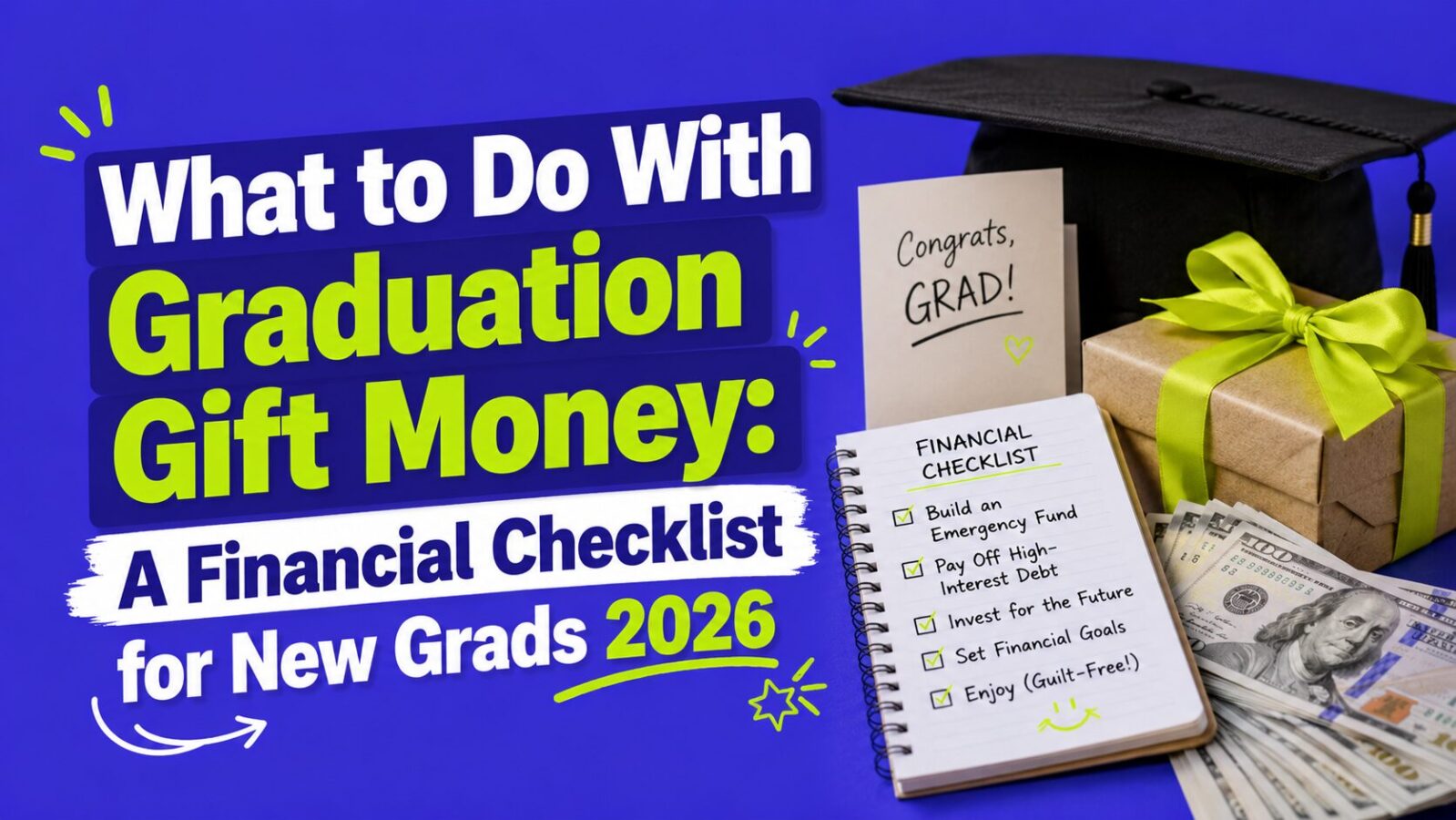

The smartest order for graduation gift money is simple: build a $1,000 starter emergency fund, pay off any high-interest debt, capture your first job’s 401(k) match, then put the rest in a Roth IRA or a named savings goal. Whether you got $500 or $3,000, what you do in the next 30 days sets the tone for decades, because the habits compound. Here is the honest order of operations, not what sounds inspiring, but what actually works.

Key Takeaways

- Know your number first, so the money does not vanish into daily spending.

- Emergency fund and high-interest debt come before investing.

- The 401(k) match is free money, the highest-return move of your first job.

- A Roth IRA in your low-tax 20s grows tax-free for decades.

First: Know Your Number

Add up all the gift money you received and write it down. This prevents the most common new-grad mistake: treating gift money as “extra” that slowly disappears into daily spending without a single deliberate decision. Once you have the number, allocate it in writing before spending any of it.

Build a Starter Emergency Fund ($1,000)

Before anything else, put $1,000 into a high-yield savings account you do not touch. At current top rates of 4.20% to 4.75% APY, that earns a bit of interest just sitting there, but the real point is that the first surprise expense, a car repair or a deposit, does not go on a credit card. If your gifts total under $1,000, put it all here first. See our guide on the best high-yield savings accounts.

Pay Off Any High-Interest Debt

If you carry credit card balances above about 15% APR, clear them before investing anything, since no investment reliably beats 20% a year and paying off a 21% balance is a guaranteed 21% return. Student loans are different: federal undergraduate loans run around 6.5% for 2026-27, so paying them down competes with investing but does not obviously win the way credit card payoff does. Knock out high-interest consumer debt first, then revisit student loans.

Get Your First Job’s 401(k) Match

This does not require your gift money directly, but it is the single most important action at your first job: contribute at least enough to your 401(k) to get the full employer match from your first eligible day. The match is free money, an instant 50% to 100% return that nothing else in finance beats. Do not wait to “feel settled,” enroll on day one. Having your emergency fund in place is what lets you direct paycheck contributions to the 401(k) without worry.

Open a Roth IRA and Invest the Rest

If you have gift money left, open a Roth IRA and invest it. The 2026 Roth limit is $7,000 (or your earned income for the year, whichever is lower). You need earned income to contribute (gift money itself does not count, but any job income does). Roth is usually right for new grads because you are likely in the lowest tax bracket of your career, so paying tax now and letting it grow completely tax-free wins. A $7,000 contribution at 22 growing at 7% can become well over $100,000 by 65, all tax-free. Open one at Fidelity, Vanguard, or Schwab and put it in a target-date or S&P 500 index fund. See our guide on Roth IRA vs 401(k).

Save Toward a Specific Goal

Any money left after the emergency fund and Roth IRA should have a named purpose, since generic “savings” rarely stays saved but specific goals do. Good targets include moving costs or a first apartment deposit, repairing a car before it becomes a crisis, building toward a full 3-to-6-month emergency fund, or a planned purchase like a laptop or certification exam. Keep it in a separate HYSA labeled with the goal.

What Mistakes Should New Grads Avoid?

- Upgrading your lifestyle immediately. Wait three months of full-salary living before any permanent upgrades.

- Delaying the 401(k). Every month you wait costs decades of compounding; enroll on day one.

- Carrying a credit card balance. You build credit by using the card and paying in full, not by carrying a balance.

- Ignoring the student loan grace period. Use the six months after graduation to pick the right repayment plan (RAP, standard, or IBR) before payments start.

- Treating the emergency fund as a vacation fund. Label it “emergency only” and mean it.

How Should You Allocate by Gift Total?

| Gift total | Recommended allocation |

|---|---|

| Under $500 | 100% to the emergency fund starter |

| $500 to $1,500 | $1,000 to emergency fund, rest to Roth IRA or a goal |

| $1,500 to $3,000 | $1,000 emergency fund, pay any credit card debt, rest to Roth IRA |

| Over $3,000 | $1,000 emergency fund, pay credit card debt, max the Roth IRA, rest to a goal |

See It Compound

Use this calculator to see how even a small starting amount grows over decades:

Compound Interest Calculator

FAQ

What should I do with graduation money?

In order: build a $1,000 emergency fund, pay off high-interest debt, capture your 401(k) match, then invest the rest in a Roth IRA or a named savings goal. Decide the allocation in writing before spending any of it.

Should a new grad open a Roth IRA?

Yes, if you have earned income. You are likely in your lowest tax bracket, so Roth’s tax-free growth is especially valuable, and you can contribute up to $7,000 for 2026 (or your earned income, if lower).

Pay off student loans or invest the gift money?

Clear high-interest credit card debt first, capture your 401(k) match, then weigh student loans (around 6.5%) against investing. At that rate it is closer, so the match and Roth usually come first.

How much of my gift money should I save?

Build the $1,000 buffer first, then invest or save the rest with a purpose. If your gift is under $1,000, put all of it toward the emergency fund.

Bottom Line

Graduation money is a rare head start, so use it deliberately: $1,000 emergency fund, kill high-interest debt, grab your 401(k) match, then a Roth IRA or a named goal. Avoid instant lifestyle creep and 401(k) delay, and the habits you set now compound for decades. To go deeper, see our guides on Roth IRA vs 401(k), the best high-yield savings accounts, and negotiating your first salary.

This article is for educational and informational purposes only and does not constitute financial advice. Contribution limits, rates, and tax rules are for 2026 and subject to change.