If you are 65 or older, you can claim a new $6,000 deduction for 2026, on top of your regular standard deduction. The One Big Beautiful Bill Act created this extra deduction for seniors, worth $6,000 per qualifying person ($12,000 for a married couple where both are 65 or older). You can take it whether you itemize or not, but it phases out at higher incomes and is temporary, running from 2025 through 2028. It is often called “no tax on Social Security,” but that name is misleading. Here is how it actually works. Because tax situations vary, confirm the details with a tax professional.

Key Takeaways

- Seniors 65 and older get a new $6,000 deduction for 2025 through 2028, on top of the standard deduction.

- It is $6,000 per qualifying person, so a couple where both are 65 or older can deduct $12,000.

- You can claim it whether you take the standard deduction or itemize.

- It phases out above $75,000 of income for singles and $150,000 for married couples.

- It is not a Social Security tax exemption, despite the “no tax on Social Security” label.

What is the $6,000 senior deduction?

The senior deduction is a new, temporary deduction created by the One Big Beautiful Bill Act (OBBBA) for taxpayers age 65 and older. It lets each qualifying senior subtract an extra $6,000 from their taxable income for tax years 2025 through 2028. It is separate from, and in addition to, the existing additional standard deduction that people 65 and older already get. For the full set of changes in the law, see our complete OBBBA tax changes guide.

Who qualifies?

You qualify if you reach age 65 on or before the last day of the tax year. The deduction is $6,000 per eligible person, so a married couple where both spouses are 65 or older can claim $12,000, while a couple with one spouse 65 or older claims $6,000.

Two requirements matter. You must include a Social Security number valid for employment on your return, and if you are married, you must file jointly to claim it (married filing separately does not qualify). You can claim the deduction whether you take the standard deduction or itemize.

How does it stack with the standard deduction?

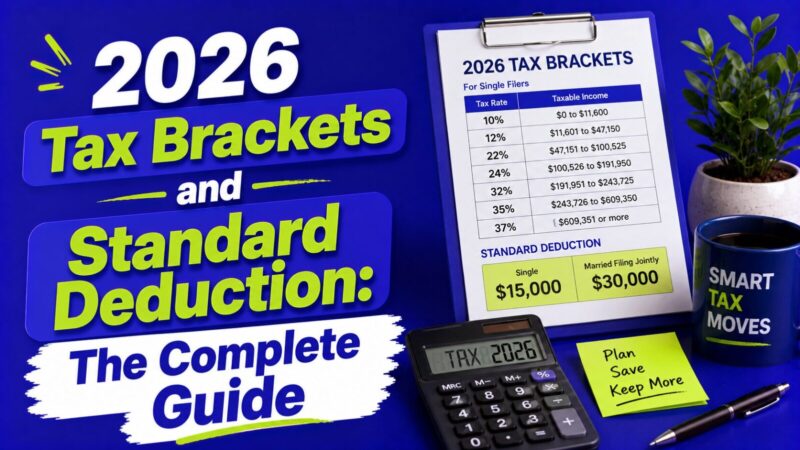

The $6,000 is layered on top of the deductions you already get. For a single 65-year-old in 2026, that means the regular standard deduction ($16,100), plus the existing age-65 additional standard deduction, plus this new $6,000. Together they shelter a meaningful slice of income before any tax applies.

For example, a single 65-year-old with $40,000 of income subtracts the $16,100 standard deduction and the $6,000 senior deduction (plus the smaller age-65 add-on), leaving well under $18,000 of taxable income. At that level, the actual tax owed is small.

What is the income phase-out?

The deduction shrinks as income rises. It begins to phase out once your modified adjusted gross income passes $75,000 for single filers or $150,000 for married filing jointly, dropping by 6% of the amount above the threshold. A single filer’s $6,000 deduction is fully gone by $175,000 of income. For married couples it disappears at higher income levels, depending on whether one or both spouses qualify.

| Filing status | Full deduction up to | Single filer fully phased out at |

|---|---|---|

| Single / head of household | $75,000 MAGI | $175,000 MAGI |

| Married filing jointly | $150,000 MAGI | Higher, based on qualifying spouses |

How much could it actually save you?

Because it is a deduction, not a credit, the cash value depends on your tax bracket. A $6,000 deduction saves you $6,000 times your marginal rate. In the 12% bracket, that is about $720 a year; in the 22% bracket, about $1,320. A couple where both spouses qualify and deduct $12,000 saves roughly $1,440 in the 12% bracket or $2,640 in the 22% bracket.

Those numbers assume you are under the income phase-out and actually owe tax to offset. A senior whose income is already low enough that they owe no federal tax gets no extra benefit, because there is no tax left to reduce. The deduction helps most in the middle: enough income to owe tax, but below the $75,000 or $150,000 phase-out thresholds.

Is this “no tax on Social Security”?

Not exactly, and this is the most common misunderstanding. The deduction was promoted as “no tax on Social Security,” but it does not change the rules for how Social Security benefits are taxed. It is a general deduction against your taxable income, not a carve-out for benefits.

What it does in practice is lower many seniors’ total taxable income, which for some households reduces or eliminates the tax they would otherwise owe, including tax on a portion of their benefits. But the underlying rules that determine how much of your Social Security is taxable, based on your combined income, still apply. Higher-income seniors above the phase-out get no benefit at all, and many lower-income seniors already paid little or no tax on their benefits before this deduction existed.

How long does it last?

The senior deduction is temporary. It applies to tax years 2025 through 2028 and expires after that unless Congress extends it. Because it is short-lived, it is worth claiming each eligible year rather than assuming it will always be there.

How do you claim it?

You claim the deduction on your federal return for each year you are eligible. Tax software will ask your date of birth and income and apply the deduction and any phase-out automatically. If you file by paper, follow the senior deduction line on the form and instructions for the year. Keep it simple: confirm you are 65 by year end, that your income is under the phase-out, and that you are filing jointly if married.

FAQ

How much is the senior deduction for 2026?

$6,000 per qualifying person age 65 or older, or $12,000 for a married couple where both qualify. It is on top of the regular and age-65 standard deductions.

Do I have to itemize to claim it?

No. The senior deduction is available whether you take the standard deduction or itemize.

At what income does it phase out?

It starts phasing out above $75,000 of income for singles and $150,000 for married filing jointly, dropping by 6% of the excess. A single filer’s deduction is fully gone by $175,000.

Does this make Social Security tax-free?

No. It is a general deduction that can lower your overall taxable income, but it does not change how Social Security benefits are taxed. The “no tax on Social Security” label oversimplifies it.

How long will the deduction last?

It applies for tax years 2025 through 2028 and expires after that unless Congress extends it.

Bottom line: The new $6,000 senior deduction gives taxpayers 65 and older an extra deduction for 2025 through 2028, on top of the standard deduction, and a couple where both qualify can claim $12,000. It phases out above $75,000 of income for singles and $150,000 for couples, and despite the marketing, it is a general deduction, not a Social Security tax exemption.

This article is for educational and informational purposes only and is not tax advice. Tax rules and figures change, and how this applies depends on your income and filing status. We want you to feel clear, not overwhelmed, so confirm how the senior deduction affects you with a qualified tax professional, or at irs.gov, before you file.