Index funds and ETFs both let you own hundreds of stocks in a single purchase. The differences are small but real. Here is what actually matters for your money and which one to pick.

In our beginner investing guide, we recommended buying index ETFs like VTI and VXUS. But you have probably also heard the term “index fund” used interchangeably with “ETF.” Are they the same thing? Not exactly. Are the differences big enough to matter? For most beginners, barely. But understanding what you are buying makes you a better investor.

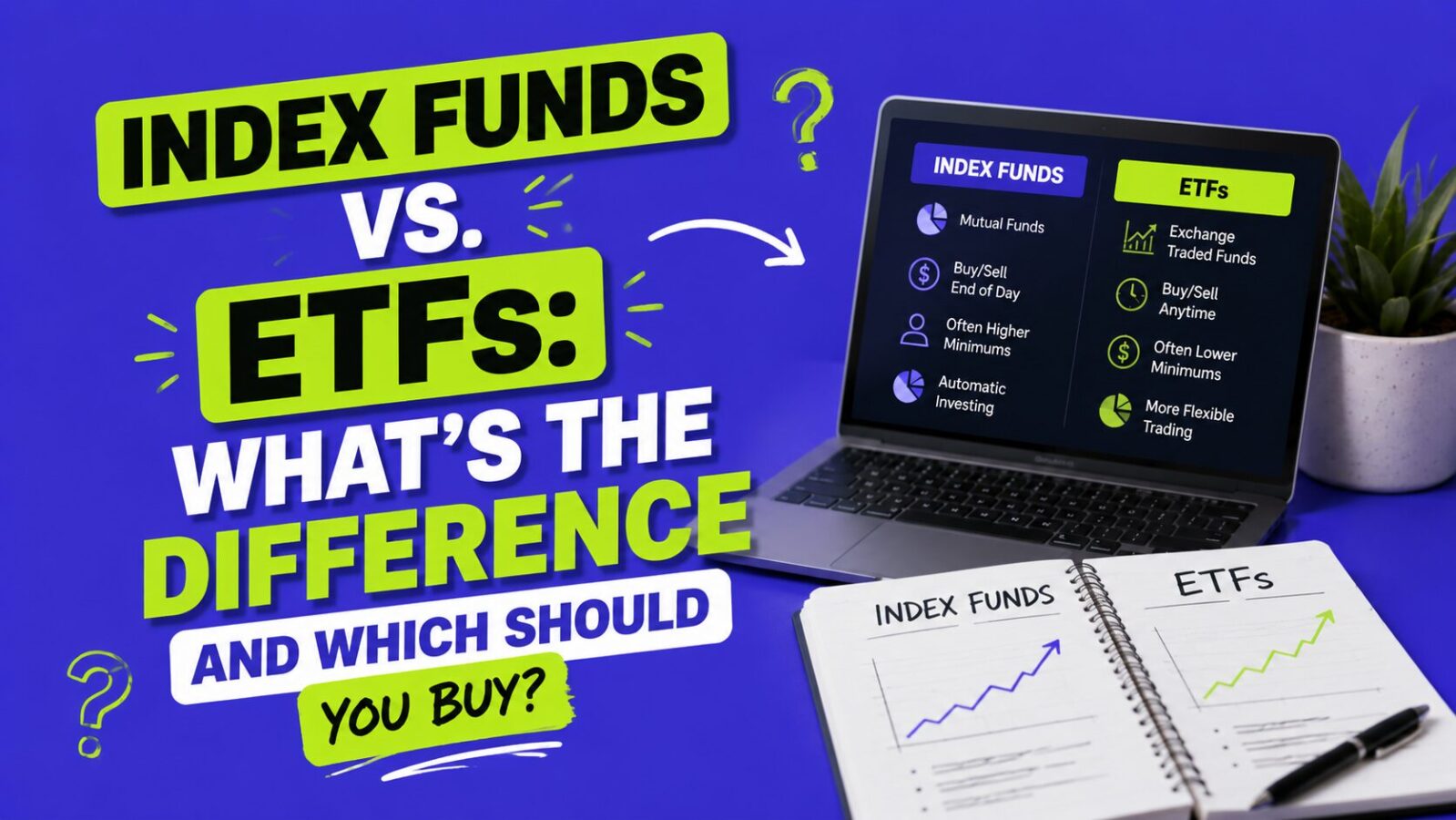

The short answer: an index fund is a strategy (track an index instead of picking stocks). An ETF is a structure (a fund that trades on the stock exchange like a stock). Many ETFs are index funds. Many index funds are not ETFs. The overlap is where the confusion starts.

What is an index?

An index is simply a list of stocks (or bonds) that follows a set of rules. The S&P 500 is an index of the 500 largest US companies by market cap. The Total US Stock Market index includes roughly 4,000 US companies of all sizes. The MSCI ACWI ex-USA index covers thousands of companies outside the US.

Nobody created these lists to sell you anything. They exist as benchmarks to measure how “the market” is performing. When the news says “the market was up 1% today,” they usually mean the S&P 500 went up 1%.

An index fund is any fund that tries to match the performance of one of these indexes by buying all (or most) of the stocks in it, in the same proportions. Instead of a team of analysts picking stocks they think will beat the market, the fund copies the list. This approach is called passive investing.

What is a mutual fund?

A mutual fund is a pool of money from many investors, managed by a fund company (like Vanguard, Fidelity, or Schwab). When you buy shares of a mutual fund, your money joins the pool.

Key characteristics of mutual funds:

Priced once per day. You place an order during the day, but it executes at the end-of-day price (called the NAV, or Net Asset Value).

Bought in dollar amounts. You can invest $100, $500, or any dollar amount. The fund gives you fractional shares automatically.

May have minimums. Some require $1,000 to $3,000 to open. Fidelity’s index funds have $0 minimums. Vanguard’s Admiral shares require $3,000.

Traded directly with the fund company, not on the stock exchange.

An index mutual fund is a mutual fund that follows a passive index strategy. Vanguard’s VFIAX (S&P 500 index) and VTSAX (Total Stock Market index) are the most famous examples.

What is an ETF?

An ETF (Exchange-Traded Fund) is also a pool of investor money, but it is packaged and traded like a stock on the stock exchange.

Key characteristics of ETFs:

Priced throughout the day. The price changes every second while the market is open. You can buy at 10:03 AM and sell at 2:47 PM.

Bought in shares (or fractional shares). You buy 1 share of VTI at $280, or 0.5 shares at $140 if your broker supports fractional shares. Most major brokers now do.

No minimums. The minimum investment is the price of one share (or a fraction). VTI costs about $280/share, but you can buy $10 worth at most brokers.

Traded on the stock exchange, just like buying Apple or Tesla stock.

An index ETF is an ETF that follows a passive index strategy. VTI (Vanguard Total Stock Market ETF) and VOO (Vanguard S&P 500 ETF) are the most popular.

The actual differences that matter

Trading flexibility

ETFs trade throughout the day at real-time prices. Mutual funds trade once at end-of-day NAV.

Does this matter for you? Almost certainly not. You are a long-term investor buying and holding for decades. Whether you buy at $280.15 at 10 AM or $280.42 at market close makes zero difference over 30 years. This feature matters for active traders, not for beginners building wealth.

Minimum investment

Index mutual funds may require $1,000 to $3,000 to open. Index ETFs require only the price of one share, and with fractional shares at most brokers, you can start with as little as $1.

Does this matter for you? Yes, if you have less than $3,000 to invest. ETFs are more accessible for small starting amounts. This is one reason the beginner investing guide recommends ETFs.

Expense ratios

The expense ratio is the annual fee the fund charges, expressed as a percentage. Lower is better.

For the same index, the ETF and mutual fund versions have nearly identical expense ratios:

- Vanguard Total Stock Market ETF (VTI): 0.03%

- Vanguard Total Stock Market Index Fund Admiral (VTSAX): 0.04%

- Fidelity Total Market Index Fund (FSKAX): 0.015%

- Schwab Total Stock Market Index Fund (SWTSX): 0.03%

The difference between 0.03% and 0.04% on a $10,000 portfolio is $1/year. Irrelevant. At $100,000 it is $10/year. Still irrelevant.

Does this matter for you? No. Any expense ratio under 0.10% is excellent. Do not choose between funds based on a 0.01% difference.

Tax efficiency

This is the one area where ETFs have a genuine structural advantage. Due to how ETFs are created and redeemed (a mechanism called “in-kind creation”), they generate fewer taxable capital gains distributions than mutual funds.

In plain English: mutual funds sometimes pay out taxable gains at year-end even if you did not sell anything. ETFs rarely do this.

Does this matter for you? Only in a taxable brokerage account. Inside a Roth IRA, Traditional IRA, or 401(k), you do not pay taxes on capital gains distributions anyway. Since most beginners should be investing in a Roth IRA first, this advantage is irrelevant for your first several years of investing.

Automatic investing

Most brokerages let you set up automatic recurring purchases of mutual funds (buy $500 of VTSAX on the 1st of every month). Automatic investing in ETFs is less universally supported, though SoFi, Fidelity, Schwab, and M1 Finance now offer auto-invest for ETFs.

Does this matter for you? It used to matter a lot. Today, most beginner-friendly brokers support auto-invest for ETFs. Check that your broker offers this before choosing. Automation is critical for long-term wealth building.

Dividend reinvestment

Both mutual funds and ETFs can automatically reinvest dividends (DRIP). With mutual funds, reinvestment is seamless because you can buy fractional shares by dollar amount. With ETFs, reinvestment requires fractional share support at your broker. Most major brokers now support this, but verify with yours.

Side-by-side comparison

| Feature | Index Mutual Fund | Index ETF |

|---|---|---|

| Tracks an index | Yes | Yes |

| Expense ratio | 0.015% to 0.04% | 0.03% to 0.04% |

| Minimum investment | $0 to $3,000 | Price of 1 share (or $1 fractional) |

| Trading | End of day only | Anytime during market hours |

| Tax efficiency | Good | Better (in taxable accounts) |

| Auto-invest | Widely supported | Supported at most major brokers |

| Fractional shares | Built in | Broker-dependent (most support it) |

| Best for | 401(k) plans, large lump sums | Roth IRA, taxable accounts, small amounts |

See how index ETF returns compound over time:

Compound Interest Calculator

Use 7% as the annual return (long-term S&P 500 average after inflation). Change the monthly contribution to see how dollar-cost averaging accelerates growth.

So which should you buy?

For most beginners, the answer is index ETFs:

- No minimums. You can start with $10. Vanguard’s best mutual fund shares require $3,000.

- Tax efficiency. Better for taxable accounts, equal for retirement accounts.

- Universally available. You can buy VTI at any brokerage. Some mutual funds are only available at their own company.

- Simplicity. One ticker symbol (VTI), one purchase, done.

The exception: if your 401(k) only offers mutual funds (most do), buy the cheapest index mutual fund available in your plan. You do not get to choose ETFs inside most 401(k) plans, and the mutual fund version is essentially identical in a tax-advantaged account.

Recommended beginner ETF portfolio (the 3-fund portfolio):

- 60% VTI (Vanguard Total US Stock Market ETF, 0.03% expense ratio)

- 30% VXUS (Vanguard Total International Stock ETF, 0.07% expense ratio)

- 10% BND (Vanguard Total Bond Market ETF, 0.03% expense ratio)

Total cost: about $0.40/year on a $1,000 portfolio. Covers virtually every publicly traded stock and bond in the world.

Where to buy these ETFs:

| Broker | ETF auto-invest | Fractional shares | Best for |

|---|---|---|---|

| Fidelity | Yes | Yes | Best overall for beginners |

| Schwab | Yes | Yes | Strong research + no fees |

| SoFi Invest | Yes | Yes | Simplest mobile onboarding |

| Vanguard | Limited | ETFs only | Buy-and-hold purists |

Disclosure: Finance Pulse has an affiliate relationship with SoFi Invest. Fidelity and Schwab are included regardless of affiliate status.

Popular index ETFs and what they track

US Total Market: VTI (Vanguard) and ITOT (iShares). Roughly 4,000 US stocks of all sizes. The broadest US diversification in a single fund.

S&P 500: VOO (Vanguard), SPY (SPDR), and IVV (iShares). The 500 largest US companies. About 80% overlap with VTI since large caps dominate the total market anyway.

International (Developed + Emerging): VXUS (Vanguard) and IXUS (iShares). Thousands of companies in Europe, Asia, Latin America, and emerging markets. Essential for diversification beyond the US.

US Bonds: BND (Vanguard) and AGG (iShares). Thousands of US government and corporate bonds. Reduces portfolio volatility.

Growth-Tilted: VUG (Vanguard Growth ETF). Heavier on tech and high-growth companies. Higher potential return, higher volatility.

Dividend-Focused: VYM (Vanguard High Dividend Yield) and SCHD (Schwab US Dividend Equity). Companies that pay above-average dividends. Popular for income-oriented investors.

For beginners: stick with VTI + VXUS + BND. Add specialty ETFs later when you understand why you want them, not because they sound interesting.

Frequently asked questions

Can I own both index mutual funds and ETFs?

Yes. Many people use index mutual funds in their 401(k) and index ETFs in their Roth IRA or taxable account. They can hold the same underlying stocks and work together in your portfolio.

Is VOO better than VTI?

VOO tracks the S&P 500 (500 large US companies). VTI tracks the total US market (about 4,000 companies including mid-cap and small-cap). Historically, their returns are nearly identical because large-cap stocks dominate both. VTI gives slightly more diversification. Either is a great choice.

What about actively managed funds?

Over 10+ year periods, 80 to 90% of actively managed funds underperform their index benchmark after fees. The fund manager charges you more (typically 0.50 to 1.00% annually) and still loses to the index. This is not opinion. It is decades of data from S&P’s SPIVA Scorecard, which tracks actively managed fund performance against benchmarks every year. Index investing wins for the vast majority of people.

Are index ETFs safe?

No investment is “safe” in the sense of guaranteed returns. Stock index ETFs can lose 30% or more in a crash. But over any 20-year period in US stock market history, a diversified stock portfolio has always produced positive returns. The risk is short-term volatility, not long-term loss.

How often should I buy?

Monthly, on payday, automatically. Do not try to time the market. Do not wait for a “dip.” Research consistently shows that time in the market beats timing the market. Set up auto-invest, buy the same ETFs every month, and check your portfolio once per quarter at most.

Should I pick Vanguard, Fidelity, or Schwab ETFs?

For index ETFs tracking the same benchmark, the differences are negligible. VTI (Vanguard), ITOT (iShares/Fidelity), and SCHB (Schwab) all track the total US market with expense ratios between 0.03% and 0.04%. Pick whichever is available at your brokerage.

The bottom line

Index funds and ETFs are two vehicles for the same strategy: own the entire market at rock-bottom cost and let time do the work. For beginners, index ETFs are the slightly better choice because of lower minimums, better tax efficiency, and universal availability. But if your 401(k) offers a low-cost index mutual fund, use it. The difference between the two is far less important than the difference between investing and not investing.

Pick VTI, VXUS, and BND (or their equivalents at your broker). Set up auto-invest. Stop comparing funds. Start growing wealth.

Ready to start?

- Open an account today:

- New to investing entirely? Read the investing with $1,000 guide for the full step-by-step account setup sequence.

- Want the full portfolio strategy? Read our 3-fund portfolio guide for exactly how to allocate across VTI, VXUS, and BND.