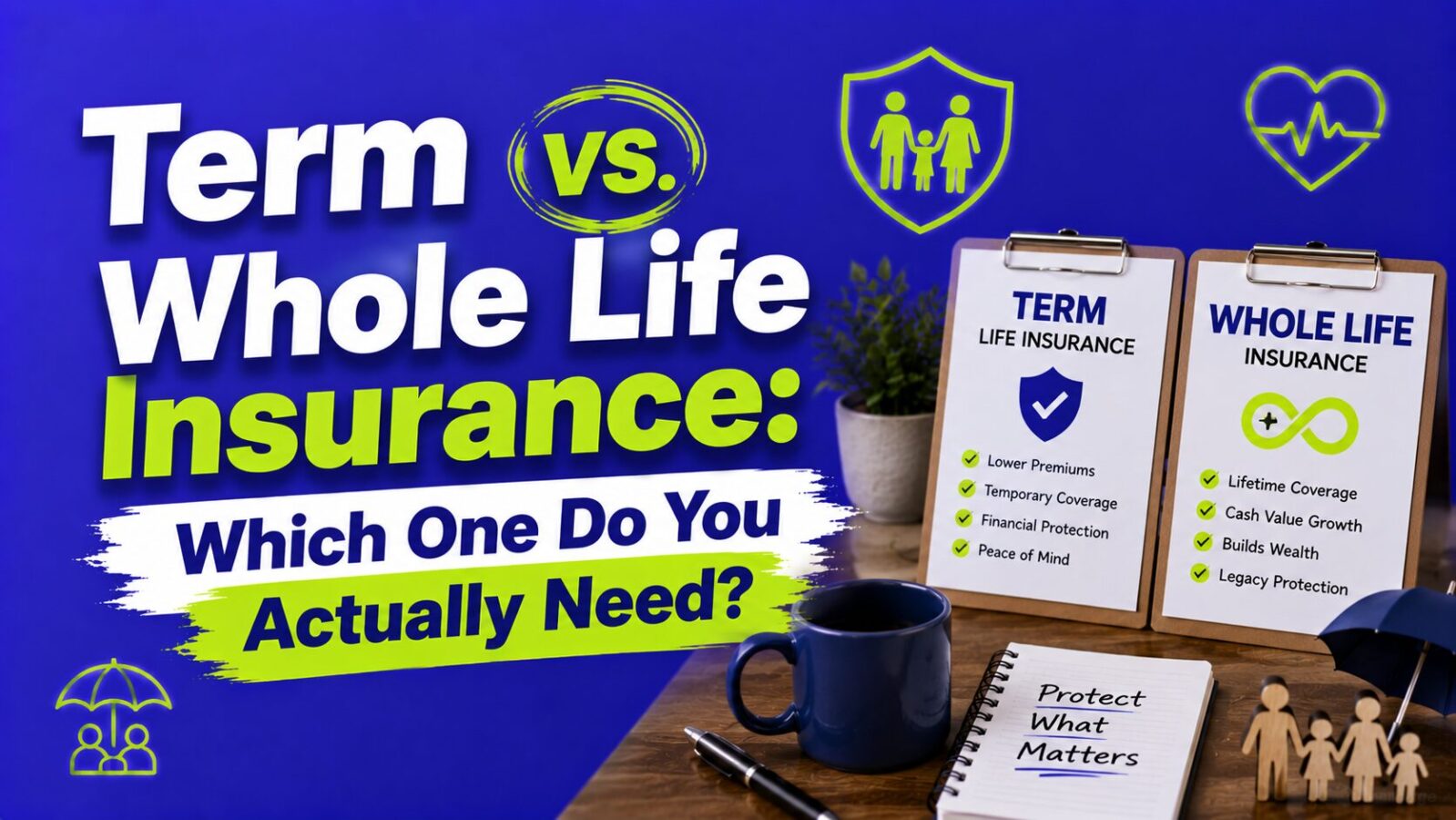

Life insurance is one of those financial products that most young adults know they should probably have but keep putting off because it feels complicated, morbid, or both. Here is the truth: it does not have to be complicated. The vast majority of people need a simple, affordable policy that protects their family if the worst happens. And the debate between term and whole life insurance has a clear winner for most situations.

- For almost everyone who needs life insurance, term life is the right choice: cheap, simple, and covering the years your family depends on your income.

- Whole life often costs around 10x more than term for the same death benefit, and its ‘investment’ component grows slowly.

- A healthy person in their 20s or 30s can often get a 20 to 30 year, $500,000 term policy for about $20 to $40 a month.

- ‘Buy term and invest the difference’ wins for most people; whole life mainly fits niche estate-planning needs.

This guide breaks down how each type works, what they cost, when each one makes sense, and how to figure out how much coverage you actually need. No sales pitch, no scare tactics, just the math.

Here is the comparison that ends most debates. A healthy 35-year-old can get a 20-year, $500,000 term policy for roughly $25 to $40 a month in 2026. A comparable whole life policy at the same coverage runs about $300 to $500 a month, often close to 10 times more. Over 30 years that gap adds up to well over $180,000 in extra premiums, before counting the slow-growing cash value the whole life policy builds. Invest that monthly difference in low-cost index funds instead and you almost always come out far ahead, which is the entire logic behind “buy term and invest the difference.”

What is life insurance and who needs it?

Life insurance is a contract: you pay premiums, and if you die during the coverage period, the insurance company pays a death benefit to your beneficiaries.

You need life insurance if anyone depends on your income:

- A spouse or partner who relies on your earnings to cover shared expenses

- Children who depend on you financially

- A co-signer on a mortgage, business loan, or other debt

- Aging parents you support financially

- A business partner who would need to buy out your share

If nobody depends on your income, you probably do not need life insurance yet. A single 25-year-old with no dependents and no co-signed debt can skip it for now and revisit later. But the moment someone depends on your paycheck to pay rent, cover childcare, or eat dinner, life insurance stops being optional.

How term life insurance works

Term life insurance is the simplest form. You pick a coverage amount and a term length, you pay a fixed premium, and if you die during that term, your beneficiaries receive the death benefit. If you outlive the term, the policy ends and nothing is paid out.

Key features:

- Term lengths: typically 10, 20, or 30 years

- Premiums: fixed for the entire term (a 20-year policy locks in the same monthly payment for all 20 years)

- Coverage amounts: usually $100,000 to $10,000,000+

- Cash value: none. Term life is pure protection.

- Renewability: most policies can be renewed after the term expires, but at higher premiums based on your age

- Convertibility: many term policies include an option to convert to a permanent policy without a new medical exam

Term life is cheap because it is straightforward. The insurance company is betting that you will not die during the term (statistically, they are almost always right), and you are paying for peace of mind in case they are wrong.

Best for: Young families who need $500K to $1M+ in coverage on a budget, anyone with a mortgage, primary breadwinners during their peak earning and child-raising years, and people who want to build wealth in their 20s and 30s by keeping insurance costs low and investing the savings.

How whole life insurance works

Whole life insurance lasts your entire life (as long as you pay the premiums). It combines a death benefit with a savings component called cash value that grows over time at a guaranteed rate.

Key features:

- Coverage period: your entire life (no expiration)

- Premiums: fixed, but significantly higher than term for the same coverage amount

- Cash value: a portion of each premium goes into a savings component that grows tax-deferred at a guaranteed rate (typically 2 to 4%)

- Loans: you can borrow against your cash value, though unpaid loans reduce the death benefit

- Guaranteed death benefit: as long as premiums are paid, your beneficiaries receive the death benefit no matter when you die

Whole life is significantly more expensive because the insurance company guarantees a payout. Since the policy never expires, they will eventually have to pay. They are also managing and guaranteeing returns on the cash value component.

Legitimate use cases: High-net-worth individuals using it as an estate planning tool, parents of children with special needs who will require lifelong financial support, and business owners funding buy-sell agreements.

The cost difference: real numbers

Here is what a $500,000 policy typically costs for a healthy 30-year-old non-smoker in 2026:

| Policy type | Monthly premium | Annual premium | Total cost over 30 years |

|---|---|---|---|

| 20-year term | $22 to $30 | $264 to $360 | $5,280 to $7,200 |

| 30-year term | $30 to $45 | $360 to $540 | $10,800 to $16,200 |

| Whole life | $350 to $500 | $4,200 to $6,000 | $126,000 to $180,000 |

A whole life policy costs roughly 10 to 15 times more than a comparable term policy. For $500,000 in coverage, you might pay $30/month for term or $400/month for whole life. That is a difference of $370/month or $4,440/year going toward a cash value component that typically earns less than a basic index fund.

Why most financial advisors recommend term

1. Insurance needs are temporary

Think about why you need life insurance: to replace your income while your kids are young, pay off the mortgage, or cover a spouse’s living expenses until they can adjust. These are time-bound needs. Your kids will grow up. The mortgage will be paid off. Your spouse will build their own financial security. A 20 or 30-year term policy covers the window when your death would cause the most financial damage. By the time the term expires, your savings and investments may mean you no longer need life insurance at all.

2. The cash value component is a poor investment

Whole life’s cash value typically grows at 2 to 4% per year. Compare that to investing the premium difference in a low-cost index fund.

Scenario: 30-year-old buys a 30-year term policy at $35/month instead of whole life at $400/month. They invest the $365 monthly difference in an S&P 500 index fund averaging 7% annual returns.

| After… | Cash value (whole life, ~3%) | Investment account (7%) |

|---|---|---|

| 10 years | ~$30,000 | ~$63,000 |

| 20 years | ~$75,000 | ~$190,000 |

| 30 years | ~$130,000 | ~$440,000 |

After 30 years, the “buy term and invest the difference” strategy produces roughly three times more wealth than whole life’s cash value — and that investment account is yours, with no insurance company in the middle.

3. Whole life’s tax advantages are overstated

Yes, whole life’s cash value grows tax-deferred. But so does your 401(k), IRA, HSA, and 529 plan. If you have not maxed out those accounts (and most young adults have not), the tax benefits of whole life insurance are redundant. Those other accounts also offer better returns, more investment flexibility, and in the case of Roth accounts, completely tax-free withdrawals.

4. Complexity benefits the seller, not the buyer

Whole life policies are complicated. The premium structure, cash value projections, dividend scales, surrender charges, and loan provisions create a product that most buyers do not fully understand. When someone earns 10 to 15 times more commission selling you whole life versus term, it is worth asking whether the recommendation is driven by your needs or their compensation.

How much coverage do you need?

The standard rule of thumb is 10 to 12 times your annual gross income. For a more precise number, use the DIME method:

- D: Debt — all debts your family would need to pay off (mortgage, car loans, student loans, credit card balances)

- I: Income — your annual income multiplied by the number of years your family would need support (typically 10 to 15 years)

- M: Mortgage — remaining mortgage balance (if not already in Debt)

- E: Education — estimated future education costs for your children

DIME Coverage Calculator

Enter your details to calculate how much life insurance coverage you actually need.

Then verify your exact premium with the life insurance calculator:

Life Insurance Needs Calculator

How to buy life insurance

Step 1: Determine your coverage amount using the DIME calculator above.

Step 2: Choose your term length. If you are 30 with young kids, a 20 or 30-year term covers you until they are financially independent.

Step 3: Get quotes from multiple providers. Online brokers like Policygenius, Ladder, and Haven Life let you compare rates in minutes.

Step 4: Complete the application. Most term policies require a health questionnaire. Some require a medical exam. "No-exam" policies exist but typically cost more.

Step 5: Name your beneficiaries. Be specific. Use names, not just "my spouse" or "my kids." Update beneficiaries after major life events (marriage, divorce, birth of a child).

Step 6: Set up automatic payments so your policy never lapses due to a missed premium.

Common mistakes to avoid

Buying too little coverage. A $100,000 policy sounds like a lot, but it covers barely one year of household expenses for many families. Use the DIME method to find your actual number.

Buying whole life when you cannot afford enough term. A $100,000 whole life policy costs more than a $1,000,000 term policy. Coverage amount matters more than policy type.

Waiting too long. Life insurance premiums are based primarily on your age and health. A 30-year-old pays roughly half what a 40-year-old pays for identical coverage. Lock in rates while you are young and healthy.

Relying solely on employer coverage. Most employer policies offer 1x to 2x your annual salary. That is far less than your family needs, and you lose it when you leave the job. Think of employer coverage as a supplement, not your primary policy.

Letting an agent upsell you. If an insurance agent is pushing hard for whole life when your situation clearly calls for term, ask yourself who benefits more from that recommendation. Get a second opinion from a fee-only financial advisor who does not earn commissions on insurance sales.

Frequently Asked Questions

The moment someone depends on your income. If you are getting married, having a child, or buying a home with a partner, get coverage before the event, not after.

The policy expires. You can renew (at higher premiums based on your current age) or purchase a new policy. If your net worth has grown enough that your family is financially secure without your income, you may not need to renew at all. This is the ideal outcome.

Yes. Many people have a base policy plus a smaller supplemental policy or employer coverage. Insurers will evaluate your total coverage relative to your income to determine how much they will issue.

Generally no, not yet. If nobody depends on your income, there is no financial risk to insure against. Save that premium money and invest it instead. Revisit when your situation changes.

The bottom line

For the vast majority of people, the answer is term life insurance. It is cheaper, simpler, and when combined with a disciplined investment strategy, produces better long-term financial outcomes than whole life.

Buy a 20 or 30-year term policy with enough coverage to replace your income and pay off your debts. Take the hundreds of dollars per month you are saving compared to whole life and put that money into index funds, your 401(k), or your wealth-building strategy. By the time your term expires, you will have built enough wealth that you no longer need life insurance at all.

That is the goal: not to need life insurance forever, but to protect your family during the years when they need it most while building the financial independence that makes insurance unnecessary.

Ready to get covered?

- Fastest quotes (under 5 minutes): Policygenius compares rates from multiple insurers without you filling out the same form repeatedly.

- No-exam term policies: Haven Life and Ladder offer instant-approval term policies entirely online, often without a medical exam for healthy applicants under 45.

- Not sure how much you need? Use the DIME calculator above or check our financial goals by age guide to see how life insurance fits into your overall financial plan.