Open enrollment comes around once a year, and every year millions of Americans stare at the same confusing question: should I sign up for an FSA, an HSA, or neither?

These two accounts sound similar, and they both help you save on healthcare costs using pre-tax dollars. But they work very differently, and choosing the wrong one (or not choosing at all) can cost you hundreds or even thousands of dollars a year in unnecessary taxes and missed savings.

This guide breaks down everything you need to know about FSAs and HSAs — the eligibility rules, contribution limits, tax advantages, rollover policies, and investment potential — so you can make the smartest choice for your health and your wallet.

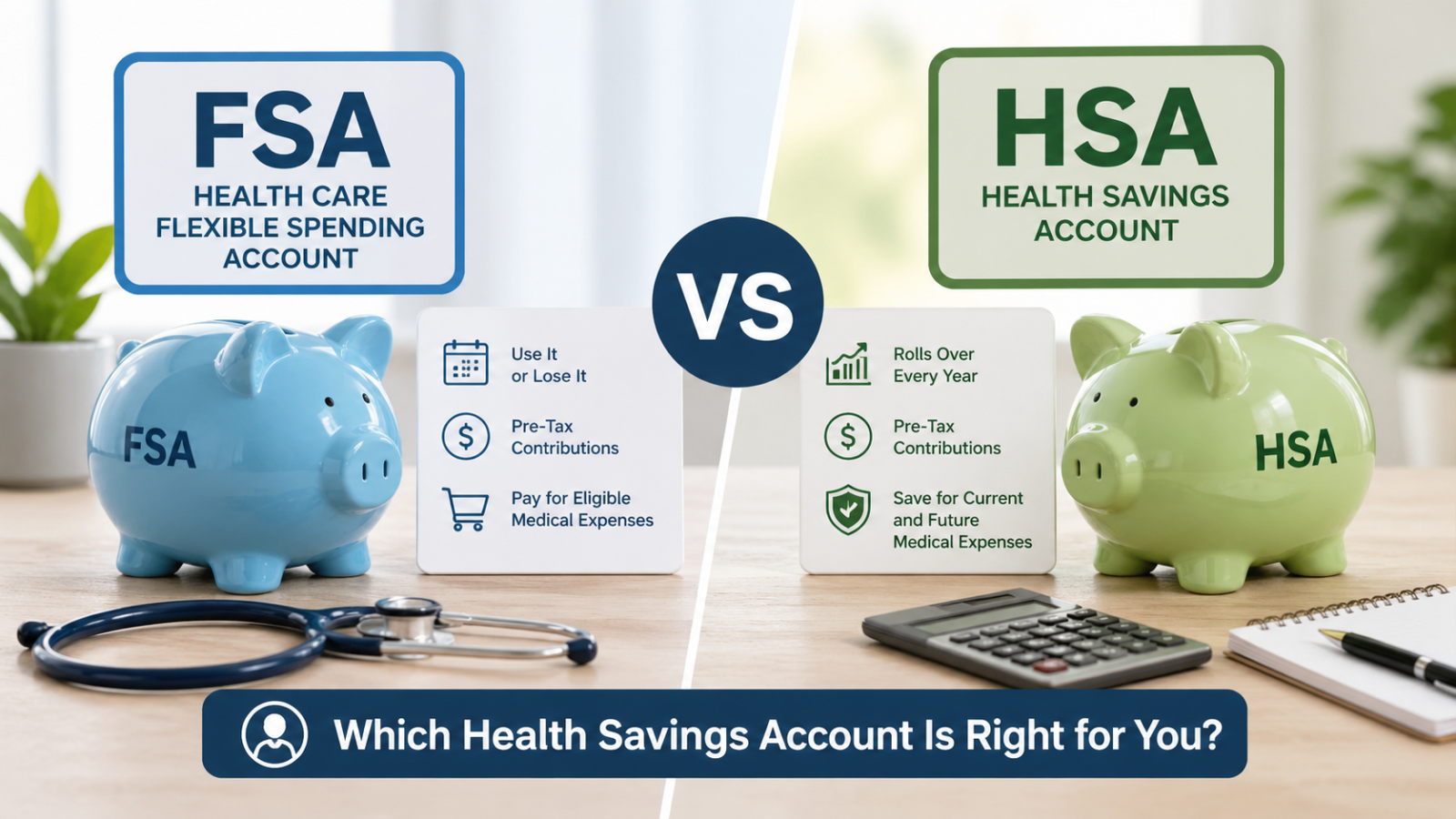

What Is an FSA (Flexible Spending Account)?

A Flexible Spending Account is an employer-sponsored benefit that lets you set aside pre-tax dollars from your paycheck to pay for eligible healthcare expenses. Think of it as a special savings bucket that reduces your taxable income while helping you cover medical costs like copays, prescriptions, glasses, and dental work.

How an FSA Works

- During open enrollment, you decide how much to contribute for the year (up to the IRS limit).

- That amount is divided evenly across your paychecks as a pre-tax deduction.

- Your full annual election is available on day one of the plan year — you don’t have to wait for the money to accumulate.

- You use the funds to pay for qualified medical expenses throughout the year.

- At the end of the plan year, you generally lose any unspent funds (with some exceptions).

Key Features of an FSA

- Employer-sponsored only. You can’t open an FSA on your own; your employer must offer one.

- Pre-tax contributions. Money goes in before federal income tax, Social Security tax, and Medicare tax are calculated.

- Use-it-or-lose-it rule. Unspent funds generally expire at the end of the plan year, though your employer may offer a grace period (up to 2.5 months) or a carryover allowance (up to $660 for 2026).

- Full balance available immediately. If you elect $3,000 for the year, you can spend all $3,000 on January 2 — even though you’ve only had one paycheck deducted.

- No investment option. FSA funds sit in cash. You can’t invest them.

- Tied to your employer. If you leave your job, you typically lose access to remaining FSA funds (though you can use COBRA to continue temporarily).

What Is an HSA (Health Savings Account)?

A Health Savings Account is a tax-advantaged savings account specifically for people enrolled in a High Deductible Health Plan (HDHP). Unlike an FSA, an HSA is yours — it’s a personal account that stays with you regardless of where you work.

How an HSA Works

- You enroll in a qualifying HDHP through your employer or the individual marketplace.

- You (or your employer) contribute pre-tax dollars to your HSA, up to the annual IRS limit.

- You use the funds to pay for qualified medical expenses at any time.

- Unused funds roll over indefinitely — there’s no expiration.

- Once your balance reaches a certain threshold (often $1,000 to $2,000), you can invest the funds in mutual funds, ETFs, and other options.

Key Features of an HSA

- Requires an HDHP. You must be enrolled in a qualifying High Deductible Health Plan. For 2026, that means a plan with a minimum deductible of $1,650 (individual) or $3,300 (family), and a maximum out-of-pocket of $8,300 (individual) or $16,600 (family).

- Triple tax advantage. Contributions are pre-tax, growth is tax-free, and withdrawals for qualified expenses are tax-free. This is the only account in the US tax code with all three benefits.

- Your money, forever. HSA funds roll over year to year. There is no use-it-or-lose-it rule. The account belongs to you, not your employer.

- Portable. Change jobs, retire, become self-employed — your HSA goes with you.

- Investment potential. Most HSA providers let you invest funds once you hit a minimum balance, giving your money the potential to grow over time.

- Available without an employer. While many people open HSAs through work, you can open one independently at a bank or financial institution as long as you have a qualifying HDHP.

FSA vs HSA: Side-by-Side Comparison

| Feature | FSA | HSA |

|---|---|---|

| Eligibility | Must be offered by employer | Must have a qualifying HDHP |

| 2026 Contribution Limit (Individual) | $3,300 | $4,300 |

| 2026 Contribution Limit (Family) | $3,300 (same limit) | $8,550 |

| Catch-Up Contribution (55+) | None | $1,000 additional |

| Tax Benefit on Contributions | Pre-tax (income, FICA) | Pre-tax (income, FICA) |

| Tax-Free Growth | No (not invested) | Yes |

| Tax-Free Withdrawals | Yes, for qualified expenses | Yes, for qualified expenses |

| Rollover | Limited ($660 carryover or 2.5-month grace period, employer chooses) | Unlimited, rolls over forever |

| Investment Options | None | Yes, once minimum balance met |

| Portability | Tied to employer | Fully portable |

| Available Day One | Yes, full annual amount | Only what’s been contributed so far |

| Can Be Used in Retirement | No | Yes (after 65, any purpose with income tax only) |

The Triple Tax Advantage of an HSA (and Why It Matters)

The HSA’s triple tax advantage is often called the best tax break in America, and for good reason. Let’s break it down.

Tax Benefit 1: Pre-Tax Contributions

When you contribute to an HSA, that money comes out before federal income tax, state income tax (in most states), Social Security tax, and Medicare tax. If you’re in the 22% federal bracket and contribute $4,300, you save roughly:

- $946 in federal income tax

- $266 in Social Security tax

- $62 in Medicare tax

- Plus state income tax savings (varies)

That’s over $1,274 in tax savings just from contributing.

Tax Benefit 2: Tax-Free Growth

If you invest your HSA funds, any gains — dividends, interest, capital gains — grow completely tax-free. Compare that to a regular brokerage account where you’d owe taxes on gains every year.

Tax Benefit 3: Tax-Free Withdrawals

When you use HSA funds for qualified medical expenses, you pay zero tax on the withdrawal. No income tax, no capital gains tax, nothing.

The Retirement Angle

After age 65, you can withdraw HSA funds for any purpose — not just medical expenses. If you use the money for non-medical expenses, you’ll pay ordinary income tax (similar to a traditional IRA withdrawal), but there’s no penalty. For medical expenses, withdrawals remain completely tax-free at any age.

This makes the HSA a powerful supplemental retirement account, especially if you can afford to pay medical expenses out of pocket now and let your HSA grow for decades. If you’re already maxing out your 401(k) and IRA contributions, the HSA is the next logical place to put your money.

Eligibility Requirements: Who Can Use Each Account?

FSA Eligibility

- Your employer must offer an FSA as part of their benefits package.

- Almost any employee can participate, regardless of what health insurance plan they have.

- Self-employed individuals cannot open an FSA.

- You can have an FSA alongside most health insurance plans, including PPOs, HMOs, and even HDHPs (with a caveat — see below).

HSA Eligibility

To contribute to an HSA, you must meet all of the following:

- Be enrolled in a qualifying HDHP. The plan must meet the IRS minimum deductible and maximum out-of-pocket thresholds for the year.

- Not be enrolled in Medicare.

- Not be claimed as a dependent on someone else’s tax return.

- Not have other non-HDHP health coverage (with limited exceptions for dental, vision, and certain preventive care).

Can You Have Both an FSA and an HSA?

Generally, no. Having a traditional FSA disqualifies you from contributing to an HSA. However, there are two exceptions:

- Limited Purpose FSA (LPFSA): This special FSA only covers dental and vision expenses. You can have an LPFSA alongside an HSA.

- Post-Deductible FSA: This FSA only kicks in after you’ve met your HDHP deductible. It can also be paired with an HSA, though it’s less common.

If your employer offers an LPFSA, it’s worth considering. You get the full power of your HSA for medical expenses while using the LPFSA to cover dental and vision costs with pre-tax dollars.

Contribution Limits for 2026

FSA Limits

- Maximum contribution: $3,300 per employee

- Carryover maximum: $660 (if your employer offers the carryover option)

- No catch-up contributions for older employees

- Married couples who both have access to FSAs through their respective employers can each contribute the maximum

HSA Limits

- Individual coverage: $4,300

- Family coverage: $8,550

- Catch-up contribution (age 55+): Additional $1,000

- These limits include both your contributions and any employer contributions

If your employer contributes $1,000 to your HSA, you can contribute up to $3,300 more (for individual coverage) to hit the $4,300 cap.

Rollover Rules: The Biggest Difference

This is where the two accounts diverge most dramatically.

FSA Rollover

FSAs follow a “use it or lose it” rule. At the end of the plan year, unspent funds generally disappear. Your employer may offer one of two relief options (but not both):

- Grace period: Up to 2.5 extra months to spend remaining funds.

- Carryover: Roll up to $660 into the next plan year.

This means you need to be relatively precise when estimating your annual healthcare expenses. Contribute too much and you lose money. Contribute too little and you miss out on tax savings.

Strategy tip: If your FSA has a carryover provision, budget conservatively and aim to use most of your balance. Schedule dental cleanings, eye exams, or other planned care before the deadline if you have funds left over.

HSA Rollover

HSA funds roll over indefinitely. There is no deadline, no expiration, and no cap on how much you can accumulate. If you contribute $4,300 every year for 20 years and never spend a dime, you’ll have $86,000 plus investment gains sitting in your account.

This is what makes the HSA uniquely powerful as a long-term savings vehicle. You can let it grow for decades and use it in retirement when healthcare costs tend to be highest.

Investment Options

FSA: No Investment

FSA funds sit in a cash account. They don’t earn interest (or if they do, it’s negligible). Since the money is meant to be spent within the year, there’s no real point in investing it anyway.

HSA: Full Investment Potential

Most HSA providers offer investment options once your cash balance reaches a threshold (typically $1,000 to $2,000). Investment options usually include:

- Index funds

- Target-date funds

- Bond funds

- Individual stocks (at some providers)

The investment lineup varies by provider. Some HSA administrators offer excellent low-cost index funds, while others have limited or expensive options. If your employer’s HSA provider has poor investment choices, you can transfer your HSA to a different provider (like Fidelity, which offers fee-free HSA investing) while still receiving employer contributions to your work HSA.

The optimal HSA strategy for long-term wealth building:

- Contribute the maximum each year.

- Keep enough in cash to cover your deductible (for emergencies).

- Invest everything above that threshold in low-cost index funds.

- Pay current medical expenses out of pocket if you can afford to.

- Save receipts for every medical expense (there’s no time limit on reimbursement).

- Let the investments grow tax-free for years or decades.

- Reimburse yourself later — or use the funds tax-free in retirement.

If you’re interested in learning more about index fund investing, check out our guide on how to get started with index funds.

Qualified Expenses: What Can You Spend the Money On?

Both FSAs and HSAs cover a similar list of IRS-qualified medical expenses, including:

- Doctor visits and specialist copays

- Prescription medications

- Dental care (cleanings, fillings, crowns, orthodontics)

- Vision care (eye exams, glasses, contact lenses)

- Mental health services

- Physical therapy

- Medical equipment (crutches, blood pressure monitors, etc.)

- Sunscreen (yes, really — it’s been eligible since 2020)

- Menstrual products

- COVID tests and related expenses

- First aid supplies

Items that are generally not covered:

- Cosmetic procedures

- Gym memberships (unless prescribed by a doctor for a specific condition)

- General wellness supplements (unless prescribed)

- Health insurance premiums (with exceptions for HSAs — see below)

HSA-Specific Spending Rules

After age 65, HSA funds can be used for:

- Medicare premiums (Parts A, B, C, and D)

- Long-term care insurance premiums (up to age-based limits)

- COBRA premiums

- Health insurance premiums while receiving unemployment benefits

These expanded uses make the HSA even more valuable in retirement.

Which Should You Choose? A Decision Framework

Choose an FSA If:

- Your employer offers an FSA but not an HDHP. If you can’t get an HSA-qualifying plan, the FSA is your only option for pre-tax healthcare savings.

- You have predictable, significant medical expenses. If you know you’ll spend close to the FSA limit on braces, a planned surgery, or ongoing treatment, an FSA lets you access the full amount on day one.

- You prefer lower deductibles. If a high-deductible plan makes you nervous and you’d rather have a traditional PPO or HMO with lower out-of-pocket costs, the FSA pairs well with that choice.

- You need the money upfront. Since the full FSA balance is available from day one, it’s helpful if you have a big expense early in the year.

Choose an HSA If:

- You’re eligible and relatively healthy. If you don’t expect huge medical bills, the HDHP’s lower premiums combined with HSA tax savings can save you money overall.

- You want long-term tax-advantaged savings. The HSA’s triple tax advantage and unlimited rollover make it one of the best savings vehicles in America.

- You can afford to pay some medical expenses out of pocket. The ideal HSA strategy involves paying current expenses from your checking account and letting your HSA grow.

- You’re thinking about retirement. The HSA functions as a supplemental retirement account with unmatched tax benefits for healthcare costs.

- You want portability. If you might change jobs, the HSA stays with you no matter what.

The Math: FSA vs HSA Over Time

Let’s compare two scenarios for a 30-year-old earning $70,000.

Scenario A: FSA

- Contributes $2,500/year to FSA

- Spends all $2,500 on medical expenses each year

- Tax savings: roughly $750/year (30% combined rate)

- After 20 years of tax savings: approximately $15,000

Scenario B: HSA (invest and don’t touch it)

- Contributes $4,300/year to HSA

- Pays $2,500 in medical expenses out of pocket

- Invests remaining $1,800/year in index funds (plus invests the tax savings)

- Tax savings on contributions: roughly $1,290/year

- After 20 years (assuming 7% average returns): HSA balance of approximately $80,000+ in tax-free money

The difference is staggering. The HSA’s ability to invest and compound tax-free over decades creates a massive advantage that the FSA simply cannot match.

Common Mistakes to Avoid

FSA Mistakes

- Over-contributing. Don’t guess high. If you contribute $3,000 and only spend $2,000, you lose $1,000 (minus any carryover). Base your election on actual expected expenses.

- Forgetting the deadline. Mark your calendar for the end of your plan year (and grace period, if applicable). Schedule any remaining appointments before the cutoff.

- Not knowing what’s eligible. Many people miss out on reimbursable expenses because they don’t realize items like sunscreen, bandages, and menstrual products qualify.

- Ignoring the dependent care FSA. If you have kids in daycare, the Dependent Care FSA is a separate account that can save you significant money on childcare expenses. Don’t confuse the two.

HSA Mistakes

- Treating it like a spending account. The HSA’s real power comes from investing and letting it grow. Try to pay current expenses out of pocket when possible.

- Not investing. Many HSA holders leave all their money in cash, missing out on years of tax-free growth.

- Choosing a bad provider. Some HSA providers charge monthly fees or offer expensive investment options. Fidelity, Lively, and others offer low-cost or no-fee HSAs.

- Not saving receipts. You can reimburse yourself from your HSA at any time, even years later. Save every medical receipt. If you pay $500 out of pocket today, you can withdraw $500 tax-free from your HSA in 2040. But you need the receipt to prove it was a qualified expense.

- Using it for non-qualified expenses before 65. Withdrawals for non-medical expenses before age 65 trigger income tax plus a 20% penalty. Don’t do it.

How to Maximize Your Benefits

If You Have an FSA

- Calculate your expected medical expenses carefully during open enrollment.

- Use your employer’s online tools to estimate costs.

- Front-load big expenses (orthodontia, LASIK, etc.) early in the year to take advantage of the full balance.

- Keep a running tally of spending throughout the year.

- In the final months, schedule dental, vision, and wellness appointments to use remaining funds.

- Buy eligible OTC items (first aid kits, sunscreen, pain relievers) if you have leftover balance.

If You Have an HSA

- Contribute the maximum every year.

- If your employer contributes, factor that into your total.

- Open your HSA with a provider that offers low-cost index fund investing.

- Keep 1-2x your deductible in cash for emergencies; invest the rest.

- Pay medical expenses out of pocket when possible.

- Save every receipt in a dedicated folder (digital is fine).

- Consider your HSA as part of your overall retirement planning strategy.

The Bottom Line

Both FSAs and HSAs are valuable tools for reducing your healthcare costs and lowering your tax bill. But they’re not interchangeable.

If you’re eligible for an HSA, it’s almost always the better long-term choice. The unlimited rollover, investment potential, triple tax advantage, and portability make it one of the most powerful financial accounts available to American workers. It’s a savings account, an investment account, and a retirement account all in one.

If an FSA is your only option, it’s still a great way to save money on predictable healthcare expenses. Just be careful not to over-contribute, and make sure you spend down your balance before the deadline.

Whichever account you choose, the worst decision is not using either one. Pre-tax healthcare savings is free money from the government. Don’t leave it on the table.