Most people glance at their pay stub, check the net pay number at the bottom, and move on. If that sounds like you, no judgment. But those other lines on your pay stub are not just noise. They tell you exactly where your money is going, whether your tax withholding is right, and whether you are on track with your retirement contributions.

- Gross pay is before deductions; net (take-home) pay is what actually lands in your account.

- The biggest line items are federal and state income tax withholding plus FICA (7.65%).

- Pre-tax deductions (401k, HSA, health premiums) lower your taxable income.

- If your refund or bill is consistently large, fix it with the IRS Tax Withholding Estimator.

Understanding your pay stub takes maybe 10 minutes of effort, and it can save you hundreds or even thousands of dollars over time. Here is every single line you will see on a typical pay stub so you never have to wonder what any of it means again.

Gross pay vs. net pay: the two numbers that matter most

Gross pay is your total earnings before anything is taken out. If you are salaried, this is your annual salary divided by the number of pay periods (typically 24 for semi-monthly or 26 for biweekly). If you are hourly, it is your hours worked multiplied by your hourly rate, plus any overtime.

Net pay (take-home pay) is what actually hits your bank account after all taxes and deductions are subtracted. The gap between gross and net is where the real story lives.

Example: $60,000 per year paid biweekly = $2,307.69 gross per paycheck. After taxes and deductions, net pay might be $1,650 to $1,750. That $550 to $650 difference is not “disappearing.” Every dollar goes somewhere specific.

Verify your gross pay is correct:

Hourly to Salary Calculator

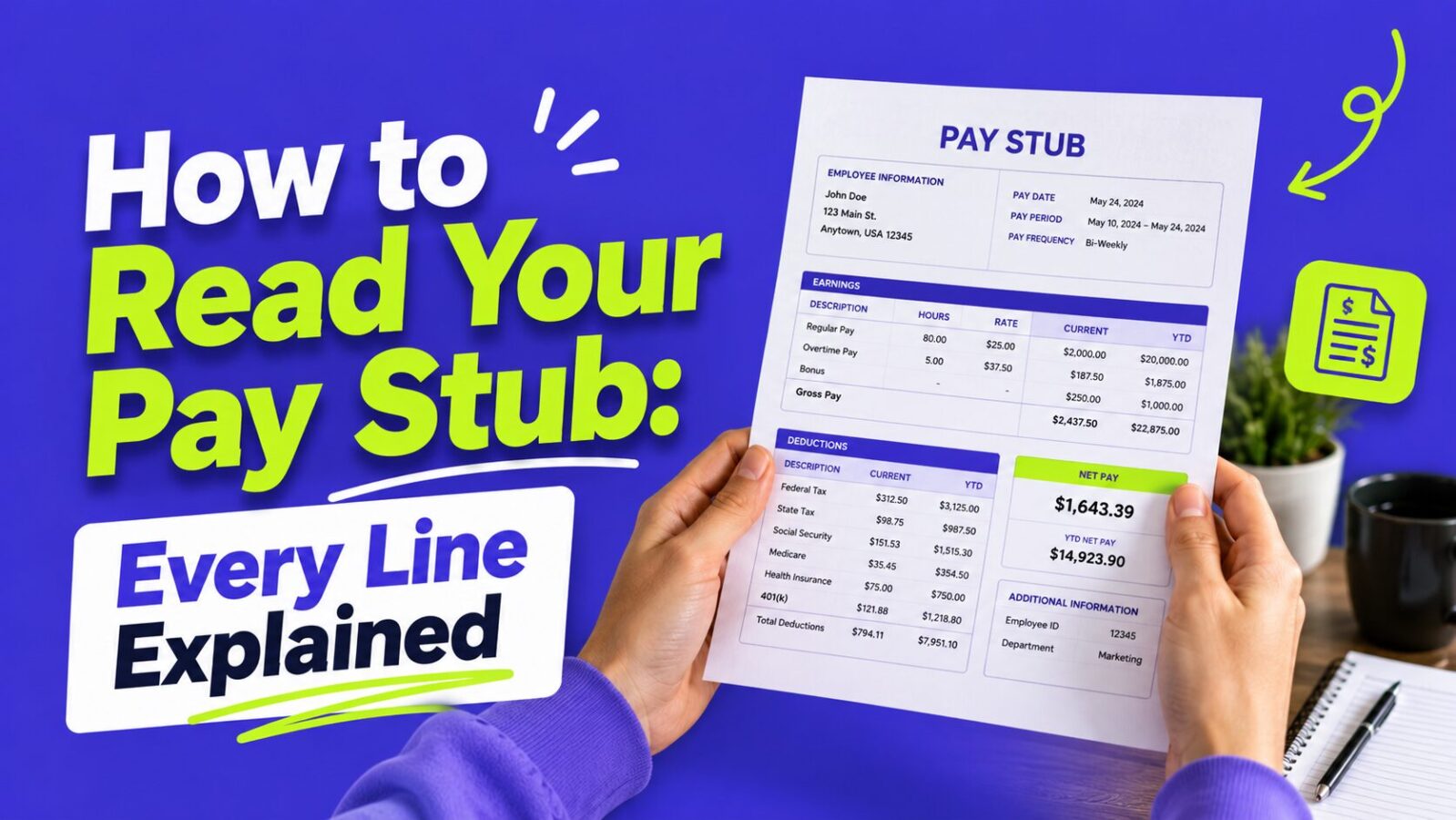

An annotated pay stub example

Here is a simplified pay stub for someone earning $60,000/year, paid biweekly, with a 6% 401(k) contribution and employer-provided health insurance:

| Line item | Current period | YTD |

|---|---|---|

| Gross pay | $2,307.69 | $27,692.28 |

| Federal income tax | -$197.54 | -$2,370.48 |

| Social Security (OASDI) | -$143.08 | -$1,716.96 |

| Medicare tax | -$33.46 | -$401.52 |

| State income tax | -$92.31 | -$1,107.72 |

| 401(k) pre-tax | -$138.46 | -$1,661.52 |

| Health insurance premium | -$85.00 | -$1,020.00 |

| Net pay | $1,617.84 | $19,414.08 |

That is $689.85 taken out of a $2,307.69 paycheck, roughly 30%.

Federal income tax withholding

Usually the largest single deduction. Your employer withholds federal income tax based on the information you provided on your W-4 form when you were hired.

The amount withheld depends on: your filing status (single, married filing jointly, head of household), any adjustments you claimed, and your income level.

Important: the amount withheld each paycheck is an estimate. If they withhold too much, you get a refund. If too little, you owe money in April. More on optimizing this below.

Social Security tax (OASDI)

Listed as “Social Security,” “OASDI,” or “SS” on your pay stub.

Rate: 6.2% of your gross pay. Your employer pays a matching 6.2% on top. There is an annual wage cap (verify the current year’s cap at SSA.gov). Once your year-to-date earnings hit that cap, Social Security tax stops being withheld for the rest of the year.

For our $60,000 example: $2,307.69 x 6.2% = $143.08 per paycheck.

Medicare tax

Rate: 1.45% of gross pay with no income cap. There is an Additional Medicare Tax of 0.9% on earnings above $200,000 (single) or $250,000 (married filing jointly).

For our example: $2,307.69 x 1.45% = $33.46 per paycheck.

Together, Social Security and Medicare are called FICA taxes (Federal Insurance Contributions Act). Combined they take 7.65% of your pay (up to the Social Security wage cap).

State and local taxes

Depending on where you live and work:

- State income tax: Rates vary widely. California and New York have rates above 10% for higher earners. Texas, Florida, and Washington have no state income tax.

- Local/city income tax: Some cities (New York City, Detroit, Philadelphia) levy their own income taxes.

- State disability insurance (SDI): Required in California, New Jersey, New York, and a few others.

Pre-tax deductions

These come out before taxes are calculated on your income, reducing your taxable income. This is a good thing — you pay less in federal (and usually state) income tax.

401(k) or 403(b) contributions

Traditional 401(k) contributions are pre-tax. The money goes directly from your gross pay into your retirement account without being taxed first. You will pay taxes when you withdraw it in retirement.

For our example with 6% contribution rate: $2,307.69 x 6% = $138.46 per paycheck. That $138.46 reduces your taxable income.

If your employer offers a match, make sure you are contributing enough to get every dollar of it. Read our 401(k) guide to see exactly how much you are leaving on the table.

Health Savings Account (HSA)

If you are enrolled in a high-deductible health plan (HDHP), HSA contributions made through payroll are pre-tax and also avoid FICA taxes, making them one of the most tax-efficient savings vehicles available.

Health insurance premiums

Most employer-sponsored health insurance premiums are deducted pre-tax through a Section 125 (cafeteria) plan. Medical, dental, and vision insurance premiums reduce your taxable income.

Flexible Spending Account (FSA)

Healthcare FSA or dependent care FSA contributions are deducted pre-tax. Remember that healthcare FSAs generally have a “use it or lose it” rule (with a small rollover allowance), so do not over-contribute.

Post-tax deductions

These come out after taxes have been calculated. They do not reduce your current taxable income.

Roth 401(k) contributions. If you are making Roth 401(k) contributions, these are post-tax. The money is taxed now, but it grows tax-free and you will not owe taxes on qualified withdrawals in retirement.

Life insurance above $50,000. If your employer-provided life insurance exceeds $50,000, the cost of the excess coverage becomes taxable (called “imputed income”). You might see a small post-tax deduction or addition to your taxable income.

Disability insurance. Short-term and long-term disability premiums may be deducted post-tax. Paying premiums post-tax has an advantage: if you ever use the disability benefit, the payouts would be tax-free.

Wage garnishments. Court-ordered wage garnishments (child support, unpaid debts, student loans in default, tax levies) appear as mandatory post-tax deductions.

Union dues. Union dues are typically deducted post-tax.

YTD totals: your running scorecard

The Year-to-Date (YTD) column shows cumulative totals for the calendar year. Key numbers to track:

YTD Gross Pay. How much you have earned so far this year. Useful for projecting whether you are on track with your annual salary, and for checking if you are approaching the Social Security wage cap.

YTD Federal Tax Withheld. Compare to your expected tax liability to see if you are on track.

YTD 401(k) Contributions. Are you on pace to max out? The 2026 employee contribution limit is $24,500 for those under 50, and $32,500 for those 50 and older ($8,000 catch-up). Verify at IRS.gov/retirement-plans. Divide by the number of pay periods to find your per-paycheck target.

YTD Social Security Tax. Once this reaches the annual wage cap, you will stop seeing this deduction.

Check your YTD totals at least quarterly. They should roughly match the numbers on your W-2 at year end.

How your W-4 affects everything

Your W-4 form is the single biggest lever you have over your federal tax withholding. The current version asks for:

- Filing status (single, married filing jointly, head of household)

- Multiple jobs or spouse works

- Dependents (credits for qualifying children and other dependents)

- Other adjustments (additional income like freelance work, extra withholding per paycheck)

If you have not updated your W-4 since you were hired, or if your life circumstances have changed (married, had a kid, picked up a side gig), your withholding might be off. Use the IRS Tax Withholding Estimator to check.

Common mistakes to watch for

Over-withholding: the interest-free loan to the IRS. If you consistently get a large tax refund, that means you have been over-withholding all year. A $3,000 refund means you gave the IRS an extra $250/month that could have been in a high-yield savings account earning interest. A small refund ($200 to $500) is fine as a buffer. Consistently over $1,000? Adjust your W-4.

Under-withholding: the April surprise. If you owe a large amount at tax time, you are under-withholding. The IRS can charge penalties if you owe more than $1,000 and did not pay at least 90% of your tax liability through withholding or estimated payments.

Not checking your pay stub at all. Payroll errors happen: wrong tax filing status, incorrect retirement contribution percentage, being charged for benefits you did not elect. Review your first pay stub of the year closely, and spot-check at least once per quarter.

Ignoring pre-tax opportunities. If your employer offers a 401(k) match and you are not contributing enough to get the full match, you are leaving free money on the table. Same goes for HSAs and FSAs.

How to check if your withholding is right

A quick 15-minute process:

- Gather your most recent pay stub with YTD totals.

- Go to the IRS Tax Withholding Estimator and enter your information.

- Compare the estimator’s recommendation to your current W-4 settings.

- If adjustments are needed, fill out a new W-4 and submit it to HR or payroll. Changes typically take effect within one to two pay periods.

Especially important if any of these happened this year: got married or divorced, had a child, started a side job or freelance work, bought a home, or had a significant change in income.

For a full walkthrough of the tax filing process, read our beginner tax filing guide.

Putting it all together

Your pay stub is a financial dashboard that tells you:

- How much you actually earn (gross pay)

- How much goes to taxes (federal, state, FICA)

- How much you are saving (retirement contributions, HSA)

- How much you take home (net pay)

- Whether you are on track for the year (YTD totals)

Take 10 minutes this week to pull up your most recent pay stub and go through it line by line using this guide. If something looks off, ask your HR or payroll department. If your withholding needs adjusting, update your W-4 now rather than waiting until tax season.

Your paycheck is the foundation of your entire financial life. You should know exactly what is happening to every dollar before it reaches your bank account.

Now that you understand your pay stub, here are three things worth doing this week:

- Check your 401(k) contribution rate. Are you getting the full employer match? If not, log into your payroll portal today and increase your contribution. Read our maximize your 401(k) guide.

- Check your tax withholding. If you consistently get a large refund or owe a large amount in April, use the IRS Tax Withholding Estimator and update your W-4 today.

- Verify your gross pay. Use the hourly-to-salary calculator above to confirm your current rate matches what you expect, especially if you recently changed hours or got a raise.

Frequently Asked Questions

Gross pay is your total earnings before anything is taken out. Net pay (take-home) is what remains after taxes, FICA, and deductions like health insurance and 401k.

FICA is the payroll tax for Social Security and Medicare, totaling 7.65% of your wages (6.2% Social Security + 1.45% Medicare). Your employer pays a matching 7.65%.

Because of withholding: federal and state income tax, FICA, and pre-tax deductions (retirement, health insurance, HSA) all come out before you are paid.