Your credit card statement is full of numbers that affect your credit score, interest charges, and financial health. Here is what every line means and the three numbers you should check every month.

Most people glance at their credit card statement, see the balance, and either pay it or panic. But your statement contains information that directly affects your credit score, how much interest you pay, and whether you are being charged fees you do not know about.

If you are building credit or paying off credit card debt, understanding your statement is not optional. It takes 2 minutes to review and can save you hundreds of dollars per year in interest and fees.

- Pay the full statement balance (not the minimum) by the due date every month. Paying in full means zero interest — you use the bank’s money free for 21 to 25 days.

- The statement balance is what gets reported to credit bureaus and determines your credit utilization. To show lower utilization, pay down the balance before the statement closing date, not just by the due date.

- Interest charges on your statement should be $0. If they are not, you are carrying a balance — and paying 18 to 28% APR daily on every remaining dollar.

- Minimum payments are designed to keep you in debt for decades. A $5,000 balance at 24% APR paid with minimums only takes roughly 20 years and costs over $6,000 in total interest.

- Review every transaction on your statement for unauthorized charges, forgotten subscriptions, and incorrect amounts. Report unauthorized charges within 60 days — your liability is capped at $50 by federal law.

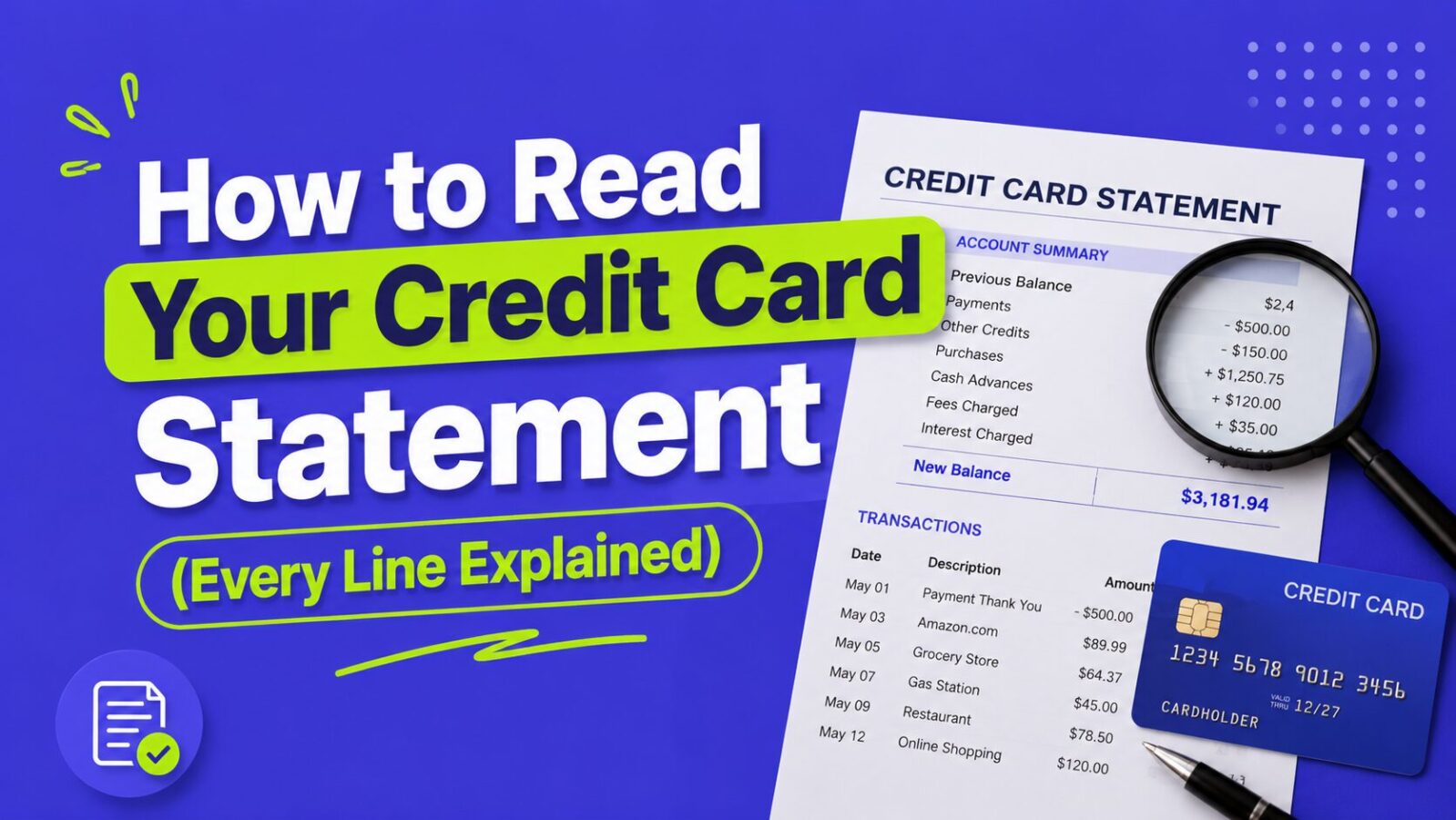

The key sections of your statement

Account summary

This is the top section, showing your high-level numbers:

| Line item | What it means | What to look for |

|---|---|---|

| Previous balance | What you owed at the start of the billing cycle | Should be $0 if you paid your last statement in full |

| Payments and credits | Payments made + refunds received during this cycle | Verify your last payment posted correctly |

| Purchases | Total new charges during this billing cycle | Does this match your expected spending? |

| Balance transfers | Any balances moved from another card | Verify transfer amount and fee are correct |

| Fees charged | Annual fee, late fee, foreign transaction fees, balance transfer fees | Any unexpected fees? Call to dispute or waive. |

| Interest charged | Total interest added this cycle | Should be $0 if you paid in full last month |

| New balance | Previous balance + purchases + fees + interest — payments | The number to pay in full by the due date |

Payment information

Statement balance (new balance): The total you owe as of the statement closing date. Pay this amount by the due date to avoid interest charges. This is the number reported to credit bureaus and determines your credit utilization ratio.

Minimum payment due: The absolute minimum you must pay to avoid a late fee and a negative mark on your credit report. Usually 1 to 3% of the balance, or $25 to $35, whichever is greater. Paying only the minimum means you are carrying a balance and paying interest on the remainder. A $5,000 balance at 24% APR with minimum payments takes roughly 20 years to pay off and costs over $6,000 in interest.

Payment due date: The date your payment must be received to avoid a late fee — typically 21 to 25 days after the statement closing date. This grace period is when you use the card’s money interest-free.

If you cannot pay the full balance: Pay as much as you can above the minimum. Every dollar above the minimum goes directly to reducing your principal. Check if a balance transfer card could give you 0% APR while you pay it off.

The real cost of minimum payments — see your numbers

Minimum Payment Cost Calculator

See the true cost of minimum payments vs paying a fixed amount — and how much you save by paying more each month.

Late payment warning

Federal law requires this disclosure. It shows the late fee (typically $30 to $41 for the first offense, up to $41 for subsequent late payments within 6 billing cycles) and the penalty APR. If you pay late, your APR may increase to the penalty rate (typically 29.99%) — and this can apply to your entire balance, not just new purchases.

A payment more than 30 days past due gets reported to the credit bureaus and can drop your credit score 50 to 100 points. It stays on your report for 7 years. Set up autopay for at least the minimum payment to prevent this entirely.

Minimum payment warning (required by CARD Act)

This section shows two scenarios your card issuer is legally required to disclose: (1) how long it will take and how much you will pay if you only make minimum payments, and (2) how much a fixed higher payment saves. Example: “If you make only the minimum payment, it will take 18 years and 4 months to pay off this balance, and you will pay $8,432 including $3,432 in interest.” The calculator above generates these numbers for your specific balance and APR.

Interest charges

| APR type | Typical rate | What to know |

|---|---|---|

| Purchase APR | 18 to 28% | Applies if you carry a balance. Charges begin after the grace period ends. |

| Balance transfer APR | 0% intro, then 18 to 28% | Shows 0% during promotional period. Watch the end date carefully. |

| Cash advance APR | 25 to 29% | No grace period — interest starts immediately. Plus a 3 to 5% upfront fee. Never use this. |

| Penalty APR | Up to 29.99% | Triggered by late payments. Can apply to your entire balance. |

How interest is calculated: Credit card interest uses the Daily Periodic Rate (APR / 365). A 24% APR means a daily rate of 0.0658%. On a $3,000 balance, daily interest is $1.97. Over 30 days: $59.18. Over a year: roughly $720 — just in interest on one card. If you pay your full statement balance by the due date, you pay $0. The grace period (21 to 25 days between statement close and due date) gives you free use of the bank’s money for that window.

Transaction details

Every purchase, payment, refund, and fee listed individually. Review this section for:

- Unauthorized charges. Contact your issuer immediately. Under the Fair Credit Billing Act, your liability is limited to $50 (most issuers have zero-liability policies). Report within 60 days.

- Forgotten subscriptions. That $14.99/month streaming service you have not used in 3 months? It is in your transactions. Cancel it now.

- Incorrect charges. Double charges, wrong amounts, charges for returned items not credited. Dispute these with your card issuer.

Rewards summary

If you have a cash back or travel rewards card, this section shows points/miles/cash back earned this cycle, total available for redemption, and bonus category earnings.

Check that purchases earned the correct category bonuses. If a grocery store purchase earned 1% instead of 3%, the merchant may be coded as a superstore rather than a supermarket (Walmart and Target are common cases). Most issuers will not fix individual merchant coding, but knowing this helps you decide which card to use at which store.

The three numbers to check every month

Statement date vs due date vs posting date

These three dates confuse many people:

Statement closing date: The last day of your billing cycle. All purchases through this date are on this statement. Your statement balance is calculated as of this date — and this is the balance reported to credit bureaus (affecting your utilization ratio). This matters enormously for your credit score.

Payment due date: 21 to 25 days after the statement closing date. Pay the full statement balance by this date to avoid interest.

Transaction posting date: The date a purchase officially appears on your account — typically 1 to 3 days after you actually made it (the “transaction date”).

Why the closing date matters for your credit score: Your utilization is based on the statement balance. If you spend $4,000/month on a card with a $5,000 limit, your utilization appears as 80% when the statement closes — even if you pay in full by the due date. To show lower utilization: pay down your balance before the statement closing date, not just by the due date. This is the single most underused credit score optimization tactic.

Paper vs electronic statements

Most card issuers default to paperless statements. Benefits: faster delivery, searchable, no physical clutter. Always download or save your statements — keep at least 12 months for tax purposes (business expenses, charitable donations) and dispute reference. Most issuers keep 7 to 10 years of statements accessible online.

Frequently Asked Questions

What happens if I only pay the minimum?

You avoid a late fee and a negative mark on your credit report — but you carry a balance and pay interest on it at 18 to 28% APR. The remaining balance accrues interest daily. The minimum payment warning section of your statement shows you exactly how long it takes and how much it costs. For a $5,000 balance at 24% APR, paying only the minimum takes roughly 20 years and costs over $6,000 in interest — more than the original balance. Use the calculator above to see your specific numbers. Pay the full statement balance whenever possible, and at least more than the minimum every month.

My statement says I owe $0 interest but I carry a balance. Why?

You are likely in a 0% introductory APR promotional period — common for new cards and balance transfer cards. During this period, no interest accrues on purchases or transferred balances as applicable. When the promotional period ends (the date should appear on your statement), interest begins at the standard APR. Check your statement for the promotional end date and use the calculator above to ensure you will pay off the balance before it expires. If the balance is not paid off by then, interest charges will appear on the very next statement.

How do I know when my statement closes?

Look for “statement closing date” or “billing cycle end date” on your statement — it is typically the same date each month (such as the 15th or 22nd of every month). You can also find it in your card issuer’s app under account details. Knowing your closing date is important for credit score optimization: if you want to lower your reported utilization, time your payments to reduce the balance before this date, not just by the payment due date.

Can I change my credit card due date?

Yes — most issuers allow you to change your payment due date through the app or by calling customer service. This is a free, underused feature. Choose a date that falls a few days after your biggest paycheck arrives for the easiest cash flow management. For example, if you get paid on the 1st and 15th, a due date around the 8th or 20th ensures money is available before the payment posts. You can usually choose from a range of dates the issuer offers.

My statement shows a charge I did not make. What do I do?

Call your card issuer’s fraud department immediately — look for the number on the back of your card or on your statement header. File a dispute. Under the Fair Credit Billing Act, you are not liable for more than $50 in unauthorized charges for credit cards, and most issuers have zero-liability policies. They will issue a temporary credit while investigating (typically within 5 business days). Also review your other accounts and credit report for signs of identity theft. Change your card password and enable 2FA if you have not already.

Is my credit card statement the same as my credit report?

No — they are different documents from different sources. Your credit card statement comes from your card issuer and shows your activity for one billing cycle (purchases, payments, fees, interest). Your credit report comes from the three credit bureaus (Equifax, Experian, TransUnion) and shows all your credit accounts, payment history, credit limits, and public records going back years. Your statement feeds into your credit report — the balance on your statement is what gets reported to the bureaus and used to calculate your credit utilization ratio. Check both regularly: statements monthly, credit reports at AnnualCreditReport.com at least once per year (free weekly access).

Why does my credit score go up after I pay my card, even when I paid the last statement in full?

Because your credit score responds to reported balances, not to whether you paid in full. Here is the timing: your statement closes, the balance gets reported to bureaus (high utilization), then you pay in full. The next month, your lower balance is reported (low utilization) and your score goes up. If you carry a high balance throughout the month but pay in full on the due date, your reported utilization may still be high because the bureau captured the statement balance before your payment. To maintain consistently low utilization — and a steadily high score — pay your balance down before the statement closing date, not just by the due date.

My statement has a “cash advance APR” section — can I just use my credit card at an ATM?

Technically yes, but you should never do this. Cash advances on credit cards are one of the most expensive ways to access money. They carry a higher APR than purchases (typically 25 to 29%), they have a separate upfront fee of 3 to 5% of the amount withdrawn, and crucially, there is no grace period — interest starts accruing from the moment you take the cash, not from the statement date. A $500 cash advance at 27% APR with a 5% fee costs $25 immediately plus interest from day one. If you need emergency cash, a personal loan, a cash advance from an employer, or a HELOC are all significantly cheaper options.

The bottom line

Your credit card statement is a 2-minute monthly check that protects you from fraud, prevents unnecessary interest charges, and helps you stay on top of your credit score. Check the statement balance (pay it in full), verify interest charges ($0 is the goal), and scan for unexpected fees and unauthorized transactions.

Set up autopay for the full statement balance so you never miss a payment. Then review the statement when it arrives to catch errors, unauthorized charges, and forgotten subscriptions. That is the entire credit card management strategy — simple, fast, and it keeps your finances healthy.

Use the minimum payment calculator above to see exactly how much your current balance costs if you only make minimum payments — and how much you save by paying it down faster.

Next steps:

- Carrying a balance right now? Read our balance transfer cards guide — move your balance to 0% APR and eliminate interest for 15 to 21 months.

- Want to understand your credit score? Read our credit score guide — the statement closing date and utilization connection is explained in full detail.

- Ready to choose a card that earns rewards on your spending? Read our cash back cards guide for the best grocery and dining rewards with no annual fee.