the number of days in your billing cycle. For example: a $3,000 balance at 24% APR in a 30-day cycle generates $3,000 × (24 ÷ 365) × 30 = $59.18 in monthly interest.

When does credit card interest start accruing?

For purchases, interest typically starts accruing after the grace period expires — meaning after your payment due date passes if you did not pay your full statement balance. If you pay in full every month, no interest ever accrues on purchases. For cash advances, interest starts from the day of the transaction with no grace period at all.

Is credit card APR calculated daily or monthly?

Daily. Your APR is divided by 365 to get a daily periodic rate, which applies to your balance every single day. At the end of each billing cycle, the total accumulated daily interest is added to your balance as your monthly interest charge. This is why even a few days of carrying a balance costs money.

What happens if I pay more than the minimum payment?

Everything above the minimum payment reduces your principal directly, which reduces next month’s interest charge, which means more of every future payment goes to principal. It is a positive feedback loop. Paying $50 extra per month does not just save $50 — it saves compounding interest on that $50 for every remaining month of the payoff period. Use the Interest Calculator above to see the exact dollar impact on your balance.

If I have a 0% APR offer, do I still have to make payments?

Yes. During a 0% intro APR period, your minimum monthly payment is still required. Missing it can cancel your 0% offer and trigger the regular APR immediately. During a 0% period, your payments reduce the principal directly since no interest is being added, which is why 0% cards are so powerful for paying down a large purchase or transferred balance.

Why did my balance go up even though I made a payment?

This happens when your payment is less than or equal to the monthly interest charge. For example: if your balance is $5,000 at 24% APR, your monthly interest is $100. If you pay $80, your balance actually grows by $20 despite the payment. You need to pay more than the monthly interest charge just to start reducing the principal. The calculator above shows you exactly whether your current payment is beating your interest charge.

Does paying on the due date vs. earlier in the month matter?

For most people paying in full, no. The interest calculation runs on your average daily balance during the billing cycle, not when in the month you pay. However, if you are carrying a balance, making an early payment in the month lowers your average daily balance for that cycle, which slightly reduces your interest charge. The effect is small but real: paying on day 10 instead of day 30 on a $3,000 balance at 24% APR saves roughly $13 in interest for that cycle.

The Bottom Line

Credit card interest is not complicated once you see it written out — APR divided by 365 gives you a daily rate, applied to your average daily balance, multiplied by the days in your billing cycle. But the numbers it produces are genuinely alarming when you run them on real balances.

A $5,000 balance at 24% APR costs $100 every month just to stand still. Minimum payments on that balance over 19 years cost more in interest than the original debt. And missing one payment can trigger a penalty APR that makes all of it worse.

The way out is straightforward: pay in full when you can, pay more than the minimum when you cannot, target the highest-APR debt first, and consider a 0% balance transfer card to pause the interest clock while you pay down the principal.

Run your own numbers in the calculator above, and use our credit card payoff calculator for a full month-by-month payoff schedule. The math is uncomfortable — but knowing it is the first step to changing it.