Retiring before 59.5? The Roth conversion ladder lets you access your 401(k) money penalty-free. It is the key strategy for FIRE practitioners. Here is exactly how to build one, year by year.

The biggest objection to early retirement is this: “My money is locked in my 401(k) until 59.5. I cannot touch it without a 10% penalty.” That objection is wrong. The Roth conversion ladder is a completely legal strategy that lets you access Traditional 401(k) and IRA money before age 59.5, penalty-free. It has been used for decades and is based on standard IRS rules described in Publication 590-B. It is the early retiree’s bridge on the retirement account roadmap.

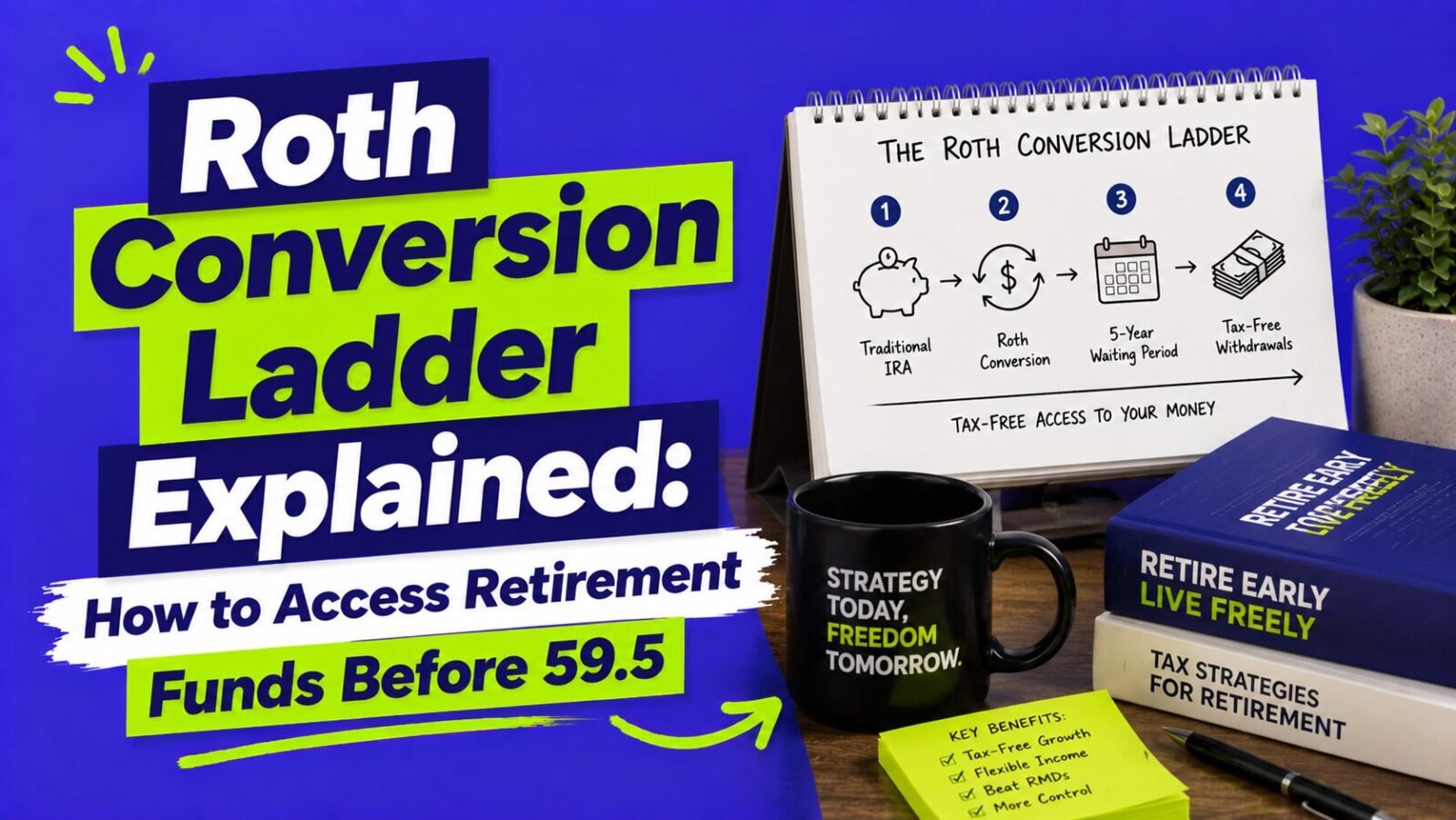

- Each Roth conversion has its own 5-year clock that starts January 1 of the year you convert. Convert $40,000 in any month of 2027 and that $40,000 is available for penalty-free withdrawal starting January 1, 2032, regardless of your age. That 5-year wait is what creates the “ladder” and requires advance planning.

- The first 5 years of early retirement must be funded by a bridge: Roth IRA contributions (withdrawable anytime, tax and penalty-free), a taxable brokerage account, or cash savings. FIRE practitioners build the bridge during working years by maxing Roth contributions and accumulating taxable investments.

- Early retirees often pay far lower taxes on conversions than workers do. With no job income, a $40,000 conversion minus the 2026 standard deduction ($16,100) leaves about $23,900 taxable, for roughly $2,620 in federal tax, an effective rate near 6.6%. This tax arbitrage is a major driver of the ladder’s power.

- ACA health insurance subsidies are sensitive to conversion income. If you buy Marketplace coverage in early retirement, converting too much in one year can reduce or eliminate your premium tax credit, so size conversions to stay within the subsidy range.

- Do not confuse the 5-year rule for conversions with the 5-year rule for Roth earnings. They are separate clocks. Regular Roth contributions (not conversions) can be withdrawn anytime, which is why your Roth contribution history is the most important bridge asset.

Build your ladder: see the year-by-year timeline

Roth Conversion Ladder Planner

Enter your details to see your ladder timeline with available withdrawals by year. Estimates only.

The problem: early withdrawal penalties

When you contribute to a Traditional 401(k) or Traditional IRA, the money is tax-deferred: you get a deduction now and pay income tax when you withdraw in retirement. Withdraw before age 59.5 and you also pay a 10% early withdrawal penalty on top of income tax.

On a $40,000 withdrawal at a 22% tax rate, the penalty adds $4,000: about $8,800 in income tax plus $4,000 penalty, roughly $12,800 total. The Roth conversion ladder eliminates the 10% penalty entirely.

How does the ladder work? Four steps

Step 1: Roll your 401(k) to a Traditional IRA

When you leave your job, roll your 401(k) into a Traditional IRA at Fidelity, Schwab, or Vanguard via a direct rollover. This gives you control over the funds and access to low-cost investments, and it sets up the source for your annual conversions.

Step 2: Convert one year of expenses per year to Roth

Each year, convert enough from your Traditional IRA to your Roth IRA to cover one year of living expenses. On $50,000/year spending, convert $50,000. You pay ordinary income tax on the converted amount that year, but in early retirement with no other income, this often falls in the 10 to 12% bracket, the lowest federal rates available. See our Roth conversion guide for the bracket-filling mechanics.

Step 3: Wait 5 years

Each conversion has its own 5-year clock that starts January 1 of the conversion year. Convert in any month of 2027 and the withdrawal window opens January 1, 2032. This is the core timing constraint, and why the strategy needs a 5-year bridge to fund early retirement before rungs become available.

Step 4: Withdraw penalty-free after 5 years

After the 5-year period, withdraw the converted amount from your Roth IRA with no penalty and no additional tax (tax was paid at conversion). Each subsequent year, a new rung opens as the previous year's conversion ages past 5 years. The ladder runs continuously until you reach 59.5, after which Traditional IRA withdrawals become penalty-free and the ladder is no longer necessary.

The 5-year bridge: funding years 1 through 5

The 5-year wait creates an immediate challenge: you need income before any conversions are available. The main bridge options:

Roth IRA contributions (often the cleanest): regular Roth contributions, not conversions, can be withdrawn anytime, at any age, with no tax or penalty. Contribute $7,500/year to a Roth IRA for 10 years and you have about $75,000 in contributions available immediately. Build this during working years by maxing Roth contributions consistently.

Taxable brokerage account: sell index fund investments to fund bridge years. Long-term capital gains are taxed at 0% if your taxable income is under roughly $49,450 single / $98,900 married filing jointly (2026). Many early retirees with low conversion income pay zero tax on gains during bridge years.

Cash savings: five years of expenses in a high-yield savings account or CDs. At $50,000/year, that is $250,000, which is significant but provides certainty. Often combined with Roth contributions for a smaller cash buffer.

HSA reimbursements: if you paid medical expenses out of pocket and saved the receipts while working, you can reimburse yourself from your HSA anytime, tax-free, with no expiration on the receipt date. Years of accumulated receipts can provide meaningful bridge funding.

Rule of 55: if you leave your employer in the calendar year you turn 55 or later, you can withdraw from that employer's 401(k) without the 10% penalty. It does not apply to IRAs or previous employers' plans, but it is useful for those retiring at 55 rather than earlier.

72(t) / SEPP distributions: Rule 72(t) allows penalty-free IRA withdrawals at any age if you take Substantially Equal Periodic Payments for at least 5 years or until 59.5, whichever is longer. It provides access but locks you into fixed payments, so the conversion ladder is usually preferred for flexibility.

Why do early retirees pay less tax?

One of the most counter-intuitive advantages of early retirement is that your tax rate often drops sharply.

| Scenario | Income | Approx. effective federal rate |

|---|---|---|

| Working at $120,000 salary | $120,000 | ~16% effective |

| Early retired, $50,000 Roth conversion | $50,000 minus $16,100 deduction = $33,900 taxable | ~7.6% effective |

| 0% capital gains threshold (single) | Under ~$49,450 taxable income | 0% on long-term gains |

You can go from about a 16% effective rate as a worker to under 8% in early retirement by converting in low-income years rather than withdrawing in traditional retirement (when Social Security and other income push you into higher brackets). This tax arbitrage is a major reason the conversion ladder is so powerful.

The ACA subsidy warning

If you buy health insurance through the ACA Marketplace before Medicare eligibility at 65, your conversion income directly affects your premium tax credit. Converting too much in a single year can raise your Modified Adjusted Gross Income above subsidy thresholds, costing thousands in annual subsidies.

For a couple in early retirement, staying within ACA subsidy eligibility (generally 100 to 400% of the federal poverty level, though rules shift over time) can be worth thousands per year in premium help. Plan your annual conversion amount to balance tax-free growth against subsidy preservation; sometimes converting slightly less is worth more than the extra Roth space. Verify current ACA rules each year, since they change.

Common mistakes

Not planning the 5-year bridge before retiring. The ladder only works if you have another funding source for years 1 through 5. Retiring without a bridge means withdrawing from the Traditional IRA with the 10% penalty, which defeats the purpose. Build your bridge (Roth contributions plus a taxable account) during working years.

Converting too much in one year. A $200,000 single-year conversion can push you into the 32% bracket or higher, erasing the tax advantage. Spread conversions across years to stay in the 10 to 12% brackets. The annual amount should roughly match your spending needs, not exceed them.

Forgetting state income taxes. Some states tax Roth conversions. The nine states with no broad income tax (Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, Wyoming) are often FIRE-friendly for this reason. If you plan to relocate in early retirement, doing so before starting the ladder can avoid state tax on conversion years.

Not tracking each conversion's date. Each conversion has its own 5-year clock. Keep records of every conversion year and amount. Your brokerage tracks this, but maintain your own records on IRS Form 8606 too.

Strategy comparison: early access options

| Strategy | Penalty-free | Flexibility | Best for |

|---|---|---|---|

| Roth conversion ladder | Yes (after 5 years) | High (annual control) | FIRE retirees 40+ |

| Roth contributions withdrawal | Yes (anytime) | Very high | Bridge years 1 to 5 |

| Taxable brokerage | Yes | Very high | Bridge + supplemental |

| 72(t) / SEPP | Yes (with restrictions) | Low (locked payments) | Those without a Roth bridge |

| Rule of 55 | Yes (last employer 401k only) | Moderate | Retiring at 55+ |

| HSA reimbursements | Yes (medical expenses) | High | Supplemental bridge |

Frequently Asked Questions

Yes. It uses standard IRS rules for conversions and the 5-year withdrawal rule, both described in Publication 590-B. The key is following them exactly: convert from a Traditional IRA to a Roth IRA, wait the full 5 calendar years from the conversion year, and file Form 8606 each year to document the conversion amounts.

They are two separate rules. The contribution 5-year rule determines when Roth earnings can be withdrawn tax-free (the account must be 5 years old); it does not affect withdrawing your contributions, which come out anytime tax and penalty-free. The conversion 5-year rule is what the ladder uses: each conversion must wait 5 years before its principal can be withdrawn without the 10% penalty (if you are under 59.5).

You need another bridge source: a taxable brokerage account (potentially 0% long-term capital gains if income is low), five years of cash savings, 72(t) SEPP distributions, or Rule of 55 if you leave a job in the year you turn 55. If you still have working years ahead, prioritize building Roth contribution history and a taxable account alongside your 401(k).

The pro-rata rule applies: if your Traditional IRA mixes deductible and non-deductible money, each conversion is a proportional blend of both. For most FIRE practitioners rolling over a 401(k), the whole balance is pre-tax, so the full conversion is taxable and pro-rata is not a complication. Track any non-deductible basis on Form 8606.

Yes, and a larger rung opens 5 years later. But converting much more than you need pushes you into higher brackets and reduces efficiency. The optimal amount usually covers a future year's spending, stays within a target bracket (often 12%), and protects ACA subsidy eligibility. A market downturn can be a good time to convert more, since the same shares cost less in taxable dollars.

Laws can change, but retroactive changes to existing Roth balances are historically rare. Money already converted is generally grandfathered under the rules at conversion. A 2021 proposal targeted the backdoor and mega backdoor mechanisms but did not propose taxing existing Roth balances. Starting sooner moves money into the protected Roth structure under current rules.

If there is any chance you retire before 59.5, even at 55, understanding the ladder gives you options. More practically, building Roth contribution history now creates a future bridge fund at no extra cost. The Roth balance grows tax-free regardless, and maxing the Roth during working years is almost always a good move, especially if early retirement enters the picture.

No. They go in the same Roth IRA, and your brokerage tracks them separately for tax purposes. IRS ordering rules pull contributions first (anytime, no tax or penalty), then conversions in chronological order (penalty-free 5 years after each), then earnings last. That ordering works in the ladder user's favor: contributions cover bridge years while conversions open in sequence.

The bottom line

The Roth conversion ladder removes the biggest barrier to early retirement: accessing tax-advantaged savings before 59.5. By converting Traditional IRA money to Roth in low-income early-retirement years, you pay minimal tax and gain penalty-free access after 5 years.

The requirements: a 5-year bridge fund (Roth contributions, a taxable account, or cash), disciplined annual conversions sized to stay in low brackets, and patience during the ramp-up. Use the planner above to see your year-by-year timeline.

- New to retirement accounts? Start with our hub, Retirement Accounts Explained.

- Building a FIRE plan? Read our FIRE movement guide for the FIRE number, the 4% rule, and the full framework.

- Want the conversion mechanics? Read our backdoor Roth IRA guide for the pro-rata rule and step-by-step process.

- Self-employed? Read our SEP IRA guide for building the Traditional IRA balance that fuels your ladder.

A quick note: this article is for educational purposes only and is not financial or tax advice. Tax figures come from the IRS and apply to tax year 2026; verify current numbers at IRS.gov. The conversion ladder, the pro-rata rule, and ACA interactions can get complex, so it is worth working with a CPA or fee-only financial planner on your specific plan.