If you are staring at multiple debts and wondering where to start, you are not alone. The average American household carries over $100,000 in total debt when you add up mortgages, car loans, student loans, and credit cards. The good news is that two proven strategies — the debt snowball and the debt avalanche — can help you crush that debt systematically. The question is: which one is right for you?

That is exactly what this guide will help you figure out. We will break down both methods, explain the math behind each one, and give you a hands-on calculator so you can plug in your own numbers and see real results.

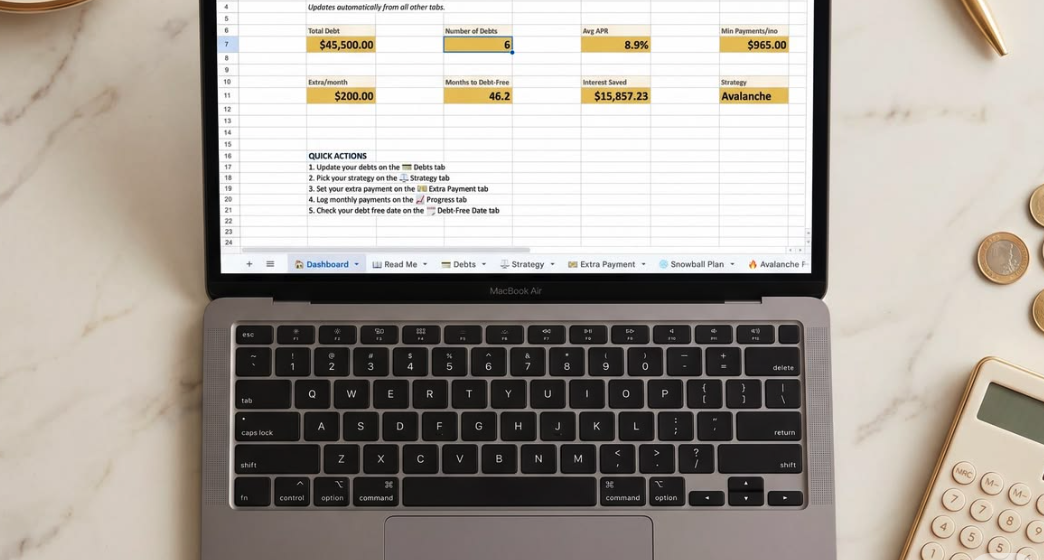

Use our free calculator below to see your personalized debt payoff plan, including total interest paid and your exact debt-free date.

Debt Snowball vs Avalanche Calculator

What Is the Debt Snowball Method?

The debt snowball method, popularized by personal finance expert Dave Ramsey, takes a psychology-first approach to paying off debt. Here is how it works:

- List all your debts from smallest balance to largest balance. Ignore interest rates for now.

- Make minimum payments on every debt except the smallest one.

- Throw every extra dollar at the smallest debt until it is completely paid off.

- Roll that payment into the next smallest debt. Your payment “snowballs” as each debt disappears.

- Repeat until every debt is gone.

Why the Snowball Works

The snowball method is built on behavioral science, not pure math. When you knock out that first small debt in a few weeks or months, your brain gets a hit of dopamine. You feel progress. You feel momentum. That emotional win keeps you motivated to tackle the next debt, and the next one after that.

Research from the Harvard Business Review found that people who focused on paying off small balances first were more likely to eliminate their overall debt than those who tried to optimize for interest rates. The reason is simple: motivation matters more than math if the math causes you to quit.

When to Choose the Snowball

The debt snowball is your best bet if:

- You have several small debts that you can knock out quickly

- You tend to lose motivation on long-term financial goals

- The interest rate differences between your debts are relatively small

- You need quick wins to build confidence

- You have tried other approaches and given up

What Is the Debt Avalanche Method?

The debt avalanche method is the mathematician’s approach. Instead of ordering debts by balance, you order them by interest rate. Here is the process:

- List all your debts from highest interest rate to lowest. Balance does not matter here.

- Make minimum payments on every debt except the one with the highest rate.

- Put all extra money toward the highest-interest debt until it is gone.

- Move to the next highest interest rate. Keep rolling payments forward.

- Continue until you are debt-free.

Why the Avalanche Works

The avalanche method minimizes the total interest you pay over the life of your debt. By attacking the highest-rate debt first, you stop the most expensive debt from compounding against you. Over time, this saves you real money — sometimes hundreds or even thousands of dollars compared to the snowball approach.

When to Choose the Avalanche

The debt avalanche makes the most sense if:

- You have a high-interest credit card or payday loan that is eating you alive

- You are disciplined and do not need quick wins to stay motivated

- The interest rate spread between your debts is large (for example, a 24% credit card vs. a 4% car loan)

- You want to pay the absolute least amount of interest possible

- You are already committed to the payoff journey and just want the optimal path

Snowball vs. Avalanche: A Head-to-Head Comparison

Let us look at how these two strategies stack up across the factors that matter most.

Total Interest Paid

Winner: Avalanche. By targeting high-interest debt first, you reduce the total cost of borrowing. In some scenarios, the savings can be significant. For example, if you have a $15,000 credit card at 22% APR and a $5,000 personal loan at 8%, the avalanche method could save you over $2,000 in interest compared to the snowball.

Time to First Payoff

Winner: Snowball. Because you start with the smallest balance, you will likely eliminate your first debt faster. That first “win” might come in just a few months, whereas the avalanche method might have you grinding away at a large, high-interest balance for a year or more before you see a debt disappear.

Psychological Motivation

Winner: Snowball. The quick wins and visible progress of the snowball method are powerful motivators. If you are the kind of person who needs to see the finish line to keep running, the snowball is built for you.

Total Time to Debt Freedom

This depends on your specific situation. In many cases, the avalanche gets you debt-free a few months sooner. But the difference is often smaller than people expect, especially if your debts have similar interest rates.

Simplicity

Tie. Both methods are straightforward. The snowball requires you to sort by balance, and the avalanche requires you to sort by interest rate. Either way, the process is the same: focus your extra payments on one debt at a time.

Example Scenario: Putting Both Methods to the Test

Let us walk through a realistic example so you can see the difference in action.

The Setup

Imagine you have the following debts and can put an extra $500 per month toward debt payoff beyond your minimum payments:

| Debt | Balance | Interest Rate | Minimum Payment |

|---|---|---|---|

| Store credit card | $2,500 | 26.99% | $75 |

| Visa credit card | $8,000 | 19.99% | $200 |

| Car loan | $12,000 | 5.49% | $350 |

| Student loan | $18,000 | 6.80% | $220 |

Total debt: $40,500

Total minimum payments: $845/month

Extra monthly payment: $500

Snowball Order (Smallest Balance First)

- Store credit card ($2,500)

- Visa credit card ($8,000)

- Car loan ($12,000)

- Student loan ($18,000)

With the snowball method, you would pay off the store credit card in about 4 months. That $575 payment ($75 minimum + $500 extra) then rolls into the Visa, giving you $775/month toward that balance. You would be completely debt-free in approximately 34 months, paying roughly $7,200 in total interest.

Avalanche Order (Highest Rate First)

- Store credit card (26.99%)

- Visa credit card (19.99%)

- Student loan (6.80%)

- Car loan (5.49%)

Interestingly, in this example, both methods start with the same debt — the store credit card has both the smallest balance and the highest rate. The paths diverge after that. The avalanche method would have you debt-free in about 32 months, paying roughly $6,400 in total interest.

The Verdict for This Scenario

The avalanche saves about $800 in interest and gets you debt-free two months sooner. But notice that the difference is not as dramatic as you might expect. Both methods work. The best method is the one you will actually stick with.

How to Use the Debt Payoff Calculator

Our calculator at the top of this page makes it easy to compare both strategies with your own numbers. Here is how to get the most out of it:

Step 1: Gather Your Debt Information

Before you start, pull together the following details for each debt:

- Current balance

- Annual interest rate (APR)

- Minimum monthly payment

You can find this information on your most recent statements or by logging into your accounts online.

Step 2: Enter Your Debts

Plug each debt into the calculator. Be thorough — include credit cards, personal loans, car loans, student loans, medical debt, and any other balances you owe. The only debt you might want to leave out is your mortgage, since that operates on a different timeline and payoff strategy.

Step 3: Set Your Extra Payment Amount

This is the amount you can pay above and beyond your combined minimum payments each month. Even an extra $50 makes a difference. If you are not sure how much extra you can afford, check out our budget calculator guide on Finance Pulse to find money in your monthly spending.

Step 4: Compare the Results

The calculator will show you both the snowball and avalanche results side by side, including:

- Total interest paid under each method

- Months until you are completely debt-free

- A month-by-month payoff schedule

- The order in which your debts will be eliminated

Advanced Strategies to Accelerate Your Debt Payoff

Whichever method you choose, these tactics will help you get to zero faster.

The Hybrid Approach

Who says you have to pick just one? Some people start with the snowball to build momentum by knocking out one or two small debts, then switch to the avalanche for the remaining balances. This gives you the psychological boost of quick wins and the mathematical efficiency of interest-rate targeting.

Balance Transfer Cards

If you have good credit, a 0% APR balance transfer card can be a powerful tool. By moving a high-interest balance to a 0% card, you effectively remove interest from the equation for 12 to 21 months. Every dollar you pay goes straight to principal. Just watch out for balance transfer fees (typically 3% to 5%) and make sure you have a plan to pay off the balance before the promotional period ends.

Debt Consolidation Loans

A personal loan at a lower interest rate can simplify multiple debts into a single payment. This works especially well if you have several high-interest credit cards. You will save on interest and only have one payment to manage. Check with your bank, credit union, or an online lender to see what rates you qualify for.

Increase Your Income Temporarily

Side hustles, overtime, freelance work, or selling things you no longer need can all generate extra cash to throw at your debt. Even a temporary income boost of $500 to $1,000 per month can shave months or years off your payoff timeline. The key is to direct that extra money straight to debt, not to lifestyle inflation.

Automate Your Payments

Set up automatic payments for at least the minimum on every debt. Then set up a separate automatic transfer for your extra payment toward your target debt. Automation removes the temptation to skip a payment or spend the money elsewhere.

Negotiate Lower Interest Rates

Call your credit card companies and ask for a rate reduction. If you have been a customer in good standing, many issuers will lower your rate by a few percentage points. Even a small reduction can save you hundreds of dollars over the life of your debt. The worst they can say is no.

Common Mistakes to Avoid

Mistake 1: Not Having an Emergency Fund First

Before you go all-in on debt payoff, make sure you have at least $1,000 to $2,000 set aside for emergencies. Without a cash cushion, one unexpected expense can derail your entire plan and send you right back to the credit cards. Learn more about building your safety net with our emergency fund calculator.

Mistake 2: Closing Credit Cards After Paying Them Off

It is tempting to cut up the card and close the account once the balance hits zero, but this can actually hurt your credit score. Closing a card reduces your total available credit, which increases your credit utilization ratio. Instead, keep the card open, set up a small recurring charge on it, and pay it off automatically each month.

Mistake 3: Only Paying Minimums

Minimum payments are designed to keep you in debt as long as possible. On a $5,000 credit card balance at 20% APR, making only minimum payments could take you over 25 years to pay off and cost you more than $8,000 in interest. Always pay more than the minimum, even if it is just an extra $25 or $50.

Mistake 4: Taking on New Debt While Paying Off Old Debt

This is like bailing water out of a sinking boat without plugging the hole. If you are serious about getting debt-free, stop using credit cards for new purchases. Switch to cash or a debit card until your balances are paid off.

Mistake 5: Ignoring Your Budget

A debt payoff plan without a budget is like a road trip without a map. You need to know exactly where your money is going each month so you can find extra dollars to throw at your debt. Our 50/30/20 budget guide is a great place to start if you do not already have a budget in place.

Frequently Asked Questions

Which method is better, snowball or avalanche?

Neither method is universally “better.” The avalanche saves more money on interest, while the snowball provides faster psychological wins. The best method is the one you will stick with consistently. If you are highly disciplined, go with the avalanche. If you need motivation boosts, choose the snowball.

How much extra should I pay toward debt each month?

As much as you can comfortably afford after covering necessities and a small emergency fund. Even $100 extra per month can dramatically reduce your payoff timeline. Use the calculator above to see exactly how different extra payment amounts affect your results.

Should I pay off debt or save for retirement?

This is a classic personal finance dilemma. As a general rule, if your debt interest rate is higher than your expected investment return (roughly 7% to 10% historically for the stock market), prioritize the debt. However, always contribute enough to your 401(k) to get your employer match — that is free money you should not leave on the table.

Does the debt snowball or avalanche affect my credit score?

Both methods can improve your credit score over time as you reduce your balances and lower your credit utilization ratio. The method you choose does not matter to the credit bureaus — what matters is that you are consistently paying down debt.

Can I switch methods midway through?

Absolutely. Many people start with the snowball to get a few quick wins, then switch to the avalanche once they have built momentum. There is no penalty for changing strategies. The important thing is to keep making progress.

What about mortgage debt?

Most financial advisors recommend keeping mortgage debt separate from your snowball or avalanche plan. Mortgage rates are typically low, the interest is tax-deductible, and the loan terms are long. Focus on consumer debt first, then decide whether accelerating your mortgage payoff makes sense for your situation.

Building Your Personalized Payoff Plan

Now that you understand both methods, here is a simple action plan to get started today:

- List every debt you owe with the balance, interest rate, and minimum payment.

- Run the numbers using the calculator above to see both snowball and avalanche results.

- Choose your method based on your personality and the math.

- Set up automatic payments for minimums on all debts plus your extra payment on the target debt.

- Review monthly and celebrate each debt you eliminate.

- Redirect freed-up payments to the next debt on your list.

- Stay the course until every balance reads $0.

The Bottom Line

The debt snowball and the debt avalanche are both powerful strategies for getting out of debt. The snowball wins on motivation, the avalanche wins on math, and a hybrid approach can give you the best of both worlds. What matters most is not which method you pick — it is that you pick one and stick with it.

Use the calculator above to compare both strategies with your actual numbers. You might be surprised by how close the results are, or you might find that one method clearly saves you more time and money. Either way, the act of running those numbers and making a plan puts you ahead of the vast majority of people who just keep making minimum payments and hoping for the best.

Your debt-free date is out there. Go find it.

Have questions about your debt payoff plan? Explore more tools and guides at Finance Pulse to take control of your financial future.