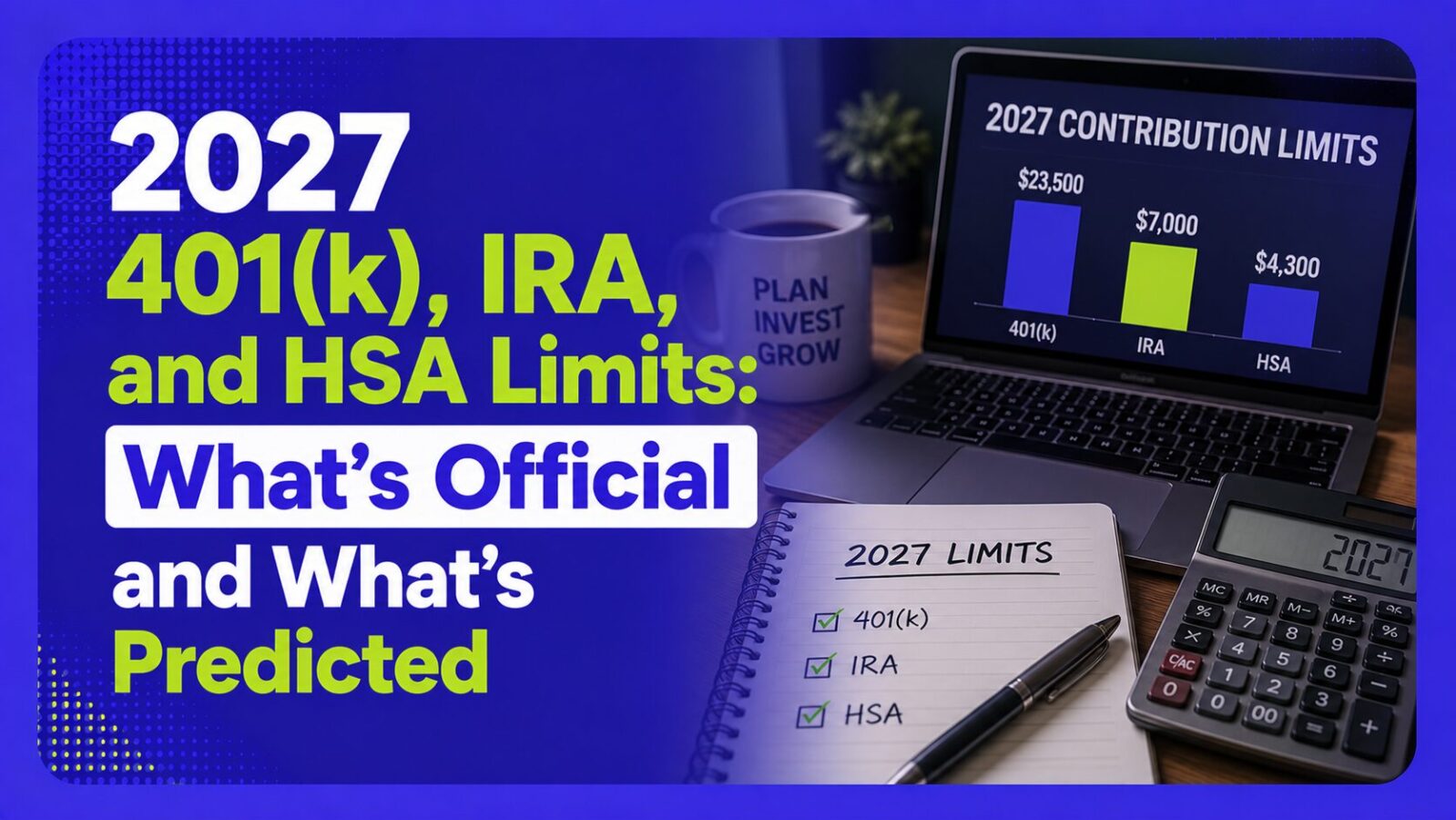

The IRS won’t announce official 2027 401(k) and IRA limits until around November 1, 2026, but 2027 HSA limits are already official: $4,500 for self-only coverage and $9,000 for family coverage, both confirmed in May 2026. For 401(k)s, actuarial firm Milliman’s latest forecast projects the deferral limit rising from $24,500 to $25,000, and the age 60-63 “super catch-up” rising from $11,250 to $11,750. Here’s what’s confirmed, what’s projected, and what it means for your 2027 planning.

Key Takeaways

- 2027 HSA limits are official: $4,500 self-only (up from $4,400), $9,000 family (up from $8,750).

- 2027 401(k)/403(b)/457 limits are projected, not official: Milliman forecasts $25,000, up from $24,500 in 2026.

- The age 60-63 super catch-up is projected to rise from $11,250 to $11,750.

- The IRA limit ($7,500 in 2026) likely won’t increase for 2027, per Milliman, since one year of moderate inflation rarely moves it.

- Official 401(k)/IRA numbers land around November 1, 2026, based on CPI-U through September 2026.

What’s Already Official for 2027?

HSA limits are set on a different, earlier schedule than 401(k) and IRA limits, so the IRS already published them in Revenue Procedure 2026-24 (May 2026):

| Limit | 2026 | 2027 (official) |

|---|---|---|

| HSA, self-only coverage | $4,400 | $4,500 |

| HSA, family coverage | $8,750 | $9,000 |

| HSA catch-up (age 55+) | $1,000 | $1,000 (fixed by statute, doesn’t adjust) |

What’s Only Projected So Far?

401(k), 403(b), 457, IRA, and related limits are calculated from the change in CPI-U over the 12 months ending September 2026, so the IRS can’t finalize them until that data is in. Milliman, an actuarial firm that tracks this every year, publishes running forecasts based on inflation data as it comes in. Its most recent estimate (based on CPI-U through May 2026, up 4.2% year-over-year):

| Limit | 2026 | 2027 (Milliman projection) |

|---|---|---|

| 401(k)/403(b)/457 employee deferral | $24,500 | $25,000 |

| Catch-up, age 50+ (standard) | $8,000 | $8,000 (no change projected) |

| Catch-up, age 60-63 (super catch-up) | $11,250 | $11,750 |

| Traditional/Roth IRA | $7,500 | $7,500 (no change likely) |

| Total annual addition, defined contribution plans | $72,000 | $75,000 |

These are forecasts, not official numbers. They can move if inflation data through September comes in hotter or cooler than expected, the same uncertainty that applies to the 2027 Social Security COLA estimate. Treat them as planning guidance, not numbers to lock into a payroll election yet.

What Should You Do With a Projection, Not a Final Number?

If you’re setting up 2027 payroll deferrals or automatic contributions before the official announcement, don’t lock in the projected max. Most employers open 2027 elections in the last quarter of 2026, after the IRS confirms the real numbers, so there’s little practical need to guess early. What is useful now: if you’re not maxing out your 2026 limit ($24,500, or $35,750 if you qualify for the $11,250 super catch-up), use the months left in 2026 to close that gap, since it doesn’t roll over.

Who Gets the Super Catch-Up?

The enhanced catch-up for ages 60, 61, 62, and 63 started in 2025 under SECURE 2.0. It’s meaningfully higher than the standard 50+ catch-up ($8,000 in 2026) and applies only in the calendar year you turn one of those four ages, reverting to the standard catch-up at 64. If you’re in that four-year window, it’s worth confirming with your plan administrator that it’s applied correctly.

What Are the Key Dates?

- Through September 2026: CPI-U data accumulates that will determine the official 401(k)/IRA figures.

- Around November 1, 2026: IRS typically announces official 2027 retirement plan limits.

- January 2027: New limits take effect for the 2027 plan year.

FAQ

What is the 2027 401(k) contribution limit?

Not official yet. Milliman’s latest forecast (May 2026) projects $25,000, up from $24,500 in 2026, but the IRS won’t confirm the real number until around November 1, 2026.

Are the 2027 HSA limits official?

Yes. The IRS confirmed them in May 2026: $4,500 for self-only HDHP coverage and $9,000 for family coverage, both up from 2026.

Will the IRA limit go up in 2027?

Milliman’s forecast says probably not, the $7,500 IRA limit just increased for 2026 and typically needs more than one year of moderate inflation to move again.

When will the IRS announce official 2027 limits?

Historically around November 1, based on CPI-U data through September of the prior year. Watch for the official IRS notice in early November 2026.

Bottom Line

2027 HSA limits are locked in at $4,500 self-only and $9,000 family, but 401(k) and IRA numbers are still projections, Milliman currently forecasts a $25,000 401(k) deferral limit and a $11,750 super catch-up, with the IRA limit likely holding at $7,500. Use the projections for planning, but wait for the official IRS announcement around November 1, 2026, before finalizing 2027 payroll elections.

A quick note: the 401(k) and IRA figures in this guide are forecasts from Milliman’s actuarial models, not official IRS numbers, and can still change based on inflation data through September 2026. Confirm the final figures at irs.gov once announced.